You might also like

- Mitigating FX Risks For TCAS Inc.: Global Vision Financial AdvisorsDocument13 pagesMitigating FX Risks For TCAS Inc.: Global Vision Financial AdvisorsMaverick GmatNo ratings yet

- TDM & Octafx (Business Plan)Document18 pagesTDM & Octafx (Business Plan)nilendumishra500No ratings yet

- Risal TMRWDocument4 pagesRisal TMRWRisal SandiNo ratings yet

- ADIB Current Spending LimitsDocument1 pageADIB Current Spending LimitsMohamed AhmedNo ratings yet

- APF2Document1 pageAPF2chuckepsteinNo ratings yet

- Trade Blotter (Incomplete + Complete)Document8 pagesTrade Blotter (Incomplete + Complete)Barry HeNo ratings yet

- Isi, Ami T, IMITF) I) : Sociat, BankDocument1 pageIsi, Ami T, IMITF) I) : Sociat, BankJamaluddin RubelNo ratings yet

- One+Bank+One+Customer+ +revenue Calculator-+24th+Nov+2020Document4 pagesOne+Bank+One+Customer+ +revenue Calculator-+24th+Nov+2020Sailesh JagdaleNo ratings yet

- Lecture on Foreign Exchange Risk ManagementDocument31 pagesLecture on Foreign Exchange Risk Managementkenny013No ratings yet

- Cryptocurrency Market Capitalizations - CoinMarketCap PDFDocument2 pagesCryptocurrency Market Capitalizations - CoinMarketCap PDFÉmànuel Arcan'jo TarginoNo ratings yet

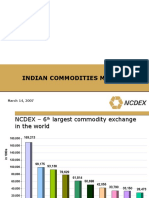

- Indian Commodities Market: March 14, 2007Document40 pagesIndian Commodities Market: March 14, 2007parishkaaNo ratings yet

- Currency Futures-18052018Document14 pagesCurrency Futures-18052018Rajshree DaulatabadNo ratings yet

- COVID19econimpact Template - 032820 - 0Document8 pagesCOVID19econimpact Template - 032820 - 0yoni hathahanNo ratings yet

- Cash Count FormDocument1 pageCash Count FormSith SopanhaNo ratings yet

- L2 - P2 - SENSEX - Sahara and NSEL.2.2Document97 pagesL2 - P2 - SENSEX - Sahara and NSEL.2.2javedaslam38No ratings yet

- 2 Forex Question CciDocument50 pages2 Forex Question CciRavneet KaurNo ratings yet

- ADM04 - Daily Cash Sales Report PDFDocument4 pagesADM04 - Daily Cash Sales Report PDFazraei aizatNo ratings yet

- Dealing Room FX SlidesDocument16 pagesDealing Room FX SlidesThanh TrúcNo ratings yet

- Worksheet R Hidaka, Retailer As at 30 June 2017: BalanceDocument3 pagesWorksheet R Hidaka, Retailer As at 30 June 2017: BalanceIris NguNo ratings yet

- Solo-Forex MarketDocument28 pagesSolo-Forex MarketFajar Putra JakartaNo ratings yet

- Change Mindset To Surf The Wave of Crisis & Aftermath: Rico Usthavia Frans @2020Document19 pagesChange Mindset To Surf The Wave of Crisis & Aftermath: Rico Usthavia Frans @2020Siti Julia AprianiNo ratings yet

- Rate 01112022Document1 pageRate 01112022Jamaluddin RubelNo ratings yet

- Leading Products / 2012: Interest RatesDocument4 pagesLeading Products / 2012: Interest RatesAdemir Peixoto de AzevedoNo ratings yet

- Bes172 p4 Blackmoney 2 Demonetization Soil RateDocument40 pagesBes172 p4 Blackmoney 2 Demonetization Soil Rateroy lexterNo ratings yet

- Manage and Track Your Cryptocurrency PortfolioDocument4 pagesManage and Track Your Cryptocurrency PortfolioJarod28No ratings yet

- Chaanakya 4 - 12Document26 pagesChaanakya 4 - 12Kshitij KumarNo ratings yet

- Money Barter To BitcoinsDocument12 pagesMoney Barter To BitcoinsbhavyaNo ratings yet

- Cryptocurrency Get inDocument16 pagesCryptocurrency Get inavinashdevan12No ratings yet

