You might also like

- Chap 016Document24 pagesChap 016Amrik SinghNo ratings yet

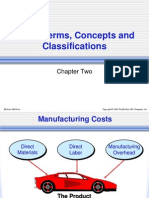

- Costs Terms, Concepts and Classifications: Chapter TwoDocument78 pagesCosts Terms, Concepts and Classifications: Chapter TwoJesus Alberto MarquezNo ratings yet

- Cost Management Concepts and ClassificationsDocument47 pagesCost Management Concepts and ClassificationsAmrik SinghNo ratings yet

- 2 Product Costing Systems Concepts and Design Issues Compatibility ModeDocument73 pages2 Product Costing Systems Concepts and Design Issues Compatibility ModeIamRuzehl VillaverNo ratings yet

- Costs Terms, Concepts and Classifications: Chapter TwoDocument34 pagesCosts Terms, Concepts and Classifications: Chapter TwounobtainableNo ratings yet

- Managerial Accounting Concepts and Principles: Irwin/Mcgraw-HillDocument29 pagesManagerial Accounting Concepts and Principles: Irwin/Mcgraw-HillAmrik SinghNo ratings yet

- Introduction To Managerial Accounting & Cost ConceptsDocument51 pagesIntroduction To Managerial Accounting & Cost ConceptsSandra LangNo ratings yet

- Basic Cost Management Concepts and Accounting For Mass Customization OperationsDocument55 pagesBasic Cost Management Concepts and Accounting For Mass Customization OperationsBelajar MembacaNo ratings yet

- Managerial Accounting and Cost ConceptsDocument85 pagesManagerial Accounting and Cost ConceptsCatherine DelRayNo ratings yet

- Calculating COGS and COGMDocument8 pagesCalculating COGS and COGMAhmed HassanNo ratings yet

- Industrial Management IPE 481: Tanveer Hossain Bhuiyan Assistant Professor, Dept. of IPE BuetDocument63 pagesIndustrial Management IPE 481: Tanveer Hossain Bhuiyan Assistant Professor, Dept. of IPE BuetNaimul Hoque ShuvoNo ratings yet

- The Cost of Goods Manufactured ScheduleDocument7 pagesThe Cost of Goods Manufactured ScheduleM Jamal KhanNo ratings yet

- 02.02.2024 Accounting Cycle For A Manufacturing Company1Document34 pages02.02.2024 Accounting Cycle For A Manufacturing Company1Dennis N. IndigNo ratings yet

- Ronald Hilton Chapter 3Document25 pagesRonald Hilton Chapter 3Swati67% (3)

- ACCG200 Lectures 2-11 HandoutDocument108 pagesACCG200 Lectures 2-11 HandoutNikita Singh DhamiNo ratings yet

- Principles of Accounting, Volume 2: Managerial AccountingDocument59 pagesPrinciples of Accounting, Volume 2: Managerial AccountingVo VeraNo ratings yet

- Principles of Accounting Chapter 16Document28 pagesPrinciples of Accounting Chapter 16myrentistoodamnhighNo ratings yet

- FIN600 Module 3 Topic 2Document25 pagesFIN600 Module 3 Topic 2Inés Tetuá TralleroNo ratings yet

- Process Costing Systems ExplainedDocument74 pagesProcess Costing Systems ExplainedKhairul ImamNo ratings yet

- Product Costing: Job and Process OperationsDocument62 pagesProduct Costing: Job and Process OperationsJackNo ratings yet

- CH 18 - Process CostingDocument46 pagesCH 18 - Process CostingafrizkiNo ratings yet

- Product Costing Systems: Concepts and Design Issues: Mcgraw-Hill/IrwinDocument73 pagesProduct Costing Systems: Concepts and Design Issues: Mcgraw-Hill/IrwinFarid MahdaviNo ratings yet

- Costs Terms, Concepts and Classifications: Chapter TwoDocument23 pagesCosts Terms, Concepts and Classifications: Chapter TwokorpseeNo ratings yet

