You might also like

- Property, Plant and EquipmentDocument8 pagesProperty, Plant and EquipmentMark John Malazo RiveraNo ratings yet

- Manage PPE AssetsDocument13 pagesManage PPE AssetsMich ClementeNo ratings yet

- Summary of IAS 16Document5 pagesSummary of IAS 16Laskar REAZNo ratings yet

- Chapter 09 Pas 16 PpeDocument9 pagesChapter 09 Pas 16 PpeJoelyn Grace MontajesNo ratings yet

- 12 PPE Part 1 With AnswersDocument13 pages12 PPE Part 1 With AnswersZatsumono YamamotoNo ratings yet

- FV provides transparency over historical costDocument3 pagesFV provides transparency over historical costHisham MalikNo ratings yet

- Ias 16 PropertyDocument6 pagesIas 16 PropertyAnjas A. M. TyasNo ratings yet

- Ias 16Document7 pagesIas 16Baqar BaigNo ratings yet

- IAS 16 SummaryDocument5 pagesIAS 16 SummarythenikkitrNo ratings yet

- These Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoDocument8 pagesThese Questions Help You Recognize Your Existing Background Knowledge On The Topic. Answer Honestly. Yes NoEki OmallaoNo ratings yet

- IAS 16 Accounting for Property, Plant and EquipmentDocument5 pagesIAS 16 Accounting for Property, Plant and EquipmentJoseph Gerald M. ArcegaNo ratings yet

- Summary of Pas 16 NDocument5 pagesSummary of Pas 16 NJenny Hermosado100% (1)

- IAS 16 PropertyDocument6 pagesIAS 16 PropertyMuhammad Salman RasheedNo ratings yet

- Accounting For PPEDocument4 pagesAccounting For PPEMaureen Derial PantaNo ratings yet

- ClassNotes IAS 16 PPEDocument2 pagesClassNotes IAS 16 PPEKhadejai LairdNo ratings yet

- SUMMARY OF IAS 16 PPE copyDocument3 pagesSUMMARY OF IAS 16 PPE copysecretary.feujpia2324No ratings yet

- Ias 16 Property Plant EquipmentDocument4 pagesIas 16 Property Plant Equipmentfaisal_zuhri100% (1)

- Ias 38Document43 pagesIas 38khan_ssNo ratings yet

- IAS 16 Overview: Accounting for Property, Plant and EquipmentDocument7 pagesIAS 16 Overview: Accounting for Property, Plant and Equipmentjustjade100% (1)

- IAS 16 Property, Plant and EquipmentDocument4 pagesIAS 16 Property, Plant and EquipmentSelva Bavani SelwaduraiNo ratings yet

- IAS-16 (Property, Plant & Equipment)Document20 pagesIAS-16 (Property, Plant & Equipment)Nazmul HaqueNo ratings yet

- Ias 16Document21 pagesIas 16Arshad BhuttaNo ratings yet

- Ias 16Document3 pagesIas 16Jhonalyn ZonioNo ratings yet

- Pas 16 Property, Plant and EquipmentDocument2 pagesPas 16 Property, Plant and Equipmentamber_harthartNo ratings yet

- Unit 1 and 2Document7 pagesUnit 1 and 2missyemylia27novNo ratings yet

- Ias 16Document7 pagesIas 16frieda20093835No ratings yet

- D5- Lê Trần Yến NhiDocument2 pagesD5- Lê Trần Yến Nhinhi lêNo ratings yet

- Theory of Accounting - SUMMARY of PPEDocument15 pagesTheory of Accounting - SUMMARY of PPESteven Chou100% (2)

- IAS 16 SummaryDocument7 pagesIAS 16 SummaryCharmaine LogaNo ratings yet

- Ias 16Document3 pagesIas 16CandyNo ratings yet

- IAS16Document2 pagesIAS16Atif RehmanNo ratings yet

- PP (A) - Lect 2 - Ias 16 PpeDocument19 pagesPP (A) - Lect 2 - Ias 16 Ppekevin digumberNo ratings yet

- IAS 16 Property Plant Equipment AccountingDocument6 pagesIAS 16 Property Plant Equipment AccountinghemantbaidNo ratings yet

- IAS 16 Property, Plant and Equipment GuideDocument35 pagesIAS 16 Property, Plant and Equipment GuideNimona BeyeneNo ratings yet

- Property, Plant and Equipment: By:-Yohannes Negatu (Acca, Dipifr)Document37 pagesProperty, Plant and Equipment: By:-Yohannes Negatu (Acca, Dipifr)Eshetie Mekonene AmareNo ratings yet

- Technical SummaryDocument2 pagesTechnical Summarysza_13100% (2)

- PAS 16: Property, Plant and EquipmentDocument21 pagesPAS 16: Property, Plant and EquipmentJoseph Gerald M. ArcegaNo ratings yet

- IFRS 6 EXPLORATION & EVALUATIONDocument8 pagesIFRS 6 EXPLORATION & EVALUATIONJoelyn Grace MontajesNo ratings yet

- Unit 1 - IAS 16: Property, Plant and Equipment Objective: Advanced Financial ReportingDocument18 pagesUnit 1 - IAS 16: Property, Plant and Equipment Objective: Advanced Financial ReportingRobin G'koolNo ratings yet

- Ias 16 PropertyDocument11 pagesIas 16 PropertyFolarin EmmanuelNo ratings yet

- Submitted By: - Muhammad Abdul Wahab Registeration No: 241 SUBMITTED TO: Madam Uzma Azam - Assignment No: 03 DATE OF SUBMISSION: 28-05-2021Document5 pagesSubmitted By: - Muhammad Abdul Wahab Registeration No: 241 SUBMITTED TO: Madam Uzma Azam - Assignment No: 03 DATE OF SUBMISSION: 28-05-2021Abdul WahabNo ratings yet

- Week 10 - 02 - Module 23 - Property, Plant & Equipment (Part 2)Document10 pagesWeek 10 - 02 - Module 23 - Property, Plant & Equipment (Part 2)지마리No ratings yet

- PPE HandoutsDocument6 pagesPPE Handoutsashish.mathur1No ratings yet

- IAS16 Defines Property, Plant and Equipment As "Tangible Items ThatDocument35 pagesIAS16 Defines Property, Plant and Equipment As "Tangible Items ThatMo HachimNo ratings yet

- Ias 16Document9 pagesIas 16ADEYANJU AKEEMNo ratings yet

- IAS 1 Presentation of Financial StatementsDocument74 pagesIAS 1 Presentation of Financial StatementsCandyNo ratings yet

- 07 PPE Cost s19Document35 pages07 PPE Cost s19Nosipho NyathiNo ratings yet

- Property, Plant and Equipment Are Tangible Items ThatDocument2 pagesProperty, Plant and Equipment Are Tangible Items ThatnasirNo ratings yet

- IAS 16 Property, Plant and Equipment GuideDocument5 pagesIAS 16 Property, Plant and Equipment GuideANURAG NairNo ratings yet

- Accounting Standard SWGDocument6 pagesAccounting Standard SWGAbhijit RoyNo ratings yet

- Ias 16 Property Plant Equipment v1 080713Document7 pagesIas 16 Property Plant Equipment v1 080713Phebieon MukwenhaNo ratings yet

- IAS 16 Property, Plant and Equipment GuideDocument12 pagesIAS 16 Property, Plant and Equipment Guideaditya pandianNo ratings yet

- 0915 IAS 16 Property Plant and Equipment Lecture Notes (Student Copy)Document13 pages0915 IAS 16 Property Plant and Equipment Lecture Notes (Student Copy)蔡易憬No ratings yet

- Ques. 1. Peterlee (A) - Purpose and Authoritative Status of The FrameworkDocument7 pagesQues. 1. Peterlee (A) - Purpose and Authoritative Status of The FrameworkJulet Harris-TopeyNo ratings yet

- Nepal Accounting Standards On Property, Plant and Equipment: Initial Cost 11 Subsequent Cost 12-14Document24 pagesNepal Accounting Standards On Property, Plant and Equipment: Initial Cost 11 Subsequent Cost 12-14Gemini_0804No ratings yet

- TA07b - Current AssetsDocument11 pagesTA07b - Current AssetsMarsha Sabrina LillahNo ratings yet

- BA 114.1 Handout On PPEDocument5 pagesBA 114.1 Handout On PPEHuarde SophiaNo ratings yet

- Mega Project Assurance: Volume One - The Terminological DictionaryFrom EverandMega Project Assurance: Volume One - The Terminological DictionaryNo ratings yet

- Industry Analysis TopicsDocument5 pagesIndustry Analysis TopicsShah KamalNo ratings yet

- F3 StudyText CIMA Kaplan 2015 Ver2 PDFDocument434 pagesF3 StudyText CIMA Kaplan 2015 Ver2 PDFShah Kamal100% (2)

- Summary - Differences Currency RM TechniquesDocument1 pageSummary - Differences Currency RM TechniquesShah KamalNo ratings yet

- Financial Instrument-Recogniton, MeasurementDocument60 pagesFinancial Instrument-Recogniton, MeasurementShah KamalNo ratings yet

- IAS#16Document17 pagesIAS#16Shah KamalNo ratings yet

- CIMA F3 SyllabusDocument8 pagesCIMA F3 SyllabusShah KamalNo ratings yet

- 15 Toughest Interview Questions and Answers!: 1. Why Do You Want To Work in This Industry?Document8 pages15 Toughest Interview Questions and Answers!: 1. Why Do You Want To Work in This Industry?johnlemNo ratings yet

- Project Stages - PlanningDocument20 pagesProject Stages - PlanningShah KamalNo ratings yet

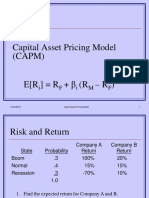

- Capital Asset Pricing ModelDocument25 pagesCapital Asset Pricing ModelShah KamalNo ratings yet

- Conceptual FrameworksDocument17 pagesConceptual FrameworksShah KamalNo ratings yet

- Chapter 5: Revenue (IAS 18) and Construction Contracts (IAS 11) MMPA - 501 Financial AccountingDocument50 pagesChapter 5: Revenue (IAS 18) and Construction Contracts (IAS 11) MMPA - 501 Financial AccountingShah KamalNo ratings yet

- Revenue and Its MeasurementDocument42 pagesRevenue and Its MeasurementShah KamalNo ratings yet

- Ifrs 8Document11 pagesIfrs 8TasminNo ratings yet

- IAS#38Document43 pagesIAS#38Shah KamalNo ratings yet

- Financial Instrument ClassificationDocument43 pagesFinancial Instrument ClassificationShah KamalNo ratings yet

- Ias 23Document18 pagesIas 23Shah KamalNo ratings yet

- Accounting Theory - Joint Conceptual Framework.Document15 pagesAccounting Theory - Joint Conceptual Framework.Shah KamalNo ratings yet

- Ias#32. 39 Ifrs 7Document38 pagesIas#32. 39 Ifrs 7Shah KamalNo ratings yet

- IAS 11 - Construction ContractDocument13 pagesIAS 11 - Construction ContractShah KamalNo ratings yet

- IFRS 5 Assets Held for Sale and Discontinued OpsDocument14 pagesIFRS 5 Assets Held for Sale and Discontinued OpsShah Kamal100% (1)

- Recent Changes in FASB FrameworkDocument6 pagesRecent Changes in FASB FrameworkShah KamalNo ratings yet

- IAS08Document29 pagesIAS08Shah KamalNo ratings yet

- IAS07Document22 pagesIAS073tsdu13No ratings yet

- IAS 19 - Employee BenefitDocument49 pagesIAS 19 - Employee BenefitShah Kamal100% (2)

- IAS#36Document31 pagesIAS#36Shah KamalNo ratings yet

- Ias 34Document11 pagesIas 34Shah Kamal100% (1)

- Calculate Zurich's taxable income and income taxes payable for 2007Document31 pagesCalculate Zurich's taxable income and income taxes payable for 2007Shah KamalNo ratings yet

- Ias 37Document22 pagesIas 37Shah KamalNo ratings yet

- Present Value TableDocument1 pagePresent Value TableShah KamalNo ratings yet

- (Final) Quiz Statement of Changes in Equity and Cash Flows Word FileDocument3 pages(Final) Quiz Statement of Changes in Equity and Cash Flows Word FileAyanna CameroNo ratings yet

- Preparing A Multiple Step Income StatementDocument2 pagesPreparing A Multiple Step Income StatementCyril Joseph ViernesNo ratings yet

- The Accounting EquationDocument4 pagesThe Accounting EquationMargo Williams100% (1)

- Module Sample ShsDocument8 pagesModule Sample ShsJoke JoNo ratings yet

- Advanced Corporate Reporting: Professional 2 Examination - November 2020Document16 pagesAdvanced Corporate Reporting: Professional 2 Examination - November 2020Issa BoyNo ratings yet

- Syllabus - Periyar UniversityDocument50 pagesSyllabus - Periyar UniversityShriHemaRajaNo ratings yet

- Deferred TaxDocument3 pagesDeferred Taxমোঃ মাহফুজুর রহমান রাকিবNo ratings yet

- Proposed DividebdDocument34 pagesProposed DividebdPiyush SrivastavaNo ratings yet

- Request For Personal Travel Abroad: Commonwealth Avenue, Quezon CityDocument5 pagesRequest For Personal Travel Abroad: Commonwealth Avenue, Quezon CityJonson PalmaresNo ratings yet

- Manufacturing Account Worked Example Question 7Document4 pagesManufacturing Account Worked Example Question 7Roshan Ramkhalawon100% (1)

- Auditing Theory Answer Key 6Document3 pagesAuditing Theory Answer Key 6Jasper GicaNo ratings yet

- Invoice SampleDocument1 pageInvoice SampleRinaldy ReiNo ratings yet

- Advanced Financial Accounting & Reporting Business CombinationDocument12 pagesAdvanced Financial Accounting & Reporting Business CombinationJunel PlanosNo ratings yet

- Siklus AkuntansiDocument15 pagesSiklus AkuntansiBachrul AlamNo ratings yet

- Liquidation ReportDocument3 pagesLiquidation Reportkabataansulong2023No ratings yet

- IFRS Framework ConflictsDocument16 pagesIFRS Framework ConflictsMJ YaconNo ratings yet

- Test Bank For Intermediate Accounting 17th Edition SticeDocument13 pagesTest Bank For Intermediate Accounting 17th Edition SticeLawrence Gardin100% (32)

- Auditing and Assurance Services in Australia 7th Edition Gay Test BankDocument41 pagesAuditing and Assurance Services in Australia 7th Edition Gay Test Bankpoulderduefulu1a4vy100% (26)

- Final Exam - Ae14 CfasDocument7 pagesFinal Exam - Ae14 CfasVillanueva RosemarieNo ratings yet

- FAR08.01d-Presentation of Financial StatementsDocument7 pagesFAR08.01d-Presentation of Financial StatementsANGELRIEH SUPERTICIOSONo ratings yet

- Capability - Table New (5) 20190825073712 (2) 20191229131437Document1 pageCapability - Table New (5) 20190825073712 (2) 20191229131437Varikuppala SrikanthNo ratings yet

- Essentials of Accounting For Governmental and Not For Profit Organizations 13th Edition Ebook PDFDocument41 pagesEssentials of Accounting For Governmental and Not For Profit Organizations 13th Edition Ebook PDFkaty.wilkins325100% (32)

- Partnership PracticeDocument1 pagePartnership PracticeIce Voltaire Buban GuiangNo ratings yet

- (Materi 5) Audit Utang Jangka Panjang - Pengujian Substantif Terhadap Utang Jangka PanjangDocument5 pages(Materi 5) Audit Utang Jangka Panjang - Pengujian Substantif Terhadap Utang Jangka PanjangFendy ArisyandanaNo ratings yet

- GAAS GAADocument13 pagesGAAS GAAshudayeNo ratings yet

- Khuram Cement TuanaDocument115 pagesKhuram Cement TuanaZeeshan ChaudhryNo ratings yet

- Ch13 DISCLOSURE PRINCIPLESDocument6 pagesCh13 DISCLOSURE PRINCIPLESralphalonzoNo ratings yet

- Martin Corporat-WPS OfficeDocument3 pagesMartin Corporat-WPS Officelaica valderasNo ratings yet

- Practice Exam Chapter 1-3Document5 pagesPractice Exam Chapter 1-3Renz Paul MirandaNo ratings yet

- Bayan Telecommunications Holdings Corporation Fs 2006Document47 pagesBayan Telecommunications Holdings Corporation Fs 2006Pauline DyNo ratings yet