You might also like

- Recruitment Brochure 2023-24Document26 pagesRecruitment Brochure 2023-24Srinath RaoNo ratings yet

- Akamai Ransomware Threat Report h1 22Document30 pagesAkamai Ransomware Threat Report h1 22Sazones Perú Gerardo SalazarNo ratings yet

- Barra OneDocument2 pagesBarra OneShubham PadhyNo ratings yet

- MM Blue PrintDocument77 pagesMM Blue PrintSantosh KumarNo ratings yet

- Accounting Report GST BusinessDocument9 pagesAccounting Report GST BusinessAneeta ann abrahamNo ratings yet

- Mutual Fund Factsheet How ToDocument4 pagesMutual Fund Factsheet How ToAvinash KumbharNo ratings yet

- Marsh Construction Webinar Slide DeckDocument20 pagesMarsh Construction Webinar Slide DecksriramraneNo ratings yet

- Welcome To All Students Dikbangspes Dokpol Pama/ Pns Gol - Iii 2017 at Korlantas PolriDocument25 pagesWelcome To All Students Dikbangspes Dokpol Pama/ Pns Gol - Iii 2017 at Korlantas PolriTaufiq SyahrialNo ratings yet

- Zhou Bicycle Company Cal State La CompressDocument11 pagesZhou Bicycle Company Cal State La CompressjohanhadiwNo ratings yet

- 3.SCRM - The As-Is LandscapeDocument26 pages3.SCRM - The As-Is LandscapeHina QamarNo ratings yet

- Darrell Due and Jun Pan Preliminary Draft: January 21, 1997Document39 pagesDarrell Due and Jun Pan Preliminary Draft: January 21, 1997Megha P NairNo ratings yet

- NullDocument37 pagesNullapi-26292753No ratings yet

- Risk ManagementDocument125 pagesRisk ManagementĐəəpáķ ĞákháŕNo ratings yet

- Zara's Relationship Marketing ApproachDocument4 pagesZara's Relationship Marketing Approachzamiar shamsNo ratings yet

- Conclusion: Bpmm6013 Marketing ManagementDocument22 pagesConclusion: Bpmm6013 Marketing ManagementEmellda MANo ratings yet

- Navg Annual 2005Document131 pagesNavg Annual 2005Radim StuchlikNo ratings yet

- What Is Marketing ?Document35 pagesWhat Is Marketing ?prarthna karwaNo ratings yet

- RBA Security Permissions by RoleDocument38 pagesRBA Security Permissions by Rolekarthikri7693No ratings yet

- Seeds: Bunium BulbocastanumDocument7 pagesSeeds: Bunium BulbocastanumNidaNo ratings yet

- Appendix: Harmonic Pattern TradingDocument16 pagesAppendix: Harmonic Pattern TradingV KumarNo ratings yet

- Market Risk Estimation Using Non-Parametric Value at Risk and Conditional Value at Risk An Empirical Study On The Algerian Stock MarketDocument15 pagesMarket Risk Estimation Using Non-Parametric Value at Risk and Conditional Value at Risk An Empirical Study On The Algerian Stock MarketFabrice GUETSOPNo ratings yet

- 2018 Ethisphere Crisis Management ReportDocument21 pages2018 Ethisphere Crisis Management ReportShikhar KhannaNo ratings yet

- DTH Pharmacy PresentationDocument46 pagesDTH Pharmacy PresentationdrkefyalewtayeNo ratings yet

- HASAB (HIV/AIDS and STD Alliance Bangladesh) : Analysis and Criticism of Diverse Job AdvertisementsDocument8 pagesHASAB (HIV/AIDS and STD Alliance Bangladesh) : Analysis and Criticism of Diverse Job AdvertisementsSabrita SafaNo ratings yet

- Measuring Market Risks for Industries in Vietnam Using VaR and CVaR ApproachesDocument17 pagesMeasuring Market Risks for Industries in Vietnam Using VaR and CVaR ApproachesPkmn MgmnNo ratings yet

- (2015 S2) FINS1613 TutorialSlides Week09 RiskandReturn CostofCapitalDocument68 pages(2015 S2) FINS1613 TutorialSlides Week09 RiskandReturn CostofCapitalSmartunblurrNo ratings yet

- 0607 s10 QP 4 PDFDocument20 pages0607 s10 QP 4 PDFBuebuebueNo ratings yet

- 0607 s09 QP 4 PDFDocument24 pages0607 s09 QP 4 PDFAnderson AlfredNo ratings yet

