You might also like

- Business Financial Information Secrets: How a Business Produces and Utilizes Critical Financial InformationFrom EverandBusiness Financial Information Secrets: How a Business Produces and Utilizes Critical Financial InformationNo ratings yet

- Turning Black Ink Into Gold: How to increase your company's profitability and market value through excellent financial performance reporting, analysis and controlFrom EverandTurning Black Ink Into Gold: How to increase your company's profitability and market value through excellent financial performance reporting, analysis and controlNo ratings yet

- Today's Topics: E-Commerce Fraud Cash Flow Shenanigans Metrics ShenanigansDocument19 pagesToday's Topics: E-Commerce Fraud Cash Flow Shenanigans Metrics ShenanigansZaman HaiderNo ratings yet

- Analysing Accounting Information Systems Risks and FraudsDocument13 pagesAnalysing Accounting Information Systems Risks and FraudsMuskan khanNo ratings yet

- Chapter 12: The Revenue Cycle: Accounting Information Systems: Essential Concepts and ApplicationsDocument37 pagesChapter 12: The Revenue Cycle: Accounting Information Systems: Essential Concepts and ApplicationsVirginia Mianuli Tiarasi SimorangkirNo ratings yet

- SA240 Sandeep ShahDocument40 pagesSA240 Sandeep ShahKING OF TIK TOKNo ratings yet

- iCPA MaterialsDocument26 pagesiCPA MaterialsNicale JeenNo ratings yet

- Top 5 Accounting Firms in The PhilippinesDocument8 pagesTop 5 Accounting Firms in The PhilippinesRoselle Hernandez100% (3)

- Legal Aspects: Fraud Investigations - Employee FraudDocument11 pagesLegal Aspects: Fraud Investigations - Employee FraudCorina-maria DincăNo ratings yet

- CparDocument18 pagesCparLes EvangeListaNo ratings yet

- THE IMPACT OF A-WPS OfficeDocument25 pagesTHE IMPACT OF A-WPS OfficePrasad MamgainNo ratings yet

- Detect Creative Accounting and Financial FraudDocument40 pagesDetect Creative Accounting and Financial FraudAirlanggaZakyNo ratings yet

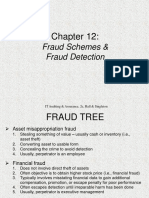

- Fraud Schemes & Fraud Detection: IT Auditing & Assurance, 2e, Hall & SingletonDocument18 pagesFraud Schemes & Fraud Detection: IT Auditing & Assurance, 2e, Hall & SingletonKaren UmaliNo ratings yet

- Unlock Your Financial Blind Spots - Alan Miltz - EC Jan 2012Document57 pagesUnlock Your Financial Blind Spots - Alan Miltz - EC Jan 2012Charles BarnardNo ratings yet

- Checklist For Due Diligence Report For BanksDocument16 pagesChecklist For Due Diligence Report For BanksAddisu Mengist ZNo ratings yet

- Financial Statements Fraud Cases and TheoryDocument25 pagesFinancial Statements Fraud Cases and TheoryCoster Itayi MukushaNo ratings yet

- Ch12 Fraud Scheme DetectionDocument18 pagesCh12 Fraud Scheme DetectionPanda BoarsNo ratings yet

- Business Driven Fraud Management Javelin 2017Document22 pagesBusiness Driven Fraud Management Javelin 2017Sidhu KaurNo ratings yet

- Frequent Asked Questions in ExaminationDocument30 pagesFrequent Asked Questions in ExaminationAmandeep Singh Manku100% (1)

- Presentation Description: Financial Statement Fraud & Corporate Governancethe Satyam CaseDocument5 pagesPresentation Description: Financial Statement Fraud & Corporate Governancethe Satyam CaseRandolph LangstiehNo ratings yet

- Pribanic WhitepaperDocument9 pagesPribanic WhitepaperCaleb PribanicNo ratings yet

- CH 3 Audit of AR and Sales FCNDocument54 pagesCH 3 Audit of AR and Sales FCNመስቀል ኃይላችን ነውNo ratings yet

- INTERNAL CONTROLS For AML ComplianceDocument7 pagesINTERNAL CONTROLS For AML ComplianceOMOLAYONo ratings yet

- Financial Reporting - BeginingDocument28 pagesFinancial Reporting - Beginingelitesquad9432No ratings yet

- KYC Officers - 210724Document29 pagesKYC Officers - 210724anriyasNo ratings yet

- A Survey by World-Check and BMR Advisors August 2009: Anti-Money Laundering in IndiaDocument39 pagesA Survey by World-Check and BMR Advisors August 2009: Anti-Money Laundering in IndiaWaai WophNo ratings yet

- Best Practices SOD Remediation ISACA V2 06.12.15Document12 pagesBest Practices SOD Remediation ISACA V2 06.12.15Norman AdimoNo ratings yet

- Frauds in Financial ReportingDocument12 pagesFrauds in Financial Reportingsathyanandaprabhu2786No ratings yet