- Systems Design: Job-Order CostingDocument25 pagesSystems Design: Job-Order CostingSafriza AhmadNo ratings yet

- Chapter 04 Testbank: StudentDocument43 pagesChapter 04 Testbank: StudentHiền DiệuNo ratings yet

- Basic Cost Management Concepts and Accounting For Mass Customization OperationsDocument44 pagesBasic Cost Management Concepts and Accounting For Mass Customization OperationsRoberto De JesusNo ratings yet

- Passaic County Community College AC-205 Quiz #1Document7 pagesPassaic County Community College AC-205 Quiz #1Giovanna CastilloNo ratings yet

- Job Order Costing Systems DesignDocument24 pagesJob Order Costing Systems DesignSonali Jagath100% (1)

- Cost and Managerial Accounting BasicsDocument59 pagesCost and Managerial Accounting BasicsGlenPalmerNo ratings yet

- Cost Accounting Cost AccumulationDocument57 pagesCost Accounting Cost AccumulationRoi Martin A. De VeyraNo ratings yet

- Chapter 4-Product Costing SystemsDocument17 pagesChapter 4-Product Costing SystemsQuế Hoàng Hoài ThươngNo ratings yet

- Chap 1Document22 pagesChap 1Zara Sikander33% (3)

- Ac102 ch2Document21 pagesAc102 ch2Fisseha GebruNo ratings yet

- Summative Quiz: Costing Calculations and Manufacturing CostsDocument2 pagesSummative Quiz: Costing Calculations and Manufacturing CostsVIRGIL KIT AUGUSTIN ABANILLANo ratings yet

- Day 06Document8 pagesDay 06Cy PenalosaNo ratings yet

- Principles of Accounting Chapter 17Document42 pagesPrinciples of Accounting Chapter 17myrentistoodamnhighNo ratings yet

- CH 2 - Cost Terms, Concepts, and ClassificationsDocument78 pagesCH 2 - Cost Terms, Concepts, and ClassificationsLimChanpatiya67% (3)

- Topic 6: Job Order CostingDocument51 pagesTopic 6: Job Order CostingNa RaunaNo ratings yet

- Manufacturing Statement2Document19 pagesManufacturing Statement2istepNo ratings yet

- Discussion - Job CostingDocument3 pagesDiscussion - Job CostingHannah Jane ToribioNo ratings yet

- Overheads AbsorbtionDocument29 pagesOverheads AbsorbtionGaurav AgarwalNo ratings yet

- DocDocument2 pagesDocAzir ShurimaNo ratings yet

- Job Order Costing HandoutsDocument8 pagesJob Order Costing HandoutsHannah Jane Arevalo LafuenteNo ratings yet

- Managerial Accounting and CostDocument19 pagesManagerial Accounting and CostIqra MughalNo ratings yet

- M1 - A3 Calculating Inventory - Finlon Upholstery IncDocument3 pagesM1 - A3 Calculating Inventory - Finlon Upholstery Inczb83100% (1)

- ch-3 To ch-5Document24 pagesch-3 To ch-5Riya DesaiNo ratings yet

- Answers To Exercise Questions - Chapter 2Document7 pagesAnswers To Exercise Questions - Chapter 2reme moNo ratings yet

- Basic Cost Management ConceptsDocument15 pagesBasic Cost Management ConceptsKatCaldwell100% (1)

- 6e Brewer CH02 B EOCDocument12 pages6e Brewer CH02 B EOCLiyanCenNo ratings yet

- Anchor Glass Cost FactorsDocument4 pagesAnchor Glass Cost FactorsJustine Paul Pangasi-anNo ratings yet

- Job Costing Chapter 20 SummaryDocument43 pagesJob Costing Chapter 20 SummaryJitender RawatNo ratings yet

- An Overview of Cost Terms in Chapter 2Document18 pagesAn Overview of Cost Terms in Chapter 2Cesur UğurNo ratings yet

- Cost Accumulation For Job-Shop & Batch Production OperationsDocument60 pagesCost Accumulation For Job-Shop & Batch Production Operationstrillion5No ratings yet