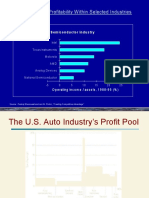

- Differences in Profitability W Ithin Selected Industries: SemiconductorindustryDocument10 pagesDifferences in Profitability W Ithin Selected Industries: SemiconductorindustrymanutdudaNo ratings yet

- The Feasibility StudyDocument52 pagesThe Feasibility StudyBrex Malaluan Galado100% (3)

- QP - Digital Hammers and Electronic Nails - Watson - 1998Document6 pagesQP - Digital Hammers and Electronic Nails - Watson - 1998taha amjadNo ratings yet

- Risk-Taking Channel of Monetary Policy ModelDocument10 pagesRisk-Taking Channel of Monetary Policy ModelPaul Rosado OlivosNo ratings yet

- Oil and Gas: Process Instruments For Reliable MeasurementsDocument24 pagesOil and Gas: Process Instruments For Reliable MeasurementsMajdi BelguithNo ratings yet

- This Study Resource Was Shared Via: Producto Académico #2Document5 pagesThis Study Resource Was Shared Via: Producto Académico #2ALEX JULCA CARRIONNo ratings yet

- Duffie1997 PDFDocument85 pagesDuffie1997 PDFYuri SantosNo ratings yet

- Accounting 132Document2 pagesAccounting 132Anne Marieline BuenaventuraNo ratings yet

- Assaf 2015Document39 pagesAssaf 2015Goldman ClarckNo ratings yet

- DistributionDocument10 pagesDistributionSanda ZahariaNo ratings yet

- Arbitrage Opportunities: A Blessing or A Curse?: Roman Kozhan Wing Wah ThamDocument40 pagesArbitrage Opportunities: A Blessing or A Curse?: Roman Kozhan Wing Wah ThamAloysius AdejoNo ratings yet

- RM Assignment Disha 032Document3 pagesRM Assignment Disha 032Shashwat ShrivastavaNo ratings yet

- Challenges To Internal Security Through CommunicationDocument120 pagesChallenges To Internal Security Through CommunicationVishal GillNo ratings yet

- AVA10004 - PPT 2 - 3 - Segmentation - P - STP - SwinDocument17 pagesAVA10004 - PPT 2 - 3 - Segmentation - P - STP - SwinDavidChenFangHongNo ratings yet

- Business Mathematics PDFDocument90 pagesBusiness Mathematics PDFHABTAMU100% (2)

- Portfolio TheoryDocument10 pagesPortfolio Theoryrameshmba100% (3)

- Risk Management in Canara BankDocument152 pagesRisk Management in Canara BankdeepupopsNo ratings yet

- Eco No Metrics Forecasting 1999 - NonLinear DynamicsDocument43 pagesEco No Metrics Forecasting 1999 - NonLinear Dynamicsapi-27174321No ratings yet

- FbvarDocument4 pagesFbvarSRGVPNo ratings yet

- Financial Analysis of CompanyDocument22 pagesFinancial Analysis of CompanyShakhawat Hossain100% (1)

- A Critical Spare Part Inventory Control Based On Hazard Function Approach - A Case Study in A Garment CompanyDocument9 pagesA Critical Spare Part Inventory Control Based On Hazard Function Approach - A Case Study in A Garment CompanyIshaan ChawlaNo ratings yet

- Solucionario Mecanismos de Transferencia de CalorDocument7 pagesSolucionario Mecanismos de Transferencia de CalorDavid Andres Lopez SaenzNo ratings yet

- Javascript Sample: Precipitation (MM) Per YearDocument3 pagesJavascript Sample: Precipitation (MM) Per YearAndriciMugurelTeodorNo ratings yet

- Quiz 8risk Assessment - Homework Questions After ModificationDocument9 pagesQuiz 8risk Assessment - Homework Questions After ModificationMohamed AbdelkaderNo ratings yet

- Short Note For Safety OfficerDocument24 pagesShort Note For Safety OfficerKhuda BukshNo ratings yet

- BRM Session 6 Value at RiskDocument39 pagesBRM Session 6 Value at RiskSrinita MishraNo ratings yet

- Karunya University Retail Management Exam Question PaperDocument2 pagesKarunya University Retail Management Exam Question PapergaureshraoNo ratings yet

- Whatsapp Pay Project Final SimpliLearnDocument19 pagesWhatsapp Pay Project Final SimpliLearnsneha lokre100% (8)

