You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Global Travel Author Caroline Lodge Date ### Purpose New Mexico Theme Park Ticket SalesDocument6 pagesGlobal Travel Author Caroline Lodge Date ### Purpose New Mexico Theme Park Ticket SalesCaroline LodgeNo ratings yet

- P&CD - in Class #3Document9 pagesP&CD - in Class #3Caroline Lodge100% (2)

- Initial Sample of PropertiesDocument7 pagesInitial Sample of PropertiesCaroline LodgeNo ratings yet

- Why Is Iodine Intake Important?Document5 pagesWhy Is Iodine Intake Important?Caroline LodgeNo ratings yet

- History of Iodine: FDSC 214 Mallori Lawson, Caroline Lodge, Katelyn Henry, Christopher Link, Paul Leonard April 11, 2013Document12 pagesHistory of Iodine: FDSC 214 Mallori Lawson, Caroline Lodge, Katelyn Henry, Christopher Link, Paul Leonard April 11, 2013Caroline LodgeNo ratings yet

- Valuation of Securities-3Document54 pagesValuation of Securities-3anupan92No ratings yet

- Chapter 3 Economic Study MethodsDocument62 pagesChapter 3 Economic Study MethodsJohn Fretz AbelardeNo ratings yet

- Formal Report-CompressedDocument12 pagesFormal Report-Compressedapi-457467141No ratings yet

- TB Chapter 05 Risk and Risk of ReturnsDocument80 pagesTB Chapter 05 Risk and Risk of Returnsabed kayaliNo ratings yet

- Group AssignmentDocument5 pagesGroup AssignmentDuc Thien LuongNo ratings yet

- Chapter 2-GST Part B - Value of SupplyDocument7 pagesChapter 2-GST Part B - Value of SupplyPooja D AcharyaNo ratings yet

- Pennantpark Investment Corporation: PNNT - NasdaqDocument8 pagesPennantpark Investment Corporation: PNNT - NasdaqnicnicooNo ratings yet

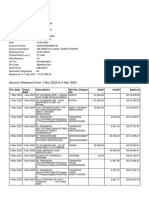

- Account Statement From 1 Mar 2023 To 4 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Mar 2023 To 4 Mar 2023: TXN Date Value Date Description Ref No./Cheque No. Debit Credit Balancesameer bawejaNo ratings yet

- Slides Macroeconomics 1 - FTUDocument50 pagesSlides Macroeconomics 1 - FTUK60 Nguyễn Ái Huyền TrangNo ratings yet

- CH 18 AnsDocument3 pagesCH 18 AnsUsama SaleemNo ratings yet

- Bookkeeper Job DescriptionDocument2 pagesBookkeeper Job Descriptionvener magpayoNo ratings yet

- Abhiraj Layer FarmDocument1 pageAbhiraj Layer Farmbhagwan kumarNo ratings yet

- Currency Hedging: Currency Hedging Is The Use of Financial Instruments, Called Derivative Contracts, ToDocument3 pagesCurrency Hedging: Currency Hedging Is The Use of Financial Instruments, Called Derivative Contracts, Tovivekananda RoyNo ratings yet

- Financial MarketDocument4 pagesFinancial MarketজহিরুলইসলামশোভনNo ratings yet

- Ex10 - Working Capital Management With SolutionDocument9 pagesEx10 - Working Capital Management With SolutionJonas Mondala80% (5)

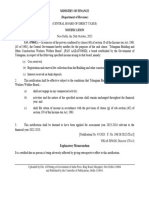

- Notification 93 2023Document1 pageNotification 93 2023tax.contactNo ratings yet

- Form 1040-V: What Is Form 1040-V How To Prepare Your PaymentDocument2 pagesForm 1040-V: What Is Form 1040-V How To Prepare Your PaymentGary KrimsonNo ratings yet

- Indian Bank Debit Card Application Form 1Document2 pagesIndian Bank Debit Card Application Form 1Devil World0% (1)

- Exercise 2Document3 pagesExercise 2Gilang PurwoNo ratings yet

- Export Price List 2011-2012 SystemairDocument312 pagesExport Price List 2011-2012 SystemairCharly ColumbNo ratings yet

- End of Season: Spring Summer 2021Document29 pagesEnd of Season: Spring Summer 2021Abdaud RasyidNo ratings yet

- Case Study 1 AnswerDocument4 pagesCase Study 1 AnswerSharNo ratings yet

- Statement of Cash FlowsDocument13 pagesStatement of Cash FlowsAldrin ZolinaNo ratings yet

- Bank of BarodaDocument99 pagesBank of BarodaYash Parekh100% (2)

- The Nigerian Financial System at A Glance - Monetary Policy DepartmentDocument356 pagesThe Nigerian Financial System at A Glance - Monetary Policy DepartmentAgbons EbohonNo ratings yet

- Momo Statement ReportDocument2 pagesMomo Statement ReportHolybabyNo ratings yet

- Eco401 Final Term NotesDocument5 pagesEco401 Final Term NotesLALANo ratings yet

- Foreign Exchange RiskDocument5 pagesForeign Exchange RiskPushpa BaruaNo ratings yet

- 354158IRSA Institutional Presentation FY22Document26 pages354158IRSA Institutional Presentation FY22Edu DanósNo ratings yet

- ICICI Prudential Multi-Asset Fund Tactical Note-1Document7 pagesICICI Prudential Multi-Asset Fund Tactical Note-1sdaobtrinNo ratings yet