- Accounting Entries in SAP FICO FICO SAP Accounting PostingsSAP Training TutorialsDocument7 pagesAccounting Entries in SAP FICO FICO SAP Accounting PostingsSAP Training TutorialsChandu BandreddiNo ratings yet

- Kyc Aml QnaDocument3 pagesKyc Aml QnaThe CSMTNo ratings yet

- Case Study - NextCard Inc.Document3 pagesCase Study - NextCard Inc.Juan Rafael Fernandez0% (1)

- Acquisition International August Page 14 15Document1 pageAcquisition International August Page 14 15KesslerInternationalNo ratings yet

- HTTP WWW Investopedia Com Exam-Guide Cfa-Level-1 Financial-Statements Cash-Flow-Statement-Basics ASPDocument8 pagesHTTP WWW Investopedia Com Exam-Guide Cfa-Level-1 Financial-Statements Cash-Flow-Statement-Basics ASPSimon YossefNo ratings yet

- OneSpan AnalystReport ISMG The State of Digital Account Opening TransformationDocument28 pagesOneSpan AnalystReport ISMG The State of Digital Account Opening TransformationJhordan ZelayaNo ratings yet

- Resume Usman - MBADocument2 pagesResume Usman - MBAusmanNo ratings yet

- Operational Risk ManagementDocument43 pagesOperational Risk ManagementJames Abueg Escaño100% (2)

- Revenue Cycle - 31082021Document46 pagesRevenue Cycle - 31082021buat bersamaNo ratings yet

- Accounts Receivable ManagementDocument24 pagesAccounts Receivable ManagementMaKayla De JesusNo ratings yet

- 1 How To Make Accounting Journal Entries PDFDocument20 pages1 How To Make Accounting Journal Entries PDFLucky MalihanNo ratings yet

- Contact Us for SAP Financial Supply Chain Management Online TrainingDocument12 pagesContact Us for SAP Financial Supply Chain Management Online TrainingFlávio PiresNo ratings yet

- Chapter 02 Financial Reporting and AnalysisDocument40 pagesChapter 02 Financial Reporting and Analysisshabrina r56% (9)

- Disney LandDocument8 pagesDisney LandBik LyNo ratings yet

- AMLCFT Training Module 2021 v2Document79 pagesAMLCFT Training Module 2021 v2pibg skbk2100% (1)

- RecDocument5 pagesRecPrankyJellyNo ratings yet

- Tally BIZ PresentationDocument10 pagesTally BIZ PresentationTurner TuringNo ratings yet

- Information Management in Financial ServicesDocument18 pagesInformation Management in Financial Servicesf1sh01No ratings yet

- I2 Presentation Money Trail v3Document42 pagesI2 Presentation Money Trail v3772748_nareshNo ratings yet

- Financial FraudDocument21 pagesFinancial FraudAayushi AroraNo ratings yet

- Accounting and FinanceDocument15 pagesAccounting and FinanceSujal BedekarNo ratings yet

- MBA Final Semester Finance Project TopicsDocument2 pagesMBA Final Semester Finance Project TopicsRiyas ParakkattilNo ratings yet

- Customer Profitability AnalysisDocument1 pageCustomer Profitability AnalysisJazelle Tenuki Rehara Gunarathne100% (1)

- Module 2 - Is My Customer Credit WorthyDocument11 pagesModule 2 - Is My Customer Credit Worthyiacpa.aialmeNo ratings yet

- Team: Charpoka: - ID:18-37212-1 - ID:18-38895-3 - ID: 17-34195-1 - ID:20-42982-1Document9 pagesTeam: Charpoka: - ID:18-37212-1 - ID:18-38895-3 - ID: 17-34195-1 - ID:20-42982-1Shimul MallickNo ratings yet

- Accounting For Non-ABM - Accounting Equation and The Double-Entry System - Module 2 AsynchronousDocument29 pagesAccounting For Non-ABM - Accounting Equation and The Double-Entry System - Module 2 AsynchronousPamela PerezNo ratings yet

- Marketing AnalyticsDocument7,343 pagesMarketing AnalyticsMaheshBirajdarNo ratings yet

- Methods of Accelarating Cash-InflowDocument23 pagesMethods of Accelarating Cash-InflowChannaveerayya Hiremath100% (1)

- Essentials of Online payment Security and Fraud PreventionFrom EverandEssentials of Online payment Security and Fraud PreventionNo ratings yet

- Wiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)From EverandWiley CMAexcel Learning System Exam Review 2017: Part 1, Financial Reporting, Planning, Performance, and Control (1-year access)No ratings yet

- b07 EbusinessDocument27 pagesb07 EbusinessSheraz HussainNo ratings yet

- Financial Ratio AnalysisDocument29 pagesFinancial Ratio AnalysisSheraz HussainNo ratings yet

- Excellent Foods PresentationDocument31 pagesExcellent Foods PresentationSheraz HussainNo ratings yet

- Excellent Foods PresentationDocument31 pagesExcellent Foods PresentationSheraz HussainNo ratings yet