- Measurement Models For Market Risk Management in NigeriaDocument11 pagesMeasurement Models For Market Risk Management in NigeriaBOHR International Journal of Financial market and Corporate Finance (BIJFMCF)No ratings yet

- Channel Participants and Their RolesDocument12 pagesChannel Participants and Their RolesMahmoudTahboubNo ratings yet

- DR Reta Group 2 Quantitative Analysiss AssignmenetDocument4 pagesDR Reta Group 2 Quantitative Analysiss AssignmenetBereket AlemuNo ratings yet

- Format Laporan LIDocument15 pagesFormat Laporan LInurahaikuNo ratings yet

- Auditing Shariah Way For Isla Fin SerDocument14 pagesAuditing Shariah Way For Isla Fin Serproffina786No ratings yet

- Industrial Training ReportDocument5 pagesIndustrial Training ReportHana ShamsulNo ratings yet

- Format Laporan LIDocument15 pagesFormat Laporan LInurahaikuNo ratings yet

- Basis of Malaysian Income TaxDocument6 pagesBasis of Malaysian Income TaxhisyamstarkNo ratings yet

- PSA Sdn Bhd Internship Log BookDocument1 pagePSA Sdn Bhd Internship Log BookAnonymous tSFKYnLNo ratings yet

- MPA Internship Journal Sample 146Document1 pageMPA Internship Journal Sample 146shippuNo ratings yet

- Citigroup Industrial Training ReportDocument27 pagesCitigroup Industrial Training ReporthisyamstarkNo ratings yet

- Weekly LOG BOOK - Week # 1Document3 pagesWeekly LOG BOOK - Week # 1hisyamstarkNo ratings yet

- USIM-LI-B9 - Student's Leave RecordDocument1 pageUSIM-LI-B9 - Student's Leave RecordSuhana KamelNo ratings yet

- MPA Internship Journal Sample 146Document1 pageMPA Internship Journal Sample 146shippuNo ratings yet

- SHARIAH COMPLIANCE OVERSIGHTDocument21 pagesSHARIAH COMPLIANCE OVERSIGHThisyamstarkNo ratings yet

- MPA Internship Journal Sample 146Document1 pageMPA Internship Journal Sample 146shippuNo ratings yet

- MPA Internship Journal Sample 146Document1 pageMPA Internship Journal Sample 146shippuNo ratings yet

- Format Laporan LIDocument15 pagesFormat Laporan LInurahaikuNo ratings yet

- Note 10 Affirmative Action and Ethnic InequalityDocument33 pagesNote 10 Affirmative Action and Ethnic InequalityhisyamstarkNo ratings yet

- Corporate Governance Requirements for Malaysian CompaniesDocument39 pagesCorporate Governance Requirements for Malaysian CompanieshisyamstarkNo ratings yet

- Shariah Audit - Lecture 4 (Sha Gov Fra)Document37 pagesShariah Audit - Lecture 4 (Sha Gov Fra)hisyamstarkNo ratings yet

- Shariah Audit - Lecture 2 (Shariah Comp) MyDocument29 pagesShariah Audit - Lecture 2 (Shariah Comp) MyhisyamstarkNo ratings yet

- Course Outline MAE4023Document2 pagesCourse Outline MAE4023hisyamstarkNo ratings yet

- MAE4023 Chap1 OverviewDocument18 pagesMAE4023 Chap1 OverviewhisyamstarkNo ratings yet

- Shariah Audit - Lecture 3 (SH Gov Bod)Document25 pagesShariah Audit - Lecture 3 (SH Gov Bod)hisyamstarkNo ratings yet

- Basis of Malaysian Income TaxDocument6 pagesBasis of Malaysian Income TaxhisyamstarkNo ratings yet

- Issuing Tax Invoices: Simplified Tax InvoiceDocument2 pagesIssuing Tax Invoices: Simplified Tax InvoicehisyamstarkNo ratings yet

- Industrial Artificial IntelligenceDocument1 pageIndustrial Artificial IntelligencehisyamstarkNo ratings yet

- MCD4013 Pemasaran Perkhidmatan Kewangan-New SLTDocument5 pagesMCD4013 Pemasaran Perkhidmatan Kewangan-New SLThisyamstarkNo ratings yet

- Entrepreneurship Course OverviewDocument4 pagesEntrepreneurship Course OverviewhisyamstarkNo ratings yet

- MAE4023 Chap1 OverviewDocument18 pagesMAE4023 Chap1 OverviewhisyamstarkNo ratings yet

