You might also like

- Ratio Analysis: Mr. David Wong/2018Document40 pagesRatio Analysis: Mr. David Wong/2018DAVID WONG LEE KANG LEE KANGNo ratings yet

- Introduction To Accounting Ratios and InterpretationDocument21 pagesIntroduction To Accounting Ratios and InterpretationAnasNo ratings yet

- Lecture 10 Create Financial PlanDocument42 pagesLecture 10 Create Financial Planmoizlaghari71No ratings yet

- Financial Statement Analysis of Kohl's and JCPenneyDocument12 pagesFinancial Statement Analysis of Kohl's and JCPenneyRegina Lee Ford0% (1)

- Ratio Analysis Categories for Accounting PrinciplesDocument20 pagesRatio Analysis Categories for Accounting PrinciplesUmaNo ratings yet

- Chapter 14 - Financial Statement AnalysisDocument40 pagesChapter 14 - Financial Statement Analysisphamngocmai1912No ratings yet

- Engineering Economics Lect 5Document38 pagesEngineering Economics Lect 5Furqan ChaudhryNo ratings yet

- Theory On RationsDocument9 pagesTheory On RationsPriyanshu GuptaNo ratings yet

- Understand key liquidity ratios like current ratio and quick ratio to evaluate a firm's ability to meet short-term obligationsDocument80 pagesUnderstand key liquidity ratios like current ratio and quick ratio to evaluate a firm's ability to meet short-term obligationsAppleCorpuzDelaRosaNo ratings yet

- Financial Ratio AnalysisDocument42 pagesFinancial Ratio Analysisfattiq_1No ratings yet

- Financial RatiosDocument7 pagesFinancial RatiosmelisaNo ratings yet

- Analyze financial ratios to evaluate FM222 courseDocument60 pagesAnalyze financial ratios to evaluate FM222 courseLai Alvarez100% (1)

- Financial Ratio Analysis - Question 1: How Liquid Is The Firm?Document10 pagesFinancial Ratio Analysis - Question 1: How Liquid Is The Firm?Amit KumarNo ratings yet

- Financial AnalysisDocument7 pagesFinancial AnalysisReyza Mikaela AngloNo ratings yet

- Unit 2 RatioDocument51 pagesUnit 2 Ratiov9510491No ratings yet

- Ratios: Jefferson Acar Mark Jasper Figueroa Sean GervasioDocument29 pagesRatios: Jefferson Acar Mark Jasper Figueroa Sean GervasioJefferson AcarNo ratings yet

- Ratios IBMIDocument17 pagesRatios IBMIhaz002No ratings yet

- ROA Net Income/Average Total Asset: Current Assets Current LiabilitiesDocument8 pagesROA Net Income/Average Total Asset: Current Assets Current Liabilitiesal pacinoNo ratings yet

- Ratio Analysis Bank AL Habib Ltd.Document23 pagesRatio Analysis Bank AL Habib Ltd.Hussain M Raza33% (3)

- Measure a Company's Ability to Pay Debt With Liquidity RatiosDocument4 pagesMeasure a Company's Ability to Pay Debt With Liquidity RatiosKeahlyn BoticarioNo ratings yet

- RatiosDocument2 pagesRatiospvbatheNo ratings yet

- Analyze Financial Statements & Assess SolvencyDocument63 pagesAnalyze Financial Statements & Assess Solvencyjeena tarakaiNo ratings yet

- Formula: Working Capital Current Assets Current LiabilitiesDocument15 pagesFormula: Working Capital Current Assets Current LiabilitiesbugsbugsNo ratings yet

- Financial Statements and Ratio AnalysisDocument9 pagesFinancial Statements and Ratio AnalysisRabie HarounNo ratings yet

- Financial RatiosDocument7 pagesFinancial RatiosarungarNo ratings yet

- Lecture 2 - Answer Part 2Document6 pagesLecture 2 - Answer Part 2Thắng ThôngNo ratings yet

- Midterm Departmental Examination Multiple Choice. Identify The Choice That Completes The Statement or Answers The QuestionDocument5 pagesMidterm Departmental Examination Multiple Choice. Identify The Choice That Completes The Statement or Answers The QuestionRandy ManzanoNo ratings yet

- Ratio AnaDocument13 pagesRatio Anakennetjoel8No ratings yet

- Financial Statement Analysis Techniques and RatiosDocument37 pagesFinancial Statement Analysis Techniques and RatiosAiron Bendaña100% (1)