- Module 4 - Auditor's ResponsibilityDocument28 pagesModule 4 - Auditor's ResponsibilityMAG MAG100% (1)

- The Asset Management Landscape: Second EditionDocument57 pagesThe Asset Management Landscape: Second EditionEduardo Estrada100% (1)

- Procesian Comsostas 7832461584dwdDocument15 pagesProcesian Comsostas 7832461584dwdNikunjNo ratings yet

- Exercise 1 Intro To Management ConsultancyDocument3 pagesExercise 1 Intro To Management ConsultancySiidolohNo ratings yet

- Module 3 Topic 3 in Cooperative ManagementDocument34 pagesModule 3 Topic 3 in Cooperative Managementharon franciscoNo ratings yet

- Information Technology Auditing and Assurance: Computer-Assisted Audit Tools and Techniques Multiple Choice QuestionsDocument3 pagesInformation Technology Auditing and Assurance: Computer-Assisted Audit Tools and Techniques Multiple Choice QuestionsRonald FloresNo ratings yet

- 3 Angels NepalDocument46 pages3 Angels Nepalविवेक शर्माNo ratings yet

- Markplus CaseDocument20 pagesMarkplus CasePuttyErwinaNo ratings yet

- HabteDocument5 pagesHabteAsfawosen DingamaNo ratings yet

- Internal Auditing Role and IndependenceDocument11 pagesInternal Auditing Role and IndependenceMhmd Habbosh100% (2)

- Robert Half Salary Guide 2012Document9 pagesRobert Half Salary Guide 2012cesarthemillennialNo ratings yet

- Accounting Ethics and The Professional Accountant: The Case of GhanaDocument7 pagesAccounting Ethics and The Professional Accountant: The Case of GhanaDavid SumarauwNo ratings yet

- Condo Furnishing Project: University of San Jose - RecoletosDocument13 pagesCondo Furnishing Project: University of San Jose - RecoletosShenn Rose CarpenteroNo ratings yet

- CH 2 Overview of Transaction Processing and ERP SystemsDocument5 pagesCH 2 Overview of Transaction Processing and ERP SystemsAnita Eva Erdina0% (1)

- Lanka Credit and Business Finance PLC (The Company) Errata Notice - Provisional Financial Statements For The Nine Months Ended 31 December 2021Document12 pagesLanka Credit and Business Finance PLC (The Company) Errata Notice - Provisional Financial Statements For The Nine Months Ended 31 December 2021girihellNo ratings yet

- دور المراجعة الداخلية في الحفاظ على القروض الممنوحة وتفعيل إيجابية إدارة المخاطر في البنوك التجاريةDocument13 pagesدور المراجعة الداخلية في الحفاظ على القروض الممنوحة وتفعيل إيجابية إدارة المخاطر في البنوك التجاريةlittazNo ratings yet

- Self Test Coso Erm FrameworkDocument19 pagesSelf Test Coso Erm FrameworkHera AsuncionNo ratings yet

- Normal Duration: Subject Description FormDocument3 pagesNormal Duration: Subject Description Formcoming ohNo ratings yet

- ICAI Student Journal Sep 2021Document36 pagesICAI Student Journal Sep 2021SakshiK ChaturvediNo ratings yet

- GSB Procedure For CertificationDocument2 pagesGSB Procedure For Certificationsaisridhar99No ratings yet

- The Banking and Financial Institutions (Disclosure) Regulation 2014Document12 pagesThe Banking and Financial Institutions (Disclosure) Regulation 2014Michael MwambangaNo ratings yet

- Tax Cooperative Compliance and Federally Collected Tax Revenue in NigeriaDocument22 pagesTax Cooperative Compliance and Federally Collected Tax Revenue in NigeriaPriandhita AsmoroNo ratings yet

- Financial Accounting and Reporting 1 (Acg001) Week 2: Accounting and Its Environment (Part 1)Document19 pagesFinancial Accounting and Reporting 1 (Acg001) Week 2: Accounting and Its Environment (Part 1)kookie bunnyNo ratings yet

- Cenpelco OjtDocument23 pagesCenpelco OjtNefer PitouNo ratings yet

- Process Flow Chart of Quality Assurance DepartmentDocument4 pagesProcess Flow Chart of Quality Assurance DepartmentRanjeetKamatNo ratings yet

- Theory Questions 5 PDF FreeDocument5 pagesTheory Questions 5 PDF FreeSamsung AccountNo ratings yet

- Configuration Steps Third PartyDocument3 pagesConfiguration Steps Third Partyrakesh_sapNo ratings yet

- DBD Accounting ManualDocument47 pagesDBD Accounting ManualFarrukh TouheedNo ratings yet

- AIS Complete Testbank QuizDocument74 pagesAIS Complete Testbank QuizRomiline Umayam100% (5)

- CS Form No. 212 Attachment - Work Experience SheetDocument2 pagesCS Form No. 212 Attachment - Work Experience SheetArnel Pablo100% (2)