- Foreign Exchange 2ND November 2020Document15 pagesForeign Exchange 2ND November 2020Jovan SsenkandwaNo ratings yet

- Currency Market: Frontier Research and Chinese Currency Market Qinhua ChenDocument11 pagesCurrency Market: Frontier Research and Chinese Currency Market Qinhua ChenJoe23232232No ratings yet

- EagleEye-Aug10 2021Document6 pagesEagleEye-Aug10 2021Abhinav KeshariNo ratings yet

- Eagle Eye Equities: June 03, 2019Document6 pagesEagle Eye Equities: June 03, 2019Anshuman GuptaNo ratings yet

- Eagle Eye Equities: June 04, 2019Document7 pagesEagle Eye Equities: June 04, 2019Anshuman GuptaNo ratings yet

- Market Update 22nd November 2017Document1 pageMarket Update 22nd November 2017Anonymous iFZbkNwNo ratings yet

- PRODUCTMAPPINGand STRUCTUREFEEREKSADANAOPENEND (UpdatedFeb17th2014) PDFDocument3 pagesPRODUCTMAPPINGand STRUCTUREFEEREKSADANAOPENEND (UpdatedFeb17th2014) PDFZulkifliNo ratings yet

- Product Mapping & Structure Fee Reksadana Open End (Updated February 17Th 2014)Document3 pagesProduct Mapping & Structure Fee Reksadana Open End (Updated February 17Th 2014)AndrianNo ratings yet

- 5 6161346545657577683 PDFDocument6 pages5 6161346545657577683 PDFShivam GoyalNo ratings yet

- 5 6161346545657577683 PDFDocument6 pages5 6161346545657577683 PDFShivam GoyalNo ratings yet

- KWe3 Micro ch20Document52 pagesKWe3 Micro ch20AB DENo ratings yet

- Saving Accounts: Key Fact StatementDocument6 pagesSaving Accounts: Key Fact StatementAfaq YousafNo ratings yet

- Cryptocurrency 2.0Document17 pagesCryptocurrency 2.0avinashdevan12No ratings yet

- Market Update 12th December 2017Document1 pageMarket Update 12th December 2017Anonymous iFZbkNwNo ratings yet

- Rate Sheet For October 5 2023Document1 pageRate Sheet For October 5 2023careernetwork.abeerNo ratings yet

- Market Update 20th November 2017Document1 pageMarket Update 20th November 2017Anonymous iFZbkNwNo ratings yet

- New No 20 Cointech2u Tutarial - Plan Have SoundDocument35 pagesNew No 20 Cointech2u Tutarial - Plan Have Soundwiwat dussadinNo ratings yet

- Currency Trader 0809 Z 77Document48 pagesCurrency Trader 0809 Z 77yaro58No ratings yet

- Market Update 20th July 2018Document1 pageMarket Update 20th July 2018Anonymous FnM14a0No ratings yet

- Les Avoirs de La Libyan Investment Authority Au 30 Juin 2010Document20 pagesLes Avoirs de La Libyan Investment Authority Au 30 Juin 2010LeMonde.frNo ratings yet

- Empowering A New Generation of Trillionaires: About UsDocument13 pagesEmpowering A New Generation of Trillionaires: About Usrexdeus.laptopNo ratings yet

- Forex Euro Currency MarketsDocument22 pagesForex Euro Currency Marketsanzraina100% (4)

- Track Crypto Portfolio in ExcelDocument15 pagesTrack Crypto Portfolio in ExcelRodolfo Castro Jr.No ratings yet

- Total USD Value: Unrealized USD Gain: Total BTC Value: Unrealized BTC GainDocument15 pagesTotal USD Value: Unrealized USD Gain: Total BTC Value: Unrealized BTC GainRodolfo Castro Jr.No ratings yet

- Money Supply, Demand & CreationDocument13 pagesMoney Supply, Demand & Creationpratyush mishraNo ratings yet

- Chapter 5 - Currency Derivatives (FX Management Tools)Document7 pagesChapter 5 - Currency Derivatives (FX Management Tools)jamilkhannNo ratings yet

- Market Update 24th April 2018Document1 pageMarket Update 24th April 2018Anonymous iFZbkNwNo ratings yet

- Saving Account Key FeaturesDocument6 pagesSaving Account Key Featuresmaya aliNo ratings yet

