You might also like

- Flexiblebudgets 1Document48 pagesFlexiblebudgets 1anon-654501No ratings yet

- 3 Flexible Budgets & StandardsDocument33 pages3 Flexible Budgets & StandardsmedrekNo ratings yet

- FLEXIBLE BUDGETS AND VARIANCESDocument20 pagesFLEXIBLE BUDGETS AND VARIANCESKommineni Ravie KumarNo ratings yet

- 7 Variable Absorption CostingDocument37 pages7 Variable Absorption CostingBəhmən OrucovNo ratings yet

- 3.sales Variance AnalysisDocument38 pages3.sales Variance Analysiskamasuke hegdeNo ratings yet

- 3.4. Overhead CostsDocument43 pages3.4. Overhead CostsmedrekNo ratings yet

- Baims-1618315565 202 PDFDocument3 pagesBaims-1618315565 202 PDFShahadNo ratings yet

- Variable Costing: A Tool for Management InsightsDocument32 pagesVariable Costing: A Tool for Management InsightsSederiku KabaruzaNo ratings yet

- Chapter 7 Garrison 13eDocument40 pagesChapter 7 Garrison 13efarhan MomenNo ratings yet

- Group IV - Variable and Absorption 1Document43 pagesGroup IV - Variable and Absorption 1Mary Ann Ortega AchurraNo ratings yet

- Chap 7 - Flexible Budget, Direct Cost Variance and Management Control - Students NoteDocument13 pagesChap 7 - Flexible Budget, Direct Cost Variance and Management Control - Students NoteZulIzzamreeZolkepliNo ratings yet

- Variable and Absorption CostingDocument23 pagesVariable and Absorption CostingGraciously ElleNo ratings yet

- Costing Methods ComparisonDocument24 pagesCosting Methods ComparisonJohn BernabeNo ratings yet

- Chapter 7 & 8Document29 pagesChapter 7 & 8Mary Ann F. MendezNo ratings yet

- CH 7Document36 pagesCH 7GhadaNo ratings yet

- The Master Budget and Flexible Budgeting: Lecture # 17Document24 pagesThe Master Budget and Flexible Budgeting: Lecture # 17mzNo ratings yet

- Session 9 Flexible Budgets and Variance AnalysesDocument98 pagesSession 9 Flexible Budgets and Variance Analyseschloe lamxdNo ratings yet

- Ch7 Variable CostingDocument20 pagesCh7 Variable CostingHechy HoopNo ratings yet

- Kinney8e PPT Ch09Document36 pagesKinney8e PPT Ch09Ashraf ZamanNo ratings yet

- Flexible Budgets and Variance AnalysisDocument50 pagesFlexible Budgets and Variance AnalysisRanjini SettyNo ratings yet

- C 4 C 00 D 37Document12 pagesC 4 C 00 D 37alyaa rabbaniNo ratings yet

- Variable Costing Tool for ManagementDocument33 pagesVariable Costing Tool for Management1793 Taherul IslamNo ratings yet

- Lecture 5Document39 pagesLecture 5Shixi ZhuNo ratings yet

- Flexible BudgetDocument15 pagesFlexible BudgetDawit AmahaNo ratings yet

- Contribution Price. This Contribution Approach To Pricing Is Most Appropriate When: (1) There Is ADocument7 pagesContribution Price. This Contribution Approach To Pricing Is Most Appropriate When: (1) There Is AEVELYN ROSE MOGAONo ratings yet

- Assignment 111Document20 pagesAssignment 111Mary Ann F. MendezNo ratings yet

- Flexible BudgetDocument15 pagesFlexible BudgetDawit AmahaNo ratings yet

- Static and Flexible Budget ExampleDocument12 pagesStatic and Flexible Budget ExampleAFSYARINA BT ZUNAIDI50% (2)

- CH 3 Cost IIDocument10 pagesCH 3 Cost IIfirewNo ratings yet

- UTS AKMEN - IRA MS - 01012622226026 - 52B FinalDocument7 pagesUTS AKMEN - IRA MS - 01012622226026 - 52B FinalIra M. SariNo ratings yet

- Varaible Costing 2Document18 pagesVaraible Costing 2AIRA NHAIRE MECATENo ratings yet

