You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- (Trading Ebook) Pristine - Micro Trading For A Living Micro Trading For A Living PDFDocument54 pages(Trading Ebook) Pristine - Micro Trading For A Living Micro Trading For A Living PDFjairojuradoNo ratings yet

- P2 105 Agency Home Office and Branch Accounting Key AnswersDocument6 pagesP2 105 Agency Home Office and Branch Accounting Key AnswersHikari100% (1)

- Oil PricingDocument68 pagesOil Pricingyash saragiya100% (2)

- Cash SweepDocument5 pagesCash SweepWild FlowerNo ratings yet

- 0108 Futures MagDocument68 pages0108 Futures MagPaul FairleyNo ratings yet

- Key Answer of Chapter 22 of Nonprofit Organization by GuereroDocument8 pagesKey Answer of Chapter 22 of Nonprofit Organization by GuereroArmia MarquezNo ratings yet

- Downloadable Solution Manual For Financial Accounting IFRS 3rd Edition Weygandt Ch01 2Document68 pagesDownloadable Solution Manual For Financial Accounting IFRS 3rd Edition Weygandt Ch01 2Neti Kesumawati100% (2)

- Basic Concepts (Cost Accounting)Document9 pagesBasic Concepts (Cost Accounting)alexandro_novora6396No ratings yet

- MethodsDocument6 pagesMethodsHikariNo ratings yet

- FAR Preboard SolutionsDocument6 pagesFAR Preboard SolutionsHikariNo ratings yet

- FAR Preboard SolutionsDocument4 pagesFAR Preboard SolutionsHikariNo ratings yet

- Reorganization of DOHDocument9 pagesReorganization of DOHHikariNo ratings yet

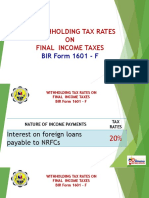

- Ii. Withholding Tax Rates ON Final Income Taxes: BIR Form 1601 - FDocument28 pagesIi. Withholding Tax Rates ON Final Income Taxes: BIR Form 1601 - FAustin Viel Lagman MedinaNo ratings yet

- Biological MoleculesDocument61 pagesBiological MoleculesHikariNo ratings yet

- Intellectual Property Law (R.A. No. 8293 A.K.A. Intellectual Property Code of The Philippines)Document5 pagesIntellectual Property Law (R.A. No. 8293 A.K.A. Intellectual Property Code of The Philippines)HikariNo ratings yet

- Management AccountingDocument3 pagesManagement AccountingHikariNo ratings yet

- Cell TransportDocument37 pagesCell TransportHikariNo ratings yet

- Analysis of Variances From Standard Costs - Solutions PDFDocument39 pagesAnalysis of Variances From Standard Costs - Solutions PDFHikariNo ratings yet

- Securities Regulation CodeDocument11 pagesSecurities Regulation CodeHikariNo ratings yet

- PFRS Adopted by SEC As of December 31, 2011 PDFDocument27 pagesPFRS Adopted by SEC As of December 31, 2011 PDFJennybabe PetaNo ratings yet

- RMYC ScheduleDocument12 pagesRMYC ScheduleHikariNo ratings yet

- ResearchDocument1 pageResearchHikariNo ratings yet

- Tff3e Chapsumm ch05Document3 pagesTff3e Chapsumm ch05Collins CheruiyotNo ratings yet

- Owl ApaformatDocument38 pagesOwl Apaformatapi-268267969No ratings yet

- Strategik 8Document64 pagesStrategik 8HikariNo ratings yet

- Pre Planning PDFDocument5 pagesPre Planning PDFHikariNo ratings yet

- At PreboardDocument12 pagesAt PreboardKevin Ryan EscobarNo ratings yet

- Auditing Theory Solution Manual by Salosagcol (Posted)Document4 pagesAuditing Theory Solution Manual by Salosagcol (Posted)HikariNo ratings yet

- Analysis of Variances From Standard Costs - Solutions PDFDocument39 pagesAnalysis of Variances From Standard Costs - Solutions PDFHikariNo ratings yet