- Eagle Eye Equities: April 03, 2020Document6 pagesEagle Eye Equities: April 03, 2020RogerNo ratings yet

- Bitcoin and Cryptocurrency Technologies: The Ultimate Guide to Everything You Need to Know About CryptocurrenciesFrom EverandBitcoin and Cryptocurrency Technologies: The Ultimate Guide to Everything You Need to Know About CryptocurrenciesNo ratings yet

- Fitch - Accounting ManipulationDocument13 pagesFitch - Accounting ManipulationMarius MuresanNo ratings yet

- Religare)Document118 pagesReligare)Atul ChandraNo ratings yet

- BOP Category GuideDocument29 pagesBOP Category GuidePaul JohnNo ratings yet

- Asset SampleDocument30 pagesAsset SampleDilakshini VjKumarNo ratings yet

- Financial Derivatives 260214Document347 pagesFinancial Derivatives 260214Kavya M Bhat33% (3)

- Itulip - Fire Economy in Crisis Part IDocument16 pagesItulip - Fire Economy in Crisis Part Idonnal47No ratings yet

- Investment AvenuesDocument103 pagesInvestment AvenuesSuresh Gupta50% (2)

- Insider Trading PolicyDocument27 pagesInsider Trading PolicyShubham HiralkarNo ratings yet

- Prestige Institute of Management & Research, Indore: "Analysis of Stock Market at Arihant Capital"Document27 pagesPrestige Institute of Management & Research, Indore: "Analysis of Stock Market at Arihant Capital"Samyak JainNo ratings yet

- A Study On Trading Financial Instruments111Document19 pagesA Study On Trading Financial Instruments111Rajendra NishadNo ratings yet

- Data TechDocument34 pagesData TechPartha ChakaravartiNo ratings yet

- 2023 CFA Level 1 Curriculum Changes Summary (300hours)Document2 pages2023 CFA Level 1 Curriculum Changes Summary (300hours)johnNo ratings yet

- An Introduction To SwapsDocument4 pagesAn Introduction To Swaps777antonio777No ratings yet

- Role of Financial IntermediariesDocument7 pagesRole of Financial IntermediariesSelvanesan G100% (2)

- MScFE 560 FM - Notes1 - M1 - U1Document7 pagesMScFE 560 FM - Notes1 - M1 - U1chiranshNo ratings yet

- Project TopicDocument7 pagesProject TopicmehmudNo ratings yet

- MCCP LeafDocument2 pagesMCCP LeafManish GoelNo ratings yet

- Capital Market: Unit II: PrimaryDocument55 pagesCapital Market: Unit II: PrimaryROHIT CHHUGANI 1823160No ratings yet

- Major ProjectDocument80 pagesMajor ProjectAllan RajuNo ratings yet

- FRM LOBs 111320-FinalDocument65 pagesFRM LOBs 111320-Finalgenius_2No ratings yet

- RSK2601 Complete Questions AnswersDocument84 pagesRSK2601 Complete Questions Answerswycliff brancNo ratings yet

- Icahn RialtoDocument57 pagesIcahn RialtoLas Vegas Review-JournalNo ratings yet

- SIP Report On Equity ResearchDocument56 pagesSIP Report On Equity ResearchAkshay Gour57% (7)

- Aggregation Policy SummaryDocument5 pagesAggregation Policy SummaryjosephmeawadNo ratings yet

- Investment PolicyDocument9 pagesInvestment PolicyCheeseong LimNo ratings yet

- CESR's risk management principles for UCITS fundsDocument22 pagesCESR's risk management principles for UCITS fundsmanugeorgeNo ratings yet

- BBrief Six Degrees of Tiger Management 01 03 12Document11 pagesBBrief Six Degrees of Tiger Management 01 03 12Sarah RamirezNo ratings yet

- Dr. Sharan Shetty PHD (Banking & Finance) Mba (Finance) B. Com (Hons)Document54 pagesDr. Sharan Shetty PHD (Banking & Finance) Mba (Finance) B. Com (Hons)Nagesh Pai MysoreNo ratings yet

- Financial ManagementDocument4 pagesFinancial ManagementPauline BiancaNo ratings yet

- 12.20.10 ENER Dilution Tracker - Dec Debt Swap Boosts Share Out by 5%Document5 pages12.20.10 ENER Dilution Tracker - Dec Debt Swap Boosts Share Out by 5%ac310No ratings yet