You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Lectures 8 and 10Document30 pagesLectures 8 and 10maria fernNo ratings yet

- Advance AuditingDocument36 pagesAdvance Auditingmaria fernNo ratings yet

- ENG2012 GEN2010 Unit 1Document88 pagesENG2012 GEN2010 Unit 1maria fernNo ratings yet

- Lectures 4 and 5Document7 pagesLectures 4 and 5maria fernNo ratings yet

- Financial Statement Analysis: K.R. SubramanyamDocument45 pagesFinancial Statement Analysis: K.R. Subramanyammaria fernNo ratings yet

- ACY4401 Advanced Taxation Lecture 3 International Aspects of Current Hong Kong Taxation Law and Practice 1. Double Taxation Agreement ("DTA")Document13 pagesACY4401 Advanced Taxation Lecture 3 International Aspects of Current Hong Kong Taxation Law and Practice 1. Double Taxation Agreement ("DTA")maria fernNo ratings yet

- Financial Statement Analysis: K.R. SubramanyamDocument48 pagesFinancial Statement Analysis: K.R. SubramanyamCarolina SuryajayaNo ratings yet

- Lecture 3Document31 pagesLecture 3maria fernNo ratings yet

- Financial Statement Analysis: K.R. SubramanyamDocument49 pagesFinancial Statement Analysis: K.R. Subramanyammaria fernNo ratings yet

- Eng 2012Document69 pagesEng 2012maria fernNo ratings yet

- Week 13b - Stylistic DevicesDocument8 pagesWeek 13b - Stylistic Devicesmaria fernNo ratings yet

- Lectures 8 and 10Document30 pagesLectures 8 and 10maria fernNo ratings yet

- Lecture 2Document42 pagesLecture 2maria fernNo ratings yet

- Lecture 3Document31 pagesLecture 3maria fernNo ratings yet

- Writing Mobile MessagesDocument3 pagesWriting Mobile Messagesmaria fernNo ratings yet

- Advance Financial ReportingDocument101 pagesAdvance Financial Reportingmaria fernNo ratings yet

- Business Law Notes - AllDocument56 pagesBusiness Law Notes - Allmaria fernNo ratings yet

- Lecture 2Document7 pagesLecture 2maria fernNo ratings yet

- 7 Employment LawDocument4 pages7 Employment Lawmaria fernNo ratings yet

- 3 Literal RuleDocument1 page3 Literal Rulemaria fernNo ratings yet

- Week 13 Exercise With AnswersDocument10 pagesWeek 13 Exercise With Answersmaria fernNo ratings yet

- Pre-Test 1 Review Exercise - AnswersDocument6 pagesPre-Test 1 Review Exercise - Answersmaria fernNo ratings yet

- Purchase Payment Exercise-Answers ASIDocument3 pagesPurchase Payment Exercise-Answers ASImaria fernNo ratings yet

- ACY 3201 Pre-FinalDocument8 pagesACY 3201 Pre-Finalmaria fernNo ratings yet

- Purchase Payment Exercise-Answers ASIDocument3 pagesPurchase Payment Exercise-Answers ASImaria fernNo ratings yet

- Answers - Chapter 6-2Document17 pagesAnswers - Chapter 6-2maria fernNo ratings yet

- Pre-Test 1 Review Exercise - AnswersDocument6 pagesPre-Test 1 Review Exercise - Answersmaria fernNo ratings yet

- ACY 3801 AnswerDocument5 pagesACY 3801 Answermaria fernNo ratings yet

- Internal Controls for Inventory and Cash ReceiptsDocument6 pagesInternal Controls for Inventory and Cash Receiptsmaria fernNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- SHS Entrepreneurship 2nd PT 2023 2024 Test QuestionsDocument5 pagesSHS Entrepreneurship 2nd PT 2023 2024 Test Questionscarlo deguzmanNo ratings yet

- Corporate Level StrategyDocument33 pagesCorporate Level StrategyDave NamakhwaNo ratings yet

- Sample Ctos Score Report CompanyDocument3 pagesSample Ctos Score Report Companyhwyap2022No ratings yet

- Financial Markets and Services: Unit 1Document12 pagesFinancial Markets and Services: Unit 1Saumya SinghNo ratings yet

- Cost of Capital Final Ppt1Document12 pagesCost of Capital Final Ppt1Mehul ShuklaNo ratings yet

