You might also like

- Music Mart SolutionDocument6 pagesMusic Mart SolutionStranger Sinha50% (2)

- Ribbons an’ Bows case analysisDocument4 pagesRibbons an’ Bows case analysisShivam Kanojia100% (2)

- Lone Pine CafeDocument4 pagesLone Pine CafeRahul TiwariNo ratings yet

- Case 2-2 Music Mart Balance Sheet 1 OctDocument5 pagesCase 2-2 Music Mart Balance Sheet 1 OctAnubhav Jha100% (3)

- Lone Pine Cafe-CaseDocument28 pagesLone Pine Cafe-CaseNadya Rizkita100% (2)

- Case 3.1Document2 pagesCase 3.1Sandeep Agrawal100% (6)

- Dispensers of CaliforniaDocument4 pagesDispensers of CaliforniaShweta GautamNo ratings yet

- ACCOUNTING STERN CORPORATION (A) AnswerDocument4 pagesACCOUNTING STERN CORPORATION (A) AnswerPradina RachmadiniNo ratings yet

- Lone Pine Cafe Case SolutionDocument5 pagesLone Pine Cafe Case SolutionShammika Krishna75% (4)

- Maynard Company financial analysisDocument1 pageMaynard Company financial analysisTarry Berry75% (4)

- Lori Crump Accounting Case StudyDocument1 pageLori Crump Accounting Case StudyHarsh Anchalia100% (1)

- Lone Pine Café FinancialsDocument5 pagesLone Pine Café FinancialsRitu ChhipaNo ratings yet

- Campus PizzeriaDocument12 pagesCampus PizzeriaSHIVAM SRIVASTAVANo ratings yet

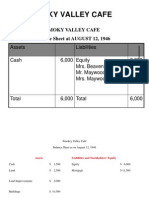

- Smokey Valley Cafe Balance Sheets 1946Document3 pagesSmokey Valley Cafe Balance Sheets 1946mohit_namanNo ratings yet

- Assumptions - : Cash Flow From Operations $ 0Document4 pagesAssumptions - : Cash Flow From Operations $ 0Krish HegdeNo ratings yet

- Forest City Tennis Club General Ledger and Financial StatementsDocument9 pagesForest City Tennis Club General Ledger and Financial StatementsAhmedNiaz100% (1)

- Case Report - Grenell FarmDocument5 pagesCase Report - Grenell Farmajsibal100% (1)

- Case1 1,1 2,2 1,2 2,2 3,3 1,3 2,4 1,4 2,5 1 pb2 6,3 9Document20 pagesCase1 1,1 2,2 1,2 2,2 3,3 1,3 2,4 1,4 2,5 1 pb2 6,3 9amyth_dude_9090100% (2)

- AHM13e - Chapter - 06 Solution To Problems and Key To CasesDocument26 pagesAHM13e - Chapter - 06 Solution To Problems and Key To CasesGaurav ManiyarNo ratings yet

- Problem 3-1Document2 pagesProblem 3-1Omar CirunayNo ratings yet

- Balance Sheet and Transactions Analysis for Charles CompanyDocument14 pagesBalance Sheet and Transactions Analysis for Charles CompanyArunesh SN100% (1)

- Maynard CompanyDocument5 pagesMaynard CompanyNikitha Andrea SaldanhaNo ratings yet

- Waltham Oil Lube Centre Inc - FinalDocument10 pagesWaltham Oil Lube Centre Inc - Finalerarun2267% (3)

- CPL Case Analysis SolutionDocument5 pagesCPL Case Analysis SolutionInder Singh100% (2)

- Case 4 Colgate - Palmolive Makes A Total EffortDocument2 pagesCase 4 Colgate - Palmolive Makes A Total EffortCathy GonzalesNo ratings yet

- Maynard Company (A & B)Document9 pagesMaynard Company (A & B)akashnathgarg0% (1)

- Campus PizzeriaDocument5 pagesCampus PizzeriaJotika MaheshwariNo ratings yet

- Statement of Profit and Loss, Balance Sheet and Cash Flow Analysis for 1999Document4 pagesStatement of Profit and Loss, Balance Sheet and Cash Flow Analysis for 1999Jayash KaushalNo ratings yet

- Revenue Recognition at HBPDocument2 pagesRevenue Recognition at HBPtechna8No ratings yet