- Europa Publications Financial AnalysisDocument4 pagesEuropa Publications Financial Analysisbella100% (1)

- Week 5 Variance AnalysisDocument43 pagesWeek 5 Variance AnalysisMichel BanvoNo ratings yet

- BEP N CVP AnalysisDocument49 pagesBEP N CVP AnalysisJamaeca Ann MalsiNo ratings yet

- 02 Profit PlanningDocument32 pages02 Profit PlanningJelliane de la CruzNo ratings yet

- Cost-Volume-Profit AnalysisDocument24 pagesCost-Volume-Profit AnalysisIbrahim ElsayedNo ratings yet

- Chapter 7 Variable Costing A Tool For ManagementDocument34 pagesChapter 7 Variable Costing A Tool For ManagementMulugeta GirmaNo ratings yet

- Review Problem: CVP Relationships: RequiredDocument6 pagesReview Problem: CVP Relationships: RequiredMaika J. PudaderaNo ratings yet

- Tutorial Chapter 12 Cost Behaviour and Measurement of CostsDocument54 pagesTutorial Chapter 12 Cost Behaviour and Measurement of CostsNaKib Nahri0% (1)

- Manufacturing Company Analyzes Costing MethodsDocument8 pagesManufacturing Company Analyzes Costing MethodsNana NurhayatiNo ratings yet

- 10 Variance Analysis Concepts PDFDocument5 pages10 Variance Analysis Concepts PDFbarakkat72No ratings yet

- Garrison 17e GEs PPT Chapter 1Document15 pagesGarrison 17e GEs PPT Chapter 1Princess Jullyn ClaudioNo ratings yet

- Flexible Budgets and Variance Analysis: © 2007 Pearson Education Canada Slide 12-1Document14 pagesFlexible Budgets and Variance Analysis: © 2007 Pearson Education Canada Slide 12-1nowthisisitkoolNo ratings yet

- Variable Costing and Segment Reporting: Tools For ManagementDocument20 pagesVariable Costing and Segment Reporting: Tools For ManagementFarhan RabbehNo ratings yet

- Financial Control - 2 - Variances - Additional Exercises With SolutionDocument9 pagesFinancial Control - 2 - Variances - Additional Exercises With SolutionQuang Nhựt100% (1)

- 107-W7-8-Variable cost-chp05-STDocument48 pages107-W7-8-Variable cost-chp05-STmargaret mariaNo ratings yet

- Flexible Budgets and StandardsDocument16 pagesFlexible Budgets and Standardsborena extensionNo ratings yet

- Managerial CH6 GarriDocument74 pagesManagerial CH6 GarriDalia ElarabyNo ratings yet

- Jawaban Uts ZquuDocument10 pagesJawaban Uts ZquuKattyNo ratings yet

- Variable Costing and Segment Reporting: Tools For ManagementDocument20 pagesVariable Costing and Segment Reporting: Tools For ManagementAbed Al-Rahman SalehNo ratings yet

- Master Budget Variance AnalysisDocument17 pagesMaster Budget Variance AnalysisDavieCDNo ratings yet

- Marginal Costing NotesDocument7 pagesMarginal Costing NotesJul 480weshNo ratings yet

- Variable vs. Absorption CostingDocument21 pagesVariable vs. Absorption Costingsgulay117No ratings yet

- Chapter 7 PPT Version 2Document61 pagesChapter 7 PPT Version 2islamasifNo ratings yet

- CH 14 Var Vs Abs CostingDocument60 pagesCH 14 Var Vs Abs CostingShannon BánañasNo ratings yet

- Answer For Final PracticeDocument5 pagesAnswer For Final Practicedimas suryaNo ratings yet

- Stand CostingDocument38 pagesStand CostingaydhaNo ratings yet

- Module 7 CVP Analysis SolutionsDocument12 pagesModule 7 CVP Analysis SolutionsChiran AdhikariNo ratings yet

- CHAPTER 08 Flixible Budgets and Standard CostsDocument63 pagesCHAPTER 08 Flixible Budgets and Standard CostsNischay RathiNo ratings yet