- Practice Questions - Class Excercises 2Document12 pagesPractice Questions - Class Excercises 2Chris With LuvNo ratings yet

- A to Z Cost Accounting Dictionary: A Practical Approach - Theory to CalculationFrom EverandA to Z Cost Accounting Dictionary: A Practical Approach - Theory to CalculationNo ratings yet

- Practical Guide To Production Planning & Control [Revised Edition]From EverandPractical Guide To Production Planning & Control [Revised Edition]Rating: 1 out of 5 stars1/5 (1)

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- Engineering Service Revenues World Summary: Market Values & Financials by CountryFrom EverandEngineering Service Revenues World Summary: Market Values & Financials by CountryNo ratings yet

- Introducing and Naming New Products and Brand ExtensionsDocument15 pagesIntroducing and Naming New Products and Brand ExtensionsamnaNo ratings yet

- Integrating Marketing Communications To Build Brand EquityDocument16 pagesIntegrating Marketing Communications To Build Brand EquityamnaNo ratings yet

- Brand Positioning & ValuesDocument31 pagesBrand Positioning & ValuesamnaNo ratings yet

- Lecture 1 Risk & Return OverviewDocument51 pagesLecture 1 Risk & Return OverviewamnaNo ratings yet

- FinalDocument44 pagesFinalamnaNo ratings yet

- Brand Management EssentialsDocument19 pagesBrand Management EssentialsamnaNo ratings yet

- End-Term Project Assignment Digital Media Strategy Components of DMS (Facebook and Instagram)Document1 pageEnd-Term Project Assignment Digital Media Strategy Components of DMS (Facebook and Instagram)amnaNo ratings yet

- Chapter 001Document19 pagesChapter 001amnaNo ratings yet

- Chapter 1Document28 pagesChapter 1shak91No ratings yet

- Demand and Supply Lec 4Document21 pagesDemand and Supply Lec 4amnaNo ratings yet

- Continental AirlinesDocument9 pagesContinental AirlinesamnaNo ratings yet

- 2016 Specimen Paper 2 Mark Scheme PDFDocument8 pages2016 Specimen Paper 2 Mark Scheme PDFSumaira AliNo ratings yet

- David Sm15 Inppt 04Document51 pagesDavid Sm15 Inppt 04Henry Andino VelásquezNo ratings yet

- Business Research Methods: Attitude MeasurementDocument20 pagesBusiness Research Methods: Attitude MeasurementNael Nasir ChiraghNo ratings yet

- 4 Elements If Quran IlahDocument2 pages4 Elements If Quran IlahamnaNo ratings yet

- Management Accounting: A Business Partner: Lecture # 1Document15 pagesManagement Accounting: A Business Partner: Lecture # 1devilroksNo ratings yet

- Business Research MethodsDocument38 pagesBusiness Research MethodsamnaNo ratings yet

- CH 09Document36 pagesCH 09amnaNo ratings yet

- 02-Operation Strategy and CompetitivenessDocument30 pages02-Operation Strategy and CompetitivenessamnaNo ratings yet

- 03 - Process Analysis and SelectionDocument29 pages03 - Process Analysis and SelectionamnaNo ratings yet

- Introduction To Operations ManagementDocument34 pagesIntroduction To Operations ManagementamnaNo ratings yet

- Economics - Theory and Practice: Ninth EditionDocument16 pagesEconomics - Theory and Practice: Ninth EditionJun Virador MagallonNo ratings yet

- USM SWOT Analysis: Page 1 of 2Document2 pagesUSM SWOT Analysis: Page 1 of 2lingt_6No ratings yet

- DFPR1978 PDFDocument76 pagesDFPR1978 PDFricki2010No ratings yet

- Apex IndustriesDocument62 pagesApex IndustriesAlpeshNo ratings yet

- Anuj Verma's asset allocation notesDocument23 pagesAnuj Verma's asset allocation notesSweta HansariaNo ratings yet

- FI Document: List of Update Terminations: SA38 SE38Document11 pagesFI Document: List of Update Terminations: SA38 SE38Manohar G ShankarNo ratings yet

- Fernando Shashen s3655990 Aero2410 Ind AssignmentDocument5 pagesFernando Shashen s3655990 Aero2410 Ind AssignmentShashen FernandoNo ratings yet

- Return On Assets (ROA) - Meaning, Formula, Assumptions and InterpretationDocument4 pagesReturn On Assets (ROA) - Meaning, Formula, Assumptions and Interpretationakashds16No ratings yet

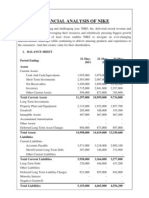

- Financial Analysis of NikeDocument5 pagesFinancial Analysis of NikenimmymathewpkkthlNo ratings yet

- CA IPCC Accounts Group I Nov 14 Guideline Answers 08.11.2014Document16 pagesCA IPCC Accounts Group I Nov 14 Guideline Answers 08.11.2014anupNo ratings yet

- Operating and Financial Leverage - XLSX - 0Document6 pagesOperating and Financial Leverage - XLSX - 0maniNo ratings yet

- Ch08 189-220Document32 pagesCh08 189-220vancho_mkdNo ratings yet

- JS Bank Annual Report December 31 2018 1Document328 pagesJS Bank Annual Report December 31 2018 1binraziNo ratings yet

- ACAS Taxation 2 (Income Tax - Full Midterm Coverage)Document15 pagesACAS Taxation 2 (Income Tax - Full Midterm Coverage)Steven OrtizNo ratings yet

- Robusta Coffee Shop A Feasibility StudyDocument26 pagesRobusta Coffee Shop A Feasibility StudysabberNo ratings yet

- Accounting Standards OverviewDocument21 pagesAccounting Standards Overview119936232141No ratings yet

- Monetary Policy India Last 5 YearsDocument28 pagesMonetary Policy India Last 5 YearsPiyush ChitlangiaNo ratings yet

- Economic Entity AssumptionDocument4 pagesEconomic Entity AssumptionNouman KhanNo ratings yet

- Acca Paper P5 Advanced Performance Management Final Mock ExaminationDocument20 pagesAcca Paper P5 Advanced Performance Management Final Mock ExaminationMSA-ACCANo ratings yet

- Shouldice Hospital Case Study SolutionDocument10 pagesShouldice Hospital Case Study SolutionSinta Surya DewiNo ratings yet

- E120 Fall14 HW6Document2 pagesE120 Fall14 HW6kimball_536238392No ratings yet

- Glencore 31 5 11Document6 pagesGlencore 31 5 11Chandra ChadalawadaNo ratings yet

- Role of Merchant Bankers in Capital MarketsDocument23 pagesRole of Merchant Bankers in Capital MarketschandranilNo ratings yet

- Living TrustDocument7 pagesLiving TrustRocketLawyer100% (30)

- A Study On Financial Performance Using Ratio Analysis in Khivraj Motors PVT LTDDocument30 pagesA Study On Financial Performance Using Ratio Analysis in Khivraj Motors PVT LTDvinoth_17588No ratings yet

- Sales Process Max NewDocument67 pagesSales Process Max NewumeshrathoreNo ratings yet

- AJC Case Analysis.Document4 pagesAJC Case Analysis.sunny rahulNo ratings yet

- Empirical Methods: UvA - Lecture - 01 2019Document57 pagesEmpirical Methods: UvA - Lecture - 01 2019Jason SpanoNo ratings yet

- Merger & AcquisitionDocument15 pagesMerger & AcquisitionmadegNo ratings yet

- Dunlop India Limited 2012 PDFDocument10 pagesDunlop India Limited 2012 PDFdidwaniasNo ratings yet

![Practical Guide To Production Planning & Control [Revised Edition]](https://imgv2-2-f.scribdassets.com/img/word_document/235162742/149x198/2a816df8c8/1709920378?v=1)