You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Cpar - Ap 07.28.13Document12 pagesCpar - Ap 07.28.13KwonyoongmaoNo ratings yet

- Statement of Cash FlowDocument24 pagesStatement of Cash FlowUgly Duckling0% (1)

- Types of Foreign Exchange Exposure: Changes in Exchange Rates Can Effect Firm Value ThroughDocument8 pagesTypes of Foreign Exchange Exposure: Changes in Exchange Rates Can Effect Firm Value ThroughFatim Zohra EssaafNo ratings yet

- CPA Review School of the Philippines Auditing Problems Final Preboard Examination Set September 2013Document18 pagesCPA Review School of the Philippines Auditing Problems Final Preboard Examination Set September 2013Herald Gangcuangco0% (1)

- Help Kit - AoC-4 CFS NBFCDocument15 pagesHelp Kit - AoC-4 CFS NBFCNavneetNo ratings yet

- ESW Capital OverviewDocument7 pagesESW Capital OverviewindyanexpressNo ratings yet

- Interim Report q3 2023Document26 pagesInterim Report q3 2023jvnshrNo ratings yet

- Monthly financial report of a food businessDocument12 pagesMonthly financial report of a food businessAhire Ganesh Ravindra bs20b004No ratings yet

- Afif Juwandira-1162003016-Jawaban UTS Semester GenapDocument10 pagesAfif Juwandira-1162003016-Jawaban UTS Semester GenapYusuf AssegafNo ratings yet

- IAS 10 - Events After The Reporting Period (Detailed Review)Document4 pagesIAS 10 - Events After The Reporting Period (Detailed Review)Nico Rivera CallangNo ratings yet

- State and Public Land Management: The Drivers of Change: Richard Grover Oxford Brookes University United KingdomDocument20 pagesState and Public Land Management: The Drivers of Change: Richard Grover Oxford Brookes University United KingdomsheebheeNo ratings yet

- The Teuer Furniture CaseDocument7 pagesThe Teuer Furniture CaseKshitish100% (9)

- Smartphone Melsie C. TudtudDocument10 pagesSmartphone Melsie C. TudtudEdmon FuentesNo ratings yet

- Corporate Information: (Agensi Di Bawah KPDNHEP)Document6 pagesCorporate Information: (Agensi Di Bawah KPDNHEP)Leow Zi Liang100% (1)

- Unitedhealth Group Inc Swot Analysis BacDocument15 pagesUnitedhealth Group Inc Swot Analysis Bachassan mehmoodNo ratings yet

- Accountancy MCQDocument93 pagesAccountancy MCQabnadeemmalik111No ratings yet

- Call +91 9712985389: To Enquire. Whatsapp: 9830110214Document15 pagesCall +91 9712985389: To Enquire. Whatsapp: 9830110214ThomDeltaNo ratings yet

- Journal Entry For Correction of Errors and CounterbalancingDocument9 pagesJournal Entry For Correction of Errors and CounterbalancingsharbularsNo ratings yet

- CFL's Financial Performance and Corporate Governance AnalysisDocument11 pagesCFL's Financial Performance and Corporate Governance AnalysisHugsNo ratings yet

- Tarc Acc t8Document3 pagesTarc Acc t8Shirley VunNo ratings yet

- Unseen Question TemplateDocument2 pagesUnseen Question TemplategeorgeNo ratings yet

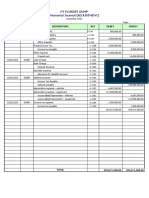

- PT Florist Gump December 2020 Financial StatementDocument9 pagesPT Florist Gump December 2020 Financial StatementSu MiniNo ratings yet

- PRINCIPLES OF ACCOUNTING FORMATDocument4 pagesPRINCIPLES OF ACCOUNTING FORMATSumithaNo ratings yet

- Level Three Theory (Knowledge) Choice: C. Journalizing - Posting - Trial Balance - Financial StatementsDocument17 pagesLevel Three Theory (Knowledge) Choice: C. Journalizing - Posting - Trial Balance - Financial Statementseferem0% (1)

- RWJ Chapter 2 Financial Statements and Cash FlowsDocument39 pagesRWJ Chapter 2 Financial Statements and Cash FlowsAshekin MahadiNo ratings yet

- Intangible Assets Asset Useful Lif Recognized Acquisition Acquirer Balance SheetDocument4 pagesIntangible Assets Asset Useful Lif Recognized Acquisition Acquirer Balance SheetMuhammad Arslan QadirNo ratings yet

- Fundamentals of Accounting Business Management 1Document29 pagesFundamentals of Accounting Business Management 1Nicole AngodungNo ratings yet

- CA-Ipcc Old Course: Advanced AccountingDocument125 pagesCA-Ipcc Old Course: Advanced AccountingAruna Rajappa100% (1)

- Corporate AccountingDocument7 pagesCorporate AccountingAkshit JhingranNo ratings yet

- Harvard Case Study - Flash Inc - AllDocument40 pagesHarvard Case Study - Flash Inc - All竹本口木子100% (1)