You might also like

- Fundamental Economic Concepts: Risk-Adjusted Discount RatesDocument37 pagesFundamental Economic Concepts: Risk-Adjusted Discount Ratestanvir09No ratings yet

- Fundamental Economic Concepts: ©2008 Thomson South-WesternDocument27 pagesFundamental Economic Concepts: ©2008 Thomson South-WesternMangalah Gauari MahaletchnanNo ratings yet

- Managerial Economics (Chapter 13)Document33 pagesManagerial Economics (Chapter 13)api-3703724100% (3)

- Capm - Risk and ReturnDocument81 pagesCapm - Risk and ReturnBeatriz DinisNo ratings yet

- The Basics of Capital Budgeting: Should We Build This Plant?Document36 pagesThe Basics of Capital Budgeting: Should We Build This Plant?EshaNo ratings yet

- Introduction To Risk and ReturnDocument59 pagesIntroduction To Risk and ReturnGaurav AgarwalNo ratings yet

- Fundamental Economic Concepts ExplainedDocument34 pagesFundamental Economic Concepts ExplainedWilliam DC RiveraNo ratings yet

- Session 14-Capital Budgeting and RiskDocument22 pagesSession 14-Capital Budgeting and RiskNANCY BANSALNo ratings yet

- FinanceDocument39 pagesFinancenamien koneNo ratings yet

- Lec 17 NPV, IRR, Profitability IndexDocument29 pagesLec 17 NPV, IRR, Profitability Indexsuryatrikal123No ratings yet

- FIN 402 Capital Budgeting and Corporate Objectives: Yunjeen Kim 5. Portfolio TheoryDocument42 pagesFIN 402 Capital Budgeting and Corporate Objectives: Yunjeen Kim 5. Portfolio TheoryShashankNo ratings yet

- Linear Optimization Models in Finance: BY CHIRAYU K TRIVEDI (207943087) & ALANNA ELBAUM (206459119)Document29 pagesLinear Optimization Models in Finance: BY CHIRAYU K TRIVEDI (207943087) & ALANNA ELBAUM (206459119)Muneéb IrfanNo ratings yet

- Ch-4 Risk and ReturnDocument40 pagesCh-4 Risk and ReturnEyuel SintayehuNo ratings yet

- FINA2010 Financial Management: Lecture 5: Capital Budgeting IIDocument46 pagesFINA2010 Financial Management: Lecture 5: Capital Budgeting IIWai Lam HsuNo ratings yet

- Basics of Capital Budgeting AnalysisDocument30 pagesBasics of Capital Budgeting AnalysisChandra HimaniNo ratings yet

- Risk Assessment Tools and TechniquesDocument27 pagesRisk Assessment Tools and TechniquesMd. Ibtida Fahim 1621749043No ratings yet

- Risk and DiversificationDocument93 pagesRisk and DiversificationANIL_SHAR_MANo ratings yet

- Chap 13 DWDocument45 pagesChap 13 DWMehrab IslamNo ratings yet

- BU7300 Corporate Finance Return, Risk and The Security Market LineDocument45 pagesBU7300 Corporate Finance Return, Risk and The Security Market LineKawther Moh'dNo ratings yet

- Manegerial Economics (Risk Analysis Presentation)Document39 pagesManegerial Economics (Risk Analysis Presentation)Faheem Ul HassanNo ratings yet

- Chapter Thirteen Expected Returns and RiskDocument38 pagesChapter Thirteen Expected Returns and RiskNusratJahanHeabaNo ratings yet

- Chapter VDocument28 pagesChapter VNesri YayaNo ratings yet

- Cash Flow Estimation and Risk AnalysisDocument51 pagesCash Flow Estimation and Risk AnalysisANo ratings yet

- Mangerial EconomicsDocument37 pagesMangerial EconomicsevelynNo ratings yet

- INVESTMENT DECISIONS: WHEN TO INVEST AND WHEN TO WAITDocument49 pagesINVESTMENT DECISIONS: WHEN TO INVEST AND WHEN TO WAITiuNo ratings yet

- CAPITAL BUDGETING by AriefDocument42 pagesCAPITAL BUDGETING by AriefariefNo ratings yet

- IUBFINMAN5555Document25 pagesIUBFINMAN5555Sajan Razzak AkonNo ratings yet

- Chapter II Choice Involving RiskDocument29 pagesChapter II Choice Involving Riskselomonbrhane17171No ratings yet