- A to Z Cost Accounting Dictionary: A Practical Approach - Theory to CalculationFrom EverandA to Z Cost Accounting Dictionary: A Practical Approach - Theory to CalculationNo ratings yet

- Naturally Cool Water Clay Bottle - 1000ML Self Cooling Handmade Lead FreeDocument1 pageNaturally Cool Water Clay Bottle - 1000ML Self Cooling Handmade Lead FreeamanNo ratings yet

- Approved CAE GuidelineDocument50 pagesApproved CAE GuidelineamanNo ratings yet

- Zomatorevenueanalysis 160905035521Document16 pagesZomatorevenueanalysis 160905035521amanNo ratings yet

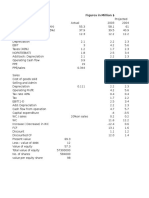

- Monmouth Inc Figures in Million $Document3 pagesMonmouth Inc Figures in Million $amanNo ratings yet

- Stability of The Equilibrium: Reference Material For International Finance Course For Ex-MBA-2016-17Document4 pagesStability of The Equilibrium: Reference Material For International Finance Course For Ex-MBA-2016-17amanNo ratings yet

- Rice Mills of Jharkhand and Their Pollutions Problems by Er. S.K.singhDocument3 pagesRice Mills of Jharkhand and Their Pollutions Problems by Er. S.K.singhamanNo ratings yet

- Tech M + MSat Merger Case Study AnalysisDocument21 pagesTech M + MSat Merger Case Study AnalysisamanNo ratings yet

- HRM - Sustainability Management - 2016-2018 - PPT I - Introduction and Manpower PlanningDocument90 pagesHRM - Sustainability Management - 2016-2018 - PPT I - Introduction and Manpower Planningaman0% (1)

- Cost ConceptsDocument33 pagesCost ConceptsamanNo ratings yet

- HRM-One Year Full Time Program 2016-2017 - Phase 4-Rewards and CompensationDocument43 pagesHRM-One Year Full Time Program 2016-2017 - Phase 4-Rewards and CompensationamanNo ratings yet

- Transfer Pricing Regulations OverviewDocument19 pagesTransfer Pricing Regulations OverviewamanNo ratings yet

- Indian Value System: Ethics. Aristotle in His N.E Part Company WithDocument16 pagesIndian Value System: Ethics. Aristotle in His N.E Part Company WithamanNo ratings yet

- The Marketing Audit Comes of AgeDocument16 pagesThe Marketing Audit Comes of AgeIsaac AdomNo ratings yet

- Market Signals & Competitive MovesDocument8 pagesMarket Signals & Competitive Movesaman100% (1)

- MockExerciseDocument50 pagesMockExerciseamanNo ratings yet

- Case Analysis High Street 05.01.2017Document2 pagesCase Analysis High Street 05.01.2017amanNo ratings yet

- Market Signals & Competitive MovesDocument8 pagesMarket Signals & Competitive Movesaman100% (1)

- Prowess Annual Report Data ComparisonDocument12 pagesProwess Annual Report Data ComparisonamanNo ratings yet

- Sma EvaDocument15 pagesSma EvaamanNo ratings yet

- Prowess Annual Report Data ComparisonDocument12 pagesProwess Annual Report Data ComparisonamanNo ratings yet

- 16 Non Performing AssetsDocument80 pages16 Non Performing AssetsamanNo ratings yet

- Prowess Annual Report Data ComparisonDocument12 pagesProwess Annual Report Data ComparisonamanNo ratings yet

- 16 - What Are BanksDocument42 pages16 - What Are BanksamanNo ratings yet

- Ambuja Cement Annual Report 2015 Web Final - PDF 13Document170 pagesAmbuja Cement Annual Report 2015 Web Final - PDF 13amanNo ratings yet

- PG 367 - Portfolio SelectionDocument2 pagesPG 367 - Portfolio SelectionamanNo ratings yet

- BLDocument4 pagesBLamanNo ratings yet

- PG406 Advertsising CampaignDocument2 pagesPG406 Advertsising CampaignamanNo ratings yet

- X (No. of Cups) Y (No of Plates) 120 160 Profit $/unit 2 1.5Document9 pagesX (No. of Cups) Y (No of Plates) 120 160 Profit $/unit 2 1.5amanNo ratings yet