- The Audit Process: Health Research & Informat Ion Division, ESRI, Dublin, July 2008Document36 pagesThe Audit Process: Health Research & Informat Ion Division, ESRI, Dublin, July 2008HikariNo ratings yet

- Chapter 01 - AnswerDocument18 pagesChapter 01 - AnswerTJ NgNo ratings yet

- Business Com Cni 16 18Document3 pagesBusiness Com Cni 16 18HikariNo ratings yet

- Basic Accounting Test Questions1Document4 pagesBasic Accounting Test Questions1Ervin CabangalNo ratings yet

- Quick BooksDocument2 pagesQuick BooksHikariNo ratings yet

- FS Ultj Q3 2018Document94 pagesFS Ultj Q3 2018DianasyNo ratings yet

- Poa T - 8Document3 pagesPoa T - 8SHEVENA A/P VIJIANNo ratings yet

- Group 4 ResearchDocument60 pagesGroup 4 Researchroselletimagos30No ratings yet

- Blaine Kitchenware AssignmentDocument5 pagesBlaine Kitchenware AssignmentChrisNo ratings yet

- BX3031 - L2 - International Parity Conditions - TaggedDocument54 pagesBX3031 - L2 - International Parity Conditions - TaggedSe SeNo ratings yet

- Summer Internship ReportDocument16 pagesSummer Internship ReportRavi MehraNo ratings yet

- Rate NPV 351,212,178.13 365,660,986.27 290,844,716.89 207,520,203.54 Irr 180% 128% 189% 329%Document1 pageRate NPV 351,212,178.13 365,660,986.27 290,844,716.89 207,520,203.54 Irr 180% 128% 189% 329%pinkieNo ratings yet

- Sebi Guidelines Related To Green Shoe OptionDocument4 pagesSebi Guidelines Related To Green Shoe OptionPriyesh ChoureyNo ratings yet

- Financial Marketing Group 4Document31 pagesFinancial Marketing Group 4Emijiano RonquilloNo ratings yet

- MABALAZADocument4 pagesMABALAZAMahasa R HajiiNo ratings yet

- Consolidated and StandaloneDocument9 pagesConsolidated and StandaloneNISHANT RNo ratings yet

- Di OutlineDocument81 pagesDi OutlineRobert E. BrannNo ratings yet

- Final Corporate Finance GROUP 4Document10 pagesFinal Corporate Finance GROUP 4sudipta shrivastavaNo ratings yet

- Financial Modeling & Valuation Analyst (FMVA) ® Certification ProgramDocument2 pagesFinancial Modeling & Valuation Analyst (FMVA) ® Certification ProgramJoseph KachereNo ratings yet

- SARIE Payment ProcessDocument45 pagesSARIE Payment Processsheik abdullahNo ratings yet

- NTCC REPORT Hero Motocorp LTDDocument31 pagesNTCC REPORT Hero Motocorp LTDsagar sharmaNo ratings yet

- Adani Ports and Sez Economic Zone Companyname: Strong Quarter Encouraging GuidanceDocument13 pagesAdani Ports and Sez Economic Zone Companyname: Strong Quarter Encouraging GuidanceAmey TiwariNo ratings yet

- Week 7 Class Exercises (Answers)Document4 pagesWeek 7 Class Exercises (Answers)Chinhoong OngNo ratings yet

- Debt To Asset RatioDocument3 pagesDebt To Asset RatioJaneNo ratings yet

- PK04 NotesDocument24 pagesPK04 NotesBirat Sharma100% (1)

- Literature Review Cash Flow ManagementDocument6 pagesLiterature Review Cash Flow Managementafmzitaaoxahvp100% (2)

- Cash Flows at Warf Computers - Group 5 v.28.09Document8 pagesCash Flows at Warf Computers - Group 5 v.28.09Zero MustafNo ratings yet

- Group 3-Case 1Document3 pagesGroup 3-Case 1Yuki Chen100% (1)

- лекция 6Document28 pagesлекция 6dNo ratings yet

- Mis Assignment 2Document3 pagesMis Assignment 2naraNo ratings yet