- AHM13e Chapter 05 Solution To Problems and Key To CasesDocument21 pagesAHM13e Chapter 05 Solution To Problems and Key To CasesGaurav ManiyarNo ratings yet

- The Garden Spot 1Document25 pagesThe Garden Spot 1Saad Arain0% (1)

- Lone Pine Cafe Balance Sheets Case StudyDocument13 pagesLone Pine Cafe Balance Sheets Case StudyCynthia Anggi Maulina100% (1)

- Hamilton - Case BDocument8 pagesHamilton - Case BJayash KaushalNo ratings yet

- Star Engineering CompanyDocument5 pagesStar Engineering CompanyChleo Espera100% (1)

- Chap004 SolutionsDocument7 pagesChap004 Solutionsdavegeek100% (1)

- Waltham Oil and Lube CentreDocument5 pagesWaltham Oil and Lube CentreAnirudh Singh0% (2)

- Cash Flow StatementDocument4 pagesCash Flow StatementRavina Singh100% (1)

- AHM13e Chapter - 02 - Solution To Problems and Key To CasesDocument23 pagesAHM13e Chapter - 02 - Solution To Problems and Key To CasesGaurav ManiyarNo ratings yet

- QED Electronics - Problem 3.7Document1 pageQED Electronics - Problem 3.7ivanyongforexNo ratings yet

- Problem 4-4 Dindorf CompanyDocument5 pagesProblem 4-4 Dindorf Companymelati50% (4)

- Lewis Corporation case study: Analysis of inventory valuation methodsDocument7 pagesLewis Corporation case study: Analysis of inventory valuation methodsSudeep ShahNo ratings yet

- Lewis Corporation Case 6-2 - Group 5Document8 pagesLewis Corporation Case 6-2 - Group 5Om Prakash100% (1)

- Lava Case Study Decision Paper KaushalDocument4 pagesLava Case Study Decision Paper Kaushalkaushal dhapareNo ratings yet

- Case Analysis Chapter 3Document4 pagesCase Analysis Chapter 3angelllNo ratings yet

- Stafford Press SolvedDocument2 pagesStafford Press SolvedMurali DharanNo ratings yet

- Chapter 3 SolutionsDocument8 pagesChapter 3 SolutionsViren DeshpandeNo ratings yet

- Stafford Press Move Case StudyDocument5 pagesStafford Press Move Case StudyArjun Khosla0% (2)

- Accounting - Text & Cases - 13 Edition Basic Accounting Concepts: The Balance SheetDocument7 pagesAccounting - Text & Cases - 13 Edition Basic Accounting Concepts: The Balance SheetV Hemanth KumarNo ratings yet

- Cash Accounts Receivable Inventories Equipment Income Statement Balance SheetDocument3 pagesCash Accounts Receivable Inventories Equipment Income Statement Balance Sheetrajo_onglao50% (2)

- A Bipartisan Agenda For Change: Case ProblemDocument6 pagesA Bipartisan Agenda For Change: Case ProblemunitybNo ratings yet

- Lone Pine Cafe QuestionDocument2 pagesLone Pine Cafe QuestionSahil JainNo ratings yet

- Gemini PPT 1Document21 pagesGemini PPT 1Bhanu NirwanNo ratings yet

- Accounting-Lone Pine Cafe CaseDocument28 pagesAccounting-Lone Pine Cafe CaseMuadz Akbar100% (1)

- For Analysis Basis of Carmen Diaz CaseDocument9 pagesFor Analysis Basis of Carmen Diaz CaseShielarien DonguilaNo ratings yet

- Managers We Are Katti With You - PPL - Group-4Document11 pagesManagers We Are Katti With You - PPL - Group-4kjhathiNo ratings yet

- Music Mart Balance Sheet TransactionsDocument17 pagesMusic Mart Balance Sheet TransactionsDarwin Dionisio ClementeNo ratings yet

- Problem 2-2: J.L. Gregory CompanyDocument5 pagesProblem 2-2: J.L. Gregory CompanyKAPIL MBA 2021-23 (Delhi)No ratings yet

- Drill Corporate LiquidationDocument3 pagesDrill Corporate LiquidationElizabeth DumawalNo ratings yet

- Complete Control: Business Combination: The Right of Taking DecisionDocument17 pagesComplete Control: Business Combination: The Right of Taking DecisionSaurabh AwatiNo ratings yet

- Chapter 2Document20 pagesChapter 2Coursehero PremiumNo ratings yet

- Letter - Cover Dep. Ed.Document1 pageLetter - Cover Dep. Ed.Darwin Dionisio ClementeNo ratings yet

- Lakbay AralDocument2 pagesLakbay AralDarwin Dionisio ClementeNo ratings yet

- Job Ads PostingDocument2 pagesJob Ads PostingDarwin Dionisio ClementeNo ratings yet

- Feast Day MassDocument1 pageFeast Day MassDarwin Dionisio ClementeNo ratings yet

- Deped Request For Cert. of Good Standing (School)Document1 pageDeped Request For Cert. of Good Standing (School)Darwin Dionisio ClementeNo ratings yet

- High School Course Offering ClarificationDocument1 pageHigh School Course Offering ClarificationDarwin Dionisio ClementeNo ratings yet

- Graduation Mass S.Y. 2020-2021Document1 pageGraduation Mass S.Y. 2020-2021Darwin Dionisio ClementeNo ratings yet

- For Choir Outing (Letter and Waiver)Document1 pageFor Choir Outing (Letter and Waiver)Darwin Dionisio ClementeNo ratings yet

- Garbage CollectionDocument1 pageGarbage CollectionDarwin Dionisio ClementeNo ratings yet

- Foundation Day MassDocument1 pageFoundation Day MassDarwin Dionisio ClementeNo ratings yet

- For Digitel RefundDocument1 pageFor Digitel RefundDarwin Dionisio ClementeNo ratings yet

- DPWH For Ped LaneDocument2 pagesDPWH For Ped LaneDarwin Dionisio ClementeNo ratings yet

- Choir Outing Letter 2015Document1 pageChoir Outing Letter 2015Darwin Dionisio ClementeNo ratings yet

- Collection Notice 2 (Tuition & Other Accounts)Document1 pageCollection Notice 2 (Tuition & Other Accounts)Darwin Dionisio ClementeNo ratings yet

- DIWA AccomodationDocument1 pageDIWA AccomodationDarwin Dionisio ClementeNo ratings yet

- A Night Tom Remember (Edited)Document1 pageA Night Tom Remember (Edited)Darwin Dionisio ClementeNo ratings yet

- Dep - Ed. - Report On PopulationDocument1 pageDep - Ed. - Report On PopulationDarwin Dionisio ClementeNo ratings yet

- Collection Notice 1 (Tuition Only)Document1 pageCollection Notice 1 (Tuition Only)Darwin Dionisio ClementeNo ratings yet

- Attention Followers-Epistle (Edited)Document1 pageAttention Followers-Epistle (Edited)Darwin Dionisio ClementeNo ratings yet

- Collection Letter (Latest)Document1 pageCollection Letter (Latest)Darwin Dionisio ClementeNo ratings yet

- Billboard Permit North HighlandDocument2 pagesBillboard Permit North HighlandDarwin Dionisio ClementeNo ratings yet

- Collection LetterDocument1 pageCollection LetterDarwin Dionisio ClementeNo ratings yet

- Criminals Out Zia (Edited)Document2 pagesCriminals Out Zia (Edited)Darwin Dionisio ClementeNo ratings yet

- Attention Followers-Epistle (Edited)Document1 pageAttention Followers-Epistle (Edited)Darwin Dionisio ClementeNo ratings yet

- Azkals: by Princess Pearl FetalberoDocument1 pageAzkals: by Princess Pearl FetalberoDarwin Dionisio ClementeNo ratings yet

- SCA ChoirDocument2 pagesSCA ChoirDarwin Dionisio ClementeNo ratings yet

- Azkals: by Princess Pearl FetalberoDocument1 pageAzkals: by Princess Pearl FetalberoDarwin Dionisio ClementeNo ratings yet

- Our Lady of The RosaryDocument1 pageOur Lady of The RosaryDarwin Dionisio ClementeNo ratings yet

- A Night Tom Remember (Edited)Document1 pageA Night Tom Remember (Edited)Darwin Dionisio ClementeNo ratings yet

- Maciprisa Winners For 2009Document1 pageMaciprisa Winners For 2009Darwin Dionisio ClementeNo ratings yet

- Basic Accounting Table of ContentsDocument2 pagesBasic Accounting Table of ContentsrynnaNo ratings yet

- Accounting ConceptsDocument32 pagesAccounting ConceptsSarika KeswaniNo ratings yet

- CPA Examinations Advanced AuditingDocument9 pagesCPA Examinations Advanced AuditingHaider BhaiNo ratings yet

- Dwnload Full Introduction To Financial Accounting 11th Edition Horngren Solutions Manual PDFDocument36 pagesDwnload Full Introduction To Financial Accounting 11th Edition Horngren Solutions Manual PDFgilmadelaurentis100% (14)

- Noorhidayu Binti OsmanDocument5 pagesNoorhidayu Binti OsmanNhidayu OsmanNo ratings yet

- Index MCQ Booklet: Audit MCQ Compiler by Shubham Keswani Shubham KeswaniDocument108 pagesIndex MCQ Booklet: Audit MCQ Compiler by Shubham Keswani Shubham Keswaniasd100% (2)

- Cash Flow Problem Solver - Depreciation, Taxes, NPV, IRRDocument45 pagesCash Flow Problem Solver - Depreciation, Taxes, NPV, IRRHannah Fuller100% (1)

- Aud Plan 123Document7 pagesAud Plan 123Mary GarciaNo ratings yet

- VOU Gallery Showcases Venkateshwara Open UniversityDocument74 pagesVOU Gallery Showcases Venkateshwara Open UniversitysancasnNo ratings yet

- Final Report - Payments ProcessDocument32 pagesFinal Report - Payments Processmrshami7754No ratings yet

- Super Project FinalDocument29 pagesSuper Project FinalSamuel ChuquistaNo ratings yet

- Cost Allocation and Activity-Based Costing: Financial and Managerial Accounting 8th Edition Warren Reeve FessDocument39 pagesCost Allocation and Activity-Based Costing: Financial and Managerial Accounting 8th Edition Warren Reeve FessRafif AjieNo ratings yet

- Bayan Telecommunications Holdings Corporation Fs 2006Document47 pagesBayan Telecommunications Holdings Corporation Fs 2006Pauline DyNo ratings yet

- SLA Part 9 - Create Subledger Accounting Method PDFDocument3 pagesSLA Part 9 - Create Subledger Accounting Method PDFsoireeNo ratings yet

- AuditingDocument8 pagesAuditingShahadath HossenNo ratings yet

- BFINDocument105 pagesBFINMuh AdnanNo ratings yet

- Sap Fi Transaction Codes List IDocument10 pagesSap Fi Transaction Codes List IJose Luis GonzalezNo ratings yet

- MeghaDocument1 pageMeghaMovie PostersNo ratings yet

- DAYA 2019 Annual ReportDocument192 pagesDAYA 2019 Annual Reportanggita nur kNo ratings yet

- Jam Althea O. Agner Prelec Output 1Document3 pagesJam Althea O. Agner Prelec Output 1JAM ALTHEA AGNERNo ratings yet

- Module 7 - Substantive Test and Documentation (Autosaved)Document32 pagesModule 7 - Substantive Test and Documentation (Autosaved)The Brain Dump PHNo ratings yet

- Register Disbursement & Billing SchemesDocument35 pagesRegister Disbursement & Billing SchemesHidayat KampaiNo ratings yet

- Guru Kirpa ArtsDocument8 pagesGuru Kirpa ArtsMeenu MittalNo ratings yet

- MGT402 MCQS Solved Papers Cost Management AccountingDocument669 pagesMGT402 MCQS Solved Papers Cost Management AccountingInternal AuditNo ratings yet

- Parle AuditDocument46 pagesParle AuditMukesh Manwani100% (1)

- International Scientific Conference Management 2016 Abstracts BelgradeDocument354 pagesInternational Scientific Conference Management 2016 Abstracts BelgradePredrag PetrovicNo ratings yet

- Partnership CE W Control Ans PDFDocument10 pagesPartnership CE W Control Ans PDFRedNo ratings yet

- Chapter 17Document48 pagesChapter 17Shiv NarayanNo ratings yet

- Test Bank Chapter10 Standard CostingDocument35 pagesTest Bank Chapter10 Standard Costingxxx101xxxNo ratings yet

- Oracle Financial Tables DescriptionDocument15 pagesOracle Financial Tables Descriptionrv90470No ratings yet