- Profile of Successful Entrepreneur InterviewDocument1 pageProfile of Successful Entrepreneur InterviewhisyamstarkNo ratings yet

- Final Test Deposit - MurabahahDocument13 pagesFinal Test Deposit - MurabahahNor SyahidahNo ratings yet

- Supporting Shariah Concepts: Shariah Resolutions in Islamic FinanceDocument20 pagesSupporting Shariah Concepts: Shariah Resolutions in Islamic FinanceMohd Afif bin Ab RazakNo ratings yet

- PT Bank Syariah Indonesia TBK 31dec2021 Final FullDocument431 pagesPT Bank Syariah Indonesia TBK 31dec2021 Final FullOnly GameNo ratings yet

- (Ed) Sharia Supervision Committee (Central Bank of Kuwait)Document45 pages(Ed) Sharia Supervision Committee (Central Bank of Kuwait)Mega Putri RachmaNo ratings yet

- Phil Amanah BankDocument37 pagesPhil Amanah BankQuenie De la CruzNo ratings yet

- (WNAzni) Edited IIMMDocument4 pages(WNAzni) Edited IIMMwanazniNo ratings yet

- Internship ReportDocument34 pagesInternship ReportFaisal RayhanNo ratings yet

- Diminishing Musharakah - MBL - PpsDocument17 pagesDiminishing Musharakah - MBL - Ppsgul_e_sabaNo ratings yet

- Islamic Sukuk Concepts & ApplicationsDocument79 pagesIslamic Sukuk Concepts & ApplicationsAsad UllahNo ratings yet

- Islamic Banking in BangladeshDocument26 pagesIslamic Banking in BangladeshAkram khanNo ratings yet

- Introduction to Islamic Bank OperationsDocument18 pagesIntroduction to Islamic Bank OperationsNur JulianieNo ratings yet

- Slide Isb 540Document14 pagesSlide Isb 540Syamil Hakim Abdul GhaniNo ratings yet

- Main ReportDocument63 pagesMain ReportMOhibul Islam LimonNo ratings yet

- DIB Sep 2016Document21 pagesDIB Sep 2016মোমেনুল আলমNo ratings yet

- Sources of FinanceDocument12 pagesSources of FinanceNirmal ShresthaNo ratings yet

- Chapterr 3 ModifiedDocument43 pagesChapterr 3 ModifiedMhmd KaramNo ratings yet

- MIS - Standard Chartered Bank PakistanDocument24 pagesMIS - Standard Chartered Bank PakistanÚmeř RajputNo ratings yet

- Full Report Professional Practice - Group 4Document16 pagesFull Report Professional Practice - Group 4Copter PanuwatNo ratings yet

- Islamic BankingDocument96 pagesIslamic BankingShyna ParkerNo ratings yet

- Growth of Islamic Banking in BangladeshDocument24 pagesGrowth of Islamic Banking in BangladeshFarhat987No ratings yet

- Guidelines On Islamic Financing For Agriculture: Agricultural Credit Department Islamic Banking DepartmentDocument17 pagesGuidelines On Islamic Financing For Agriculture: Agricultural Credit Department Islamic Banking DepartmentMEHEDI HASANNo ratings yet

- Dr. Sutan Emir-ICWIEF 2020 PDFDocument17 pagesDr. Sutan Emir-ICWIEF 2020 PDFMuhamad Arif RohmanNo ratings yet

- Istisna': Week 10 Mudeer Ahmed, PHDDocument10 pagesIstisna': Week 10 Mudeer Ahmed, PHDAsfand YarNo ratings yet

- 10 1108 - Imefm 07 2021 0290Document13 pages10 1108 - Imefm 07 2021 0290hazwani tarmiziNo ratings yet

- Remittance: Bwbs 2013 Islamic Bank OperationDocument15 pagesRemittance: Bwbs 2013 Islamic Bank OperationWardatul RaihanNo ratings yet

- Key differences between AAOIFI and IFRSDocument10 pagesKey differences between AAOIFI and IFRSE-cHa PineappleNo ratings yet

- Teachers With Specialization in Islamic Economics and FinanceDocument5 pagesTeachers With Specialization in Islamic Economics and FinanceAAM26No ratings yet

- Profit Sharing PDFDocument19 pagesProfit Sharing PDFGadisNo ratings yet

- Islamic Banking ExplainedDocument15 pagesIslamic Banking ExplainedSyirah Che AzizNo ratings yet