You might also like

- Economic Developments and Investment Environment in TurkeyDocument30 pagesEconomic Developments and Investment Environment in TurkeyPolat ArıNo ratings yet

- Special Section3Document14 pagesSpecial Section3Adil IshaqueNo ratings yet

- World Economic IndicatorsDocument3 pagesWorld Economic IndicatorsSteveTillNo ratings yet

- GS-Asia Outlook 2023 PDFDocument12 pagesGS-Asia Outlook 2023 PDFJNo ratings yet

- Description: Tags: Lingenfelter-PresentDocument3 pagesDescription: Tags: Lingenfelter-Presentanon-451214No ratings yet

- Recent Trends in World Trade: by Alain Henriot Delegate Director Coe-Rexecode (Paris)Document20 pagesRecent Trends in World Trade: by Alain Henriot Delegate Director Coe-Rexecode (Paris)Yashfeen FalakNo ratings yet

- ICICI Prudential Banking and Financial Services Final PresentationDocument25 pagesICICI Prudential Banking and Financial Services Final PresentationDrashti Investments100% (3)

- Lecture 4 Agriculture SectorDocument27 pagesLecture 4 Agriculture SectorShiwani BalaniNo ratings yet

- Behind the Food Crisis in India and the Global SouthDocument26 pagesBehind the Food Crisis in India and the Global SouthAnqur1984No ratings yet

- Industry Outlook March2011Document4 pagesIndustry Outlook March2011iminvisibleNo ratings yet

- Team Gangs of Fms - MWR - FmsDocument33 pagesTeam Gangs of Fms - MWR - FmsBharat DhootNo ratings yet

- Malaysia - Economic Trends: Gross Domestic ProductDocument5 pagesMalaysia - Economic Trends: Gross Domestic ProductyuiclynesNo ratings yet

- Analyst Meeting - 1H 2018 PerformanceDocument23 pagesAnalyst Meeting - 1H 2018 PerformanceLennyNo ratings yet

- Nippon Paint Group Medium-Term Plan (FY2021-2023) Update ReportDocument36 pagesNippon Paint Group Medium-Term Plan (FY2021-2023) Update ReportRahiNo ratings yet

- Lecture 4 Agriculture SectorDocument25 pagesLecture 4 Agriculture SectorYumna HasnainNo ratings yet

- Daily Trading Stance - 2009-07-03Document2 pagesDaily Trading Stance - 2009-07-03Trading FloorNo ratings yet

- Oklahoma Budget Trends and Outlook (Rev. Jan 13, 2010)Document39 pagesOklahoma Budget Trends and Outlook (Rev. Jan 13, 2010)dblattokNo ratings yet

- Real Estate: Pre-Sales Recovery Augurs WellDocument3 pagesReal Estate: Pre-Sales Recovery Augurs WellsudhakarrrrrrNo ratings yet

- Sokkelaret 2017 Engelsk PresentasjonDocument25 pagesSokkelaret 2017 Engelsk PresentasjonHải Thân NgọcNo ratings yet

- Monetary Policy in Extraordinary Times: SlidesDocument16 pagesMonetary Policy in Extraordinary Times: SlidescreditplumberNo ratings yet

- What Is The Economic Outlook For OECD Countries?: An Interim AssessmentDocument17 pagesWhat Is The Economic Outlook For OECD Countries?: An Interim AssessmentJohn RotheNo ratings yet

- M&A Finance TrendsDocument51 pagesM&A Finance TrendsPaul GhanimehNo ratings yet

- Evolution of indias industrial sectorDocument11 pagesEvolution of indias industrial sectorSabeer VcNo ratings yet

- The Supply Chain Challenge: Procurement The "Apache Way"Document18 pagesThe Supply Chain Challenge: Procurement The "Apache Way"awscobie100% (1)

- Daily Trading Stance - 2009-10-20Document3 pagesDaily Trading Stance - 2009-10-20Trading FloorNo ratings yet

- Earnings Call 3Q2018Document22 pagesEarnings Call 3Q2018Scriptlance 2012No ratings yet

- Crisi - Conde RuizDocument17 pagesCrisi - Conde RuiznoisefromamerikaNo ratings yet

- Netra Early Warnings Signals Through Charts - May 2022Document16 pagesNetra Early Warnings Signals Through Charts - May 2022Adhiraj MukherjeeNo ratings yet

- Forecast For US Oil and Gas Production (Laherrère & Hall 2018)Document24 pagesForecast For US Oil and Gas Production (Laherrère & Hall 2018)Cliffhanger100% (3)

- The Rise of Intangible Investments and The Implications For InvestorsDocument34 pagesThe Rise of Intangible Investments and The Implications For InvestorsLaurent MilletNo ratings yet

- Economic Forecast ColombiaDocument3 pagesEconomic Forecast Colombiasuper_sumoNo ratings yet

- Byju's Company Analysis and Growth StrategyDocument5 pagesByju's Company Analysis and Growth StrategyYashvendra RawatNo ratings yet

- Template 04 Financial ProjectionsDocument338 pagesTemplate 04 Financial Projectionsokymk13No ratings yet

- Trade Integration in Latin America and the Caribbean: Opportunities and ChallengesDocument10 pagesTrade Integration in Latin America and the Caribbean: Opportunities and Challengessteve britoNo ratings yet

- Monitoring Kegiatan BulananDocument7 pagesMonitoring Kegiatan BulananSyafrullahNo ratings yet

- Vietnam and The Global Value Chain: FIGURE 2.1. Export-Led Growth and Poverty Reduction, 1992-2017Document1 pageVietnam and The Global Value Chain: FIGURE 2.1. Export-Led Growth and Poverty Reduction, 1992-2017hnmjzhviNo ratings yet

- MPRA Paper 85549Document31 pagesMPRA Paper 85549Zeeshan AshrafNo ratings yet

- BGC MatrixDocument3 pagesBGC MatrixFritz IgnacioNo ratings yet

- Oklahoma Budget Overview: Trends and Outlook (May 12, 2