- Key Financial Ratios How To Calculate Them and What They MeanDocument3 pagesKey Financial Ratios How To Calculate Them and What They MeanGilang Anwar HakimNo ratings yet

- Far 3Document9 pagesFar 3Sonu NayakNo ratings yet

- VivaDocument29 pagesVivaA. ShanmugamNo ratings yet

- Financial Ratio MBA Complete ChapterDocument19 pagesFinancial Ratio MBA Complete ChapterDhruv100% (1)

- FM I Chapter TwoDocument19 pagesFM I Chapter Twonegussie birieNo ratings yet

- Financial Health: What Is 'Working Capital'Document11 pagesFinancial Health: What Is 'Working Capital'arhijaziNo ratings yet

- FIN 300 Chapter 3 Analysis of Financial StatementsDocument9 pagesFIN 300 Chapter 3 Analysis of Financial StatementsJean EliaNo ratings yet

- Financial Statement Analysis: Key Liquidity, Profitability and Solvency Ratios (Part 2Document27 pagesFinancial Statement Analysis: Key Liquidity, Profitability and Solvency Ratios (Part 2Anna LomenarioNo ratings yet

- Analysis of Interpretation of Financial StatementsDocument4 pagesAnalysis of Interpretation of Financial StatementsuaenaNo ratings yet

- wk2 SophiaDocument7 pageswk2 SophiaJong ChaNo ratings yet

- CH - 05 Accounting RatiosDocument8 pagesCH - 05 Accounting RatiosMahathi AmudhanNo ratings yet

- Financial Ratio AnalysisDocument12 pagesFinancial Ratio AnalysisKamlesh Kumar KhiyataniNo ratings yet

- Financial RatioDocument26 pagesFinancial RatioMuhammad HasnainNo ratings yet

- Analyze Financial Performance with RatiosDocument6 pagesAnalyze Financial Performance with RatiosLysss EpssssNo ratings yet

- Short-term Solvency and Liquidity Ratios GuideDocument18 pagesShort-term Solvency and Liquidity Ratios GuideSachini Dinushika KankanamgeNo ratings yet

- Financial Management 1Document4 pagesFinancial Management 1Edith MartinNo ratings yet

- Financial Statements Analysis and Financial ModelsDocument15 pagesFinancial Statements Analysis and Financial ModelsBẢO NGUYỄN HUYNo ratings yet

- Financial Analysis ComponentsDocument6 pagesFinancial Analysis Componentskyrian chimaNo ratings yet

- Finance Chapter 4 Online PDFDocument43 pagesFinance Chapter 4 Online PDFJoseph TanNo ratings yet

- Analyze Financial Ratios to Evaluate Business PerformanceDocument13 pagesAnalyze Financial Ratios to Evaluate Business PerformanceAtyaFitriaRiefantsyahNo ratings yet

- Ulas in Customer Financial Analysis: Liquidity RatiosDocument9 pagesUlas in Customer Financial Analysis: Liquidity RatiosVarun GandhiNo ratings yet

- Ratio Analysis: Table O F Co NtentsDocument4 pagesRatio Analysis: Table O F Co NtentsSumit MalikNo ratings yet

- Finman Financial Ratio AnalysisDocument26 pagesFinman Financial Ratio AnalysisJoyce Anne SobremonteNo ratings yet

- Chapter 2 Part 1 - Ratio AnalysisDocument23 pagesChapter 2 Part 1 - Ratio AnalysisMohamed HosnyNo ratings yet

- Ratio and DupontDocument72 pagesRatio and DupontMohit RathourNo ratings yet

- How To Read Balance SheetDocument6 pagesHow To Read Balance SheetDanish SheikhNo ratings yet

- Analysis SumsDocument11 pagesAnalysis SumsJessy NairNo ratings yet

- Fundamentals of Accountancy, Business and Management 2Document38 pagesFundamentals of Accountancy, Business and Management 2wendell john medianaNo ratings yet

- Lo 4Document11 pagesLo 4Omar El-TalNo ratings yet

- Understanding Financial Statements (Review and Analysis of Straub's Book)From EverandUnderstanding Financial Statements (Review and Analysis of Straub's Book)Rating: 5 out of 5 stars5/5 (5)

- Mid SemesterExam.Q ADocument4 pagesMid SemesterExam.Q Ayow jing pei100% (4)

