You might also like

- Virginia Business GuideDocument82 pagesVirginia Business GuidesshelkeNo ratings yet

- Making Money Out of Thin Air: Salesteamlive Special ReportDocument8 pagesMaking Money Out of Thin Air: Salesteamlive Special ReportThomas SettleNo ratings yet

- Business Law Presentation FINALDocument24 pagesBusiness Law Presentation FINALNur Liyana Izzati Roslan100% (1)

- Frequently Asked Questions - Corporations: Q. Can I Incorporate in More Than One State?Document3 pagesFrequently Asked Questions - Corporations: Q. Can I Incorporate in More Than One State?mpalenaNo ratings yet

- Essentials of a Promissory NoteDocument13 pagesEssentials of a Promissory NotePrashant MahawarNo ratings yet

- Chpater 5 - Banking SystemDocument10 pagesChpater 5 - Banking System21augustNo ratings yet

- Guide to Philippine Chattel Mortgage LawDocument5 pagesGuide to Philippine Chattel Mortgage LawApril Roween AranzaNo ratings yet

- Puerto Rico's Payday LoansDocument3 pagesPuerto Rico's Payday LoansRoosevelt Institute100% (3)

- Banking FinanceDocument9 pagesBanking FinanceAstik TripathiNo ratings yet

- American Monetary Institute: "Over Time, Whoever Controls The Money System Controls The Nation."Document2 pagesAmerican Monetary Institute: "Over Time, Whoever Controls The Money System Controls The Nation."Simply Debt SolutionsNo ratings yet

- Rem 7-6Document24 pagesRem 7-6Kevin JugaoNo ratings yet

- Purchase Agreement (Template)Document4 pagesPurchase Agreement (Template)RickNo ratings yet

- Collect Yourself: How To Extract Money From Tight-Fisted ClientsDocument5 pagesCollect Yourself: How To Extract Money From Tight-Fisted ClientsSalaam Bey®No ratings yet

- Negotiable Instrument: Differences From A ContractDocument8 pagesNegotiable Instrument: Differences From A ContractHikmah EdiNo ratings yet

- Module 1 Credit FundamentalsDocument24 pagesModule 1 Credit FundamentalsCaroline Grace Enteria Mella100% (1)

- Can Big Bank's President Rescind The ContractDocument6 pagesCan Big Bank's President Rescind The ContractSwathy SallaNo ratings yet

- Tutorial 050Document18 pagesTutorial 050Jason HenryNo ratings yet

- Borrower-In-Custody Program GuidelinesDocument16 pagesBorrower-In-Custody Program GuidelinesMichael FociaNo ratings yet

- Installment Loan Agreement: Itemization of Amount FinancedDocument1 pageInstallment Loan Agreement: Itemization of Amount FinancedaaNo ratings yet

- Investment Income and Expenses: (Including Capital Gains and Losses)Document76 pagesInvestment Income and Expenses: (Including Capital Gains and Losses)Kenny Svatek100% (1)

- DychesBoddiford LLCs As Rental PropertiesDocument8 pagesDychesBoddiford LLCs As Rental PropertiesREISkillsNo ratings yet

- Long-Term Bank LoanDocument12 pagesLong-Term Bank LoanAbidah Zulkifli100% (1)

- Purchase 500K Nitrile Gloves $4.5M AgreementDocument3 pagesPurchase 500K Nitrile Gloves $4.5M AgreementPedro Ant. Núñez UlloaNo ratings yet

- Vehicle Finance Financial Bubble WPDocument16 pagesVehicle Finance Financial Bubble WPAnkit SainiNo ratings yet

- Law of Contract PDFDocument28 pagesLaw of Contract PDFtemijohnNo ratings yet

- Impact Accounting, LLCDocument6 pagesImpact Accounting, LLCbarber bobNo ratings yet

- Adverse Selection & Moral HazardDocument4 pagesAdverse Selection & Moral HazardAJAY KUMAR SAHUNo ratings yet

- Corporate Owned Life InsuranceDocument12 pagesCorporate Owned Life InsuranceMartin McTaggartNo ratings yet

- Real Estate Prospecting Letter TemplatesDocument6 pagesReal Estate Prospecting Letter TemplatesShashi PalNo ratings yet

- Tutorial 030Document8 pagesTutorial 030Jason HenryNo ratings yet

- January 2007 Newsletter Http://preservingaylenlake - Blogspot.comDocument15 pagesJanuary 2007 Newsletter Http://preservingaylenlake - Blogspot.comEnvironmental EddyNo ratings yet

- Buy and Sell TimesharesDocument29 pagesBuy and Sell Timesharessterlingbeck2552100% (1)

- Church Kit: Don't Redefine Marriage. Vote NO On Question OneDocument18 pagesChurch Kit: Don't Redefine Marriage. Vote NO On Question OneG-A-YNo ratings yet

- How To Purchase A Foreclosure Property From PASDocument3 pagesHow To Purchase A Foreclosure Property From PASsin2begin2No ratings yet

- The Power of Income Layers (The Intrepid Way)Document2 pagesThe Power of Income Layers (The Intrepid Way)Matthew S. ChanNo ratings yet

- Insider Secrets of Online PokerDocument207 pagesInsider Secrets of Online PokercoultershaneNo ratings yet

- 2 Assignment: Department of Business AdministrationDocument14 pages2 Assignment: Department of Business AdministrationFarhan KhanNo ratings yet

- A BondDocument3 pagesA Bondnusra_t100% (1)

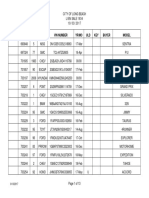

- Lien Sale Vehicles 2017Document13 pagesLien Sale Vehicles 2017camwills2No ratings yet

- NVC Tax Lien Invest in ReportDocument8 pagesNVC Tax Lien Invest in ReportJosh AlexanderNo ratings yet

- Secured Borrowing and A Sale of ReceivablesDocument1 pageSecured Borrowing and A Sale of Receivableswarsidi100% (1)

- Community Land Trust Technical Manual - 0Document482 pagesCommunity Land Trust Technical Manual - 0Peter McKownNo ratings yet

- Learning About BondsDocument12 pagesLearning About Bondshammy1480100% (1)

- 7 Smart Financial Steps To Take in 2016Document14 pages7 Smart Financial Steps To Take in 2016efsdfsdafsdNo ratings yet

- Presentation On Cheques: by Subrahmanya GSDocument12 pagesPresentation On Cheques: by Subrahmanya GSChaitra GsNo ratings yet

- Car Loan: Application FormDocument6 pagesCar Loan: Application FormVijay BhemalNo ratings yet

- Foreclosure Prevention Resource Guide Summer - Fall 2010Document56 pagesForeclosure Prevention Resource Guide Summer - Fall 2010Richarnellia-RichieRichBattiest-CollinsNo ratings yet

- Meaning of The LoanDocument26 pagesMeaning of The LoanHarmanjot Singh RiarNo ratings yet

- LeverageDocument38 pagesLeverageAnant MauryaNo ratings yet

- Home LoansDocument56 pagesHome LoansabhiNo ratings yet

- Secret Gardening HandbookDocument0 pagesSecret Gardening HandbookpudelhsdNo ratings yet

- SWF Example - BG Term Sheet First Time Buyer 28oct2013-1Document6 pagesSWF Example - BG Term Sheet First Time Buyer 28oct2013-1Malcolm WalkerNo ratings yet

- Clever Investor REI 101 GlossaryDocument24 pagesClever Investor REI 101 GlossaryMiguelNo ratings yet

- Guide To Understanding Credit GuideDocument11 pagesGuide To Understanding Credit GuideRobert Glen Murrell JrNo ratings yet

- Tutorial 020Document5 pagesTutorial 020Jason HenryNo ratings yet

- Auto1 PDFDocument211 pagesAuto1 PDFjamesbeaudoinNo ratings yet

- Law On PartnershipDocument55 pagesLaw On PartnershipYsabel ManiulitNo ratings yet

- AFFIDAVITDocument2 pagesAFFIDAVITAmit MandavilliNo ratings yet

- Court of Appeals erred in ruling tax credit basis for senior discountsDocument1 pageCourt of Appeals erred in ruling tax credit basis for senior discountsZydalgLadyz NeadNo ratings yet

- The Entering EsDocument95 pagesThe Entering Esthomas100% (1)

- Case Name: University of The Philippines College of LawDocument6 pagesCase Name: University of The Philippines College of LawYvette MoralesNo ratings yet

- Financial Management and AccountsDocument257 pagesFinancial Management and AccountsraggarwaNo ratings yet

- Change in Bank DetailDocument2 pagesChange in Bank Detailjha.sofcon5941No ratings yet

- CH 1 PDFDocument10 pagesCH 1 PDFVIjay S JariwalaNo ratings yet

- Audit Group 5 (Investment Audit and Cash Balance)Document12 pagesAudit Group 5 (Investment Audit and Cash Balance)feny febbianiNo ratings yet

- Earnings Per ShareDocument15 pagesEarnings Per ShareMuhammad SajidNo ratings yet

- Construction Bids and BondsDocument3 pagesConstruction Bids and BondsLaurence BarnesNo ratings yet

- Secret Bankers ManualDocument75 pagesSecret Bankers Manualhemanth00100% (9)

- Matling Industrial vs Coros (G.R. No. 157802 October 13, 2010Document2 pagesMatling Industrial vs Coros (G.R. No. 157802 October 13, 2010James WilliamNo ratings yet

- Disclosure Statement Pursuant To The Pink Basic Disclosure GuidelinesDocument24 pagesDisclosure Statement Pursuant To The Pink Basic Disclosure GuidelinesRenato GoncalvesNo ratings yet

- Equity Issue 2005 PDFDocument400 pagesEquity Issue 2005 PDFanon_299093230No ratings yet

- Salary Information - Asia: Banking & Financial Services - 2010Document4 pagesSalary Information - Asia: Banking & Financial Services - 2010Vicky OngNo ratings yet

- G.R. No. 205469 Bpi Family Savings Bank, Inc., Petitioner, St. Michael Medical Center, Inc., Respondent. Decision Perlas-Bernabe, J.Document61 pagesG.R. No. 205469 Bpi Family Savings Bank, Inc., Petitioner, St. Michael Medical Center, Inc., Respondent. Decision Perlas-Bernabe, J.Apling DincogNo ratings yet

- NRB Directives To Microfinance FIs, - 2074Document104 pagesNRB Directives To Microfinance FIs, - 2074NarayanPrajapatiNo ratings yet

- Functions of Financial SystemDocument2 pagesFunctions of Financial Systemrahulravi4u82% (51)

- Solution Maf653 - Dec 2019 - StudentDocument7 pagesSolution Maf653 - Dec 2019 - Studentdini ffNo ratings yet

- G.R. No. 180356: February 16, 2010Document18 pagesG.R. No. 180356: February 16, 2010Alyssa Clarizze MalaluanNo ratings yet

- Baobab Final Admission Doc Clean No CPRDocument161 pagesBaobab Final Admission Doc Clean No CPRAbhishek Ranjan SinghNo ratings yet

- Mutual Fund Unit 2Document30 pagesMutual Fund Unit 2Aman Chauhan100% (1)

- Problems and Prospects For Corporate Governance in BangladeshDocument3 pagesProblems and Prospects For Corporate Governance in BangladeshAtequr100% (2)

- Results Announcement For The Year of 2021 - Pnfu9cn2bfnnDocument142 pagesResults Announcement For The Year of 2021 - Pnfu9cn2bfnnPOLUX ALFREDO GARCIA CERDANo ratings yet

- Abrera v. BarzaDocument29 pagesAbrera v. BarzaangelieqNo ratings yet

- BankniftyDocument23 pagesBankniftyAditya MehtaNo ratings yet

- Cfap 1 Aafr PK PDFDocument312 pagesCfap 1 Aafr PK PDFMuhammad ShehzadNo ratings yet

- PROJECTED P& L Account and Balance SheetDocument7 pagesPROJECTED P& L Account and Balance SheetSimanchala DoraNo ratings yet

- Auditor Independence and Audit Quality PDFDocument22 pagesAuditor Independence and Audit Quality PDFadamNo ratings yet

- WORKSHEET Business FinanceDocument3 pagesWORKSHEET Business FinanceLuvnica VermaNo ratings yet