- Analyzing Projects with Decision Trees and OptionsDocument16 pagesAnalyzing Projects with Decision Trees and OptionsFungai MukundiwaNo ratings yet

- FM - Chapter 4, Return and RiskDocument31 pagesFM - Chapter 4, Return and RiskDaniel BalchaNo ratings yet

- Chap 4: Comparing Net Present Value, Decision Trees, and Real OptionsDocument51 pagesChap 4: Comparing Net Present Value, Decision Trees, and Real OptionsPrabhpuneet PandherNo ratings yet

- Corp Fin OverviewDocument32 pagesCorp Fin OverviewKonstantinos DelaportasNo ratings yet

- Time Value of Money: Practical Application of Compounding & DiscountingDocument32 pagesTime Value of Money: Practical Application of Compounding & DiscountingSaurabh RajputNo ratings yet

- Diversification reduces risk. By combining assets whose returns are not perfectly positively correlated, the portfolio's risk is less than either individual assetDocument75 pagesDiversification reduces risk. By combining assets whose returns are not perfectly positively correlated, the portfolio's risk is less than either individual assetTomNo ratings yet

- Essentials of Investment Analysis and Portfolio ManagementDocument46 pagesEssentials of Investment Analysis and Portfolio Managementprince185No ratings yet

- Chapter 6b Decision Making Under Risk BuncertaintyDocument47 pagesChapter 6b Decision Making Under Risk BuncertaintyTafirenyika SundeNo ratings yet

- 8.risk and ReturnDocument26 pages8.risk and ReturnJorge Luis Astudillo ArévaloNo ratings yet

- Capital Investment DecisionDocument45 pagesCapital Investment DecisionVijayKumar NishadNo ratings yet

- EFM Final Revision Note Dec 2016 PDFDocument48 pagesEFM Final Revision Note Dec 2016 PDFSiu EricNo ratings yet

- INDE/EGRM 6617-02 Engineering Economy and Cost Estimating: Chapter 5: Evaluating A Single ProjectDocument38 pagesINDE/EGRM 6617-02 Engineering Economy and Cost Estimating: Chapter 5: Evaluating A Single Projectfahad noumanNo ratings yet

- JMC Invest4 PDFDocument46 pagesJMC Invest4 PDFIshanviyaNo ratings yet

- Risk Analysis Techniques And Capital Budgeting DecisionsDocument37 pagesRisk Analysis Techniques And Capital Budgeting DecisionsAshish JainNo ratings yet

- Business Finance ExamDocument10 pagesBusiness Finance ExamAstari GatiningtyasNo ratings yet

- The Two Key Concepts in FinanceDocument63 pagesThe Two Key Concepts in FinanceneehubhagiNo ratings yet

- Real Options BV Lec 14Document49 pagesReal Options BV Lec 14Anuranjan TirkeyNo ratings yet

- Risk-adjusted discount rates and certainty equivalents in capital budgetingDocument10 pagesRisk-adjusted discount rates and certainty equivalents in capital budgetingAjmal SalamNo ratings yet

- Valuation of Preferred and Common StockDocument77 pagesValuation of Preferred and Common StockRazvan Dan0% (1)

- FCFChap 005Document30 pagesFCFChap 005ANIS NATASHA BT ABDULNo ratings yet

- Risk and Return Analysis of Stocks and PortfoliosDocument10 pagesRisk and Return Analysis of Stocks and PortfoliosRabinNo ratings yet

- Analyze Project Risk, Break-Even & LeverageDocument27 pagesAnalyze Project Risk, Break-Even & LeverageSadman Skib.No ratings yet

- MS 602 - Lec - Capital BudgetingDocument52 pagesMS 602 - Lec - Capital BudgetingGEORGENo ratings yet

- 7 Jan 17Document46 pages7 Jan 17Kritika BhattNo ratings yet

- Cost of CapitalDocument37 pagesCost of Capitalrajthakre81No ratings yet

- ACC515 Topic 6Document8 pagesACC515 Topic 6Aynul Bashar AmitNo ratings yet

- Decision Recognizing Risks: Topic 5Document24 pagesDecision Recognizing Risks: Topic 5Jayson Dela Cruz OmictinNo ratings yet