- Cash Flow StatementsDocument19 pagesCash Flow Statementsyow jing peiNo ratings yet

- Week1b IntroductionDocument34 pagesWeek1b Introductionyow jing peiNo ratings yet

- Week1a.introduction To CourseDocument7 pagesWeek1a.introduction To Courseyow jing peiNo ratings yet

- Week11 BudgetingDocument38 pagesWeek11 Budgetingyow jing peiNo ratings yet

- Week3a.journals LedgersDocument10 pagesWeek3a.journals Ledgersyow jing peiNo ratings yet

- Ebf1013 Assignment 1 RatiosDocument2 pagesEbf1013 Assignment 1 Ratiosyow jing peiNo ratings yet

- List of Companies ASSIGNMENT 1Document2 pagesList of Companies ASSIGNMENT 1yow jing peiNo ratings yet

- LedgerDocument4 pagesLedgeryow jing peiNo ratings yet

- Week2b.manualDoubleEntrySystem - Exercises WithoutAnswersDocument4 pagesWeek2b.manualDoubleEntrySystem - Exercises WithoutAnswersyow jing peiNo ratings yet

- CHAPTER 3 - Accounting EquationDocument16 pagesCHAPTER 3 - Accounting Equationyow jing pei100% (2)

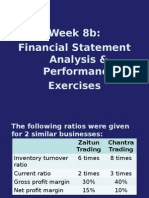

- Week8b.financialStatementsAnalysis Performance - ExercisesDocument12 pagesWeek8b.financialStatementsAnalysis Performance - Exercisesyow jing peiNo ratings yet

- Ebf1013 Assignment 1 RatiosDocument3 pagesEbf1013 Assignment 1 Ratiosyow jing peiNo ratings yet

- Accounting Framework and ConceptsDocument30 pagesAccounting Framework and Conceptsyow jing peiNo ratings yet

- Week2a ManualDoubleEntrySystem PPTTPDocument40 pagesWeek2a ManualDoubleEntrySystem PPTTPyow jing peiNo ratings yet

- Week1c.introduction - Exercises WithoutAnswersDocument8 pagesWeek1c.introduction - Exercises WithoutAnswersyow jing peiNo ratings yet

- Pleting The Accounting CycleDocument65 pagesPleting The Accounting Cycleyow jing peiNo ratings yet

- Week7.Partnerships Corporations OtherOrganisationsDocument40 pagesWeek7.Partnerships Corporations OtherOrganisationsyow jing peiNo ratings yet

- Week6 AComprehensiveIllustrationDocument86 pagesWeek6 AComprehensiveIllustrationyow jing pei89% (28)

- Week4 ClosingTheAccounts TheAdjustingProcessDocument49 pagesWeek4 ClosingTheAccounts TheAdjustingProcessyow jing peiNo ratings yet

- Week12 AccountingEthicsDocument15 pagesWeek12 AccountingEthicsyow jing peiNo ratings yet

- Week6 SampleExamQuestionDocument16 pagesWeek6 SampleExamQuestionyow jing pei67% (3)

- Week3c ReceivablesDocument14 pagesWeek3c Receivablesyow jing peiNo ratings yet

- Property, Plant & Equipment (Fixed Assets) : Reeve Warren DuchacDocument33 pagesProperty, Plant & Equipment (Fixed Assets) : Reeve Warren Duchacyow jing peiNo ratings yet

- Bank Reconciliation StatementDocument17 pagesBank Reconciliation Statementyow jing pei100% (1)

- Warehouse Study Management ProjectDocument46 pagesWarehouse Study Management Projectyow jing peiNo ratings yet

- Supply Chain Management: A Presentation by A.V. VedpuriswarDocument54 pagesSupply Chain Management: A Presentation by A.V. Vedpuriswarramasb4uNo ratings yet

- Supplier Relationship Management in The Context of Supply Chain ManagementDocument12 pagesSupplier Relationship Management in The Context of Supply Chain Managementyow jing peiNo ratings yet

- Supply Chain Management (3rd Edition)Document17 pagesSupply Chain Management (3rd Edition)Shashank SharmaNo ratings yet

- Unincorporated Business TrustDocument9 pagesUnincorporated Business TrustSpencerRyanOneal98% (42)

- Final Exam Fin 2Document3 pagesFinal Exam Fin 2ma. veronica guisihanNo ratings yet

- AUDIT OF INVESTMENTS - AssociateDocument4 pagesAUDIT OF INVESTMENTS - AssociateJoshua LisingNo ratings yet

- BUS 306 Exam 1 - Spring 2011 (B) - Solution by MateevDocument10 pagesBUS 306 Exam 1 - Spring 2011 (B) - Solution by Mateevabhilash5384No ratings yet

- MGMT611 Managing Littlefield TechDocument4 pagesMGMT611 Managing Littlefield Techqiyang84No ratings yet

- Finolex Industries 2QFY18 Results Show Muted GrowthDocument10 pagesFinolex Industries 2QFY18 Results Show Muted GrowthAnonymous y3hYf50mTNo ratings yet

- A Study of Working Capital Management Efficiency of India Cements LTDDocument4 pagesA Study of Working Capital Management Efficiency of India Cements LTDSumeet N ChaudhariNo ratings yet

- Cpa Review School of The Philippines Manila Auditing Problems Audit of Inventories Problem No. 1Document11 pagesCpa Review School of The Philippines Manila Auditing Problems Audit of Inventories Problem No. 1Angelou100% (1)

- Foundations of Financial Management 15th Edition Block Solutions ManualDocument35 pagesFoundations of Financial Management 15th Edition Block Solutions Manualwinifredholmesl39o6z100% (22)

- CMA Performance ManagementDocument135 pagesCMA Performance Managementhmtairek85100% (1)

- Fixed Asset and Depreciation ScheduleDocument5 pagesFixed Asset and Depreciation ScheduleDarkchild HeavensNo ratings yet

- General Deduction Formula-Chapter 4 Slides 2021 With Examples Highlighted PDFDocument28 pagesGeneral Deduction Formula-Chapter 4 Slides 2021 With Examples Highlighted PDFKhensaniNo ratings yet

- Investor Digest 23 Oktober 2019Document10 pagesInvestor Digest 23 Oktober 2019Rising PKN STANNo ratings yet

- Tuguegarao CPA Review HandoutsDocument35 pagesTuguegarao CPA Review HandoutsICPA ReviewNo ratings yet

- Basic Method For Making Economy Study NotesDocument3 pagesBasic Method For Making Economy Study NotesMichael DantogNo ratings yet

- Ben & Jerry's Homemade I. Point of View: A.1 Income Statement H-AnalysisDocument3 pagesBen & Jerry's Homemade I. Point of View: A.1 Income Statement H-AnalysisJeanDianeJovelo100% (1)

- Finance Indus Motor 00Document15 pagesFinance Indus Motor 00laraib nadeemNo ratings yet

- FAR 5.2MC1 Property Plant and Equipment Part 1Document6 pagesFAR 5.2MC1 Property Plant and Equipment Part 1Abegail AdoraNo ratings yet

- Operations Research Course Requirements and TopicsDocument18 pagesOperations Research Course Requirements and TopicsgotdlookzNo ratings yet

- Accounting For Income TaxDocument6 pagesAccounting For Income TaxGirl Lang AkoNo ratings yet

- Financial Statement and Ratio Analysis of Berger Paints Bangladesh LimitedDocument41 pagesFinancial Statement and Ratio Analysis of Berger Paints Bangladesh Limitedpaul ndhlovuNo ratings yet

- Capital Gains Tax PDFDocument3 pagesCapital Gains Tax PDFvalsupmNo ratings yet

- MosaerBaer PDFDocument167 pagesMosaerBaer PDFJupe JonesNo ratings yet

- Retail ManagementDocument7 pagesRetail ManagementLoki LokeshNo ratings yet

- Universal Standards On Social Performance ManagementDocument21 pagesUniversal Standards On Social Performance ManagementTherese MarieNo ratings yet

- WWW Uscis Gov-Sites-Default-Files-Files-Form-I-864Document9 pagesWWW Uscis Gov-Sites-Default-Files-Files-Form-I-864api-269468511No ratings yet

- IRS 1040a Instruction BookDocument92 pagesIRS 1040a Instruction Bookgalaxian100% (1)

- Dividend Policy at FPL Group, Inc. (A)Document16 pagesDividend Policy at FPL Group, Inc. (A)Aslan Alp0% (1)

- Nature of Transactions in A Service BusinessDocument2 pagesNature of Transactions in A Service BusinessYanela YishaNo ratings yet

- Internship Report On Ksic PDFDocument63 pagesInternship Report On Ksic PDFMANORANJAN M SNo ratings yet