- Interwar PeriodDocument2 pagesInterwar PeriodamanNo ratings yet

- Internal Audit - Tools & Techniques For Managers PDFDocument6 pagesInternal Audit - Tools & Techniques For Managers PDFNagendra KrishnamurthyNo ratings yet

- 1347957Document99 pages1347957Rohit RsnwalaNo ratings yet

- CC1 A212 - StudentDocument5 pagesCC1 A212 - StudentCarylChooNo ratings yet

- 5S Implementation ProcedureDocument18 pages5S Implementation Procedurehim123verNo ratings yet

- NestleDocument150 pagesNestleMenahil MalikNo ratings yet

- Tax Saving Schemes: in Partial Fulfilment of The Requirements For The Award of The Degree inDocument8 pagesTax Saving Schemes: in Partial Fulfilment of The Requirements For The Award of The Degree inMOHAMMED KHAYYUMNo ratings yet

- The Outsiders EssayDocument7 pagesThe Outsiders Essayezmsdedp100% (2)

- Finance and Account SOPDocument50 pagesFinance and Account SOPشادي الاخرس0% (1)

- Lifting Plan - ChimneyDocument7 pagesLifting Plan - ChimneyHerlander MatosNo ratings yet

- The Adoption of ISA CanadaDocument27 pagesThe Adoption of ISA Canadamajestas777No ratings yet

- ACC101 Course Description SyllabusDocument4 pagesACC101 Course Description SyllabusCristina MosaNo ratings yet

- IAS - 10 Questions-FinalDocument6 pagesIAS - 10 Questions-FinalAbdul SamiNo ratings yet

- MKT 337Document9 pagesMKT 337Mushfique AhmedNo ratings yet

- PepsiCo Changchun JV Capital AnalysisDocument2 pagesPepsiCo Changchun JV Capital AnalysisLeung Hiu Yeung50% (2)

- BessieDocument6 pagesBessieWomayi SamsonNo ratings yet

- Avoid The Seven Deadly Sins of Internal AuditDocument3 pagesAvoid The Seven Deadly Sins of Internal AuditAshu W ChamisaNo ratings yet

- South Western Career College, Inc.: Quarter - Module 1Document19 pagesSouth Western Career College, Inc.: Quarter - Module 1Gessel Ann AbulocionNo ratings yet

- A Organisation Study-ProjectDocument39 pagesA Organisation Study-ProjectDivyaThilakan0% (1)

- Audit Checklist for ISO 14001 EMSDocument8 pagesAudit Checklist for ISO 14001 EMSShubhangi M.100% (1)

- International Standards on Auditing NotesDocument47 pagesInternational Standards on Auditing NotesMuhammad QamarNo ratings yet

- Vda 6.3 2016Document207 pagesVda 6.3 2016Oana Mihai93% (14)

- MCO Minutes SummaryDocument3 pagesMCO Minutes Summarybappy892481100% (1)

- Final Draft RO OPCRDocument50 pagesFinal Draft RO OPCRREGIONAL DIRECTOR SOUTHERN TAGALOGNo ratings yet

- Unrelated Business Income Tax (UBIT) : Internal Revenue CodeDocument2 pagesUnrelated Business Income Tax (UBIT) : Internal Revenue CodeadhiatmajaNo ratings yet

- Assessment A - Short - QuestionsDocument59 pagesAssessment A - Short - Questionsjoe joy0% (1)

- SAP FI Certification Actual QuestionDocument4 pagesSAP FI Certification Actual QuestionkhalidmahmoodqumarNo ratings yet

- Office Fund Request for Salary PaymentsDocument2 pagesOffice Fund Request for Salary PaymentsMinlalNo ratings yet

- THE PROVINCE OF NEGROS OCCIDENTAL Vs CommissionersDocument3 pagesTHE PROVINCE OF NEGROS OCCIDENTAL Vs CommissionersJu LanNo ratings yet

- Voucher Payment SettlementDocument1 pageVoucher Payment SettlementAnthony VinceNo ratings yet

- Bu Shivani Report 4Document31 pagesBu Shivani Report 4Shivani AgarwalNo ratings yet