- Value at Risk - Theory and IllustrationsDocument75 pagesValue at Risk - Theory and IllustrationsMohamed Amine ElmardiNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- Evaluating Dell's Supply Chain ManagementDocument22 pagesEvaluating Dell's Supply Chain ManagementNoor NadiahNo ratings yet

- New Microsoft PowerPoint PresentationDocument2 pagesNew Microsoft PowerPoint PresentationNoor NadiahNo ratings yet

- HIRARC Piling WorkDocument4 pagesHIRARC Piling Workhairul89% (9)

- Project - Procurement - Management 28 Julai 2011Document6 pagesProject - Procurement - Management 28 Julai 2011Noor NadiahNo ratings yet

- Airbus VS Boeing Slide FinalDocument16 pagesAirbus VS Boeing Slide FinalNoor NadiahNo ratings yet

- ENG Y5 SK by Hafiz ManagerDocument154 pagesENG Y5 SK by Hafiz Managerharryman74No ratings yet

- Notes For ExamDocument11 pagesNotes For ExamNoor NadiahNo ratings yet

- Airbus VS Boeing Slide FinalDocument16 pagesAirbus VS Boeing Slide FinalNoor NadiahNo ratings yet

- Capital Budgeting TechniquesDocument11 pagesCapital Budgeting TechniquesNoor NadiahNo ratings yet

- Strategic Customer Management: Systems, Ethics, and Social ResponsibilityDocument28 pagesStrategic Customer Management: Systems, Ethics, and Social ResponsibilityNoor NadiahNo ratings yet

- En 20140916 KicDocument13 pagesEn 20140916 KicNoor NadiahNo ratings yet

- TFG 2014 Syouffi DDocument54 pagesTFG 2014 Syouffi DMonsur HabibNo ratings yet

- Break Even Point Produce The Desire Profit Cost +target Profit Total ContributionDocument3 pagesBreak Even Point Produce The Desire Profit Cost +target Profit Total ContributionNoor NadiahNo ratings yet

- Topic 2 Procurement PlanningDocument29 pagesTopic 2 Procurement PlanningNoor NadiahNo ratings yet

- C10398712 PDFDocument40 pagesC10398712 PDFNoor NadiahNo ratings yet

- HuhuDocument2 pagesHuhuNoor NadiahNo ratings yet

- Chapter 2 Fundamental Economic ConceptsDocument27 pagesChapter 2 Fundamental Economic ConceptsNoor NadiahNo ratings yet

- Chap 1Document18 pagesChap 1Ismail MohamedNo ratings yet

- Classroom Objects Esl Vocabulary Picture Dictionary Worksheet For Kids PDFDocument2 pagesClassroom Objects Esl Vocabulary Picture Dictionary Worksheet For Kids PDFNoor NadiahNo ratings yet

- Multiple Offers and Acceptance in Contract LawDocument2 pagesMultiple Offers and Acceptance in Contract LawNoor NadiahNo ratings yet

- Laws of Malaysia: Act A1498Document4 pagesLaws of Malaysia: Act A1498Noor NadiahNo ratings yet

- Prices, Outputs, Strategy and Market RegulationDocument21 pagesPrices, Outputs, Strategy and Market RegulationNoor NadiahNo ratings yet

- Chapter 10 Pricing TechniquesDocument31 pagesChapter 10 Pricing TechniquesNoor NadiahNo ratings yet

- Rafting Skateboarding Skydiving Mountain Biking: © 16/01/2017 - All Rights ReservedDocument2 pagesRafting Skateboarding Skydiving Mountain Biking: © 16/01/2017 - All Rights ReservedNoor NadiahNo ratings yet

- Sales of Goods ActDocument32 pagesSales of Goods ActMarjan NaseriNo ratings yet

- Chapter 3 Demand AnalysisDocument30 pagesChapter 3 Demand AnalysisNoor NadiahNo ratings yet

- Marginal Cost Curves CFA Level 1Document2 pagesMarginal Cost Curves CFA Level 1Noor NadiahNo ratings yet

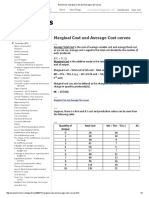

- Economics - Marginal Cost and Average Cost CurvesDocument2 pagesEconomics - Marginal Cost and Average Cost CurvesNoor NadiahNo ratings yet

- Chap 1Document18 pagesChap 1Ismail MohamedNo ratings yet