- MCD 2023 Annual ReportDocument73 pagesMCD 2023 Annual ReportsherbicepsNo ratings yet

- Notes To Interim Finacial StatementsDocument7 pagesNotes To Interim Finacial StatementsJhoanna Marie Manuel-AbelNo ratings yet

- S4Hana - New Asset Accounting in 2020 VersionDocument104 pagesS4Hana - New Asset Accounting in 2020 VersionBhargav ReddyNo ratings yet

- SubtitleDocument2 pagesSubtitleBlack LotusNo ratings yet

- Bankruptcy and Restructuring at Marvel Entertainment GroupDocument12 pagesBankruptcy and Restructuring at Marvel Entertainment Groupvikaskumar_mech89200% (2)

- Sahil Bhadviya's Answer To Should I Invest in Mutual Funds or Share Market - QuoraDocument4 pagesSahil Bhadviya's Answer To Should I Invest in Mutual Funds or Share Market - QuoraSam vermNo ratings yet

- Nism Sorm NotesDocument25 pagesNism Sorm NotesdikpalakNo ratings yet

- Awareness Among The Traders About The Settlement of Online TradingDocument13 pagesAwareness Among The Traders About The Settlement of Online TradingElson Antony PaulNo ratings yet

- CA Inter Accounts A MTP 1 Nov 2022Document13 pagesCA Inter Accounts A MTP 1 Nov 2022smartshivenduNo ratings yet

- Cash Flow Statement and AnalysisDocument2 pagesCash Flow Statement and Analysisaashidua15gmailcomNo ratings yet

- Operating and Financial LeverageDocument64 pagesOperating and Financial LeverageMohammad AtherNo ratings yet

- Emerging Markets Derivatives Activity Reduces FX ExposureDocument36 pagesEmerging Markets Derivatives Activity Reduces FX Exposurevan7911No ratings yet

- Inventories of Manufacturing Concern. A Trading Concern Is One That Buys and Sells Goods inDocument6 pagesInventories of Manufacturing Concern. A Trading Concern Is One That Buys and Sells Goods inleare ruazaNo ratings yet

- 4.2 Costs, Scale of Production and Break-Even AnalysisDocument10 pages4.2 Costs, Scale of Production and Break-Even Analysisgeneva conventionsNo ratings yet

- Financial Analysis Model:: Enter Data in Black Cells Are Computer GeneratedDocument2 pagesFinancial Analysis Model:: Enter Data in Black Cells Are Computer GeneratedAnkit ChaudharyNo ratings yet

- (Bank of America) Hybrid ARM MBS - Valuation and Risk MeasuresDocument22 pages(Bank of America) Hybrid ARM MBS - Valuation and Risk Measures00aaNo ratings yet

- Lesson 11 International Aspects of Corporate FinanceDocument17 pagesLesson 11 International Aspects of Corporate Financeman ibe0% (1)

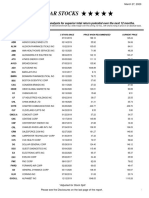

- Five Star StocksDocument5 pagesFive Star StocksJeff SturgeonNo ratings yet

- Literature Review On Goodwill ImpairmentDocument45 pagesLiterature Review On Goodwill Impairmentmahgoub2005100% (1)

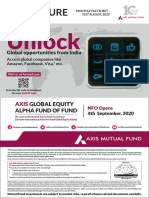

- Axis Asset Management Company LimitedDocument73 pagesAxis Asset Management Company LimitedMohammad MushtaqNo ratings yet

- Conceptual Framework Underlying Assumption - Going Concern: Based On The Information I Have Collected AboutDocument9 pagesConceptual Framework Underlying Assumption - Going Concern: Based On The Information I Have Collected AboutshazNo ratings yet

- Suggested Answers:: Answer: 1, 2 and 4Document7 pagesSuggested Answers:: Answer: 1, 2 and 4Huệ LêNo ratings yet

- Evaluate Cost-Cutting Automation ProposalDocument5 pagesEvaluate Cost-Cutting Automation ProposalĐặng Thuỳ HươngNo ratings yet

- Paper - Iii Commerce: Note: Attempt All The Questions. Each Question Carries Two (2) MarksDocument26 pagesPaper - Iii Commerce: Note: Attempt All The Questions. Each Question Carries Two (2) MarksashaNo ratings yet

- Acct224 Samuel TanDocument4 pagesAcct224 Samuel TanSonia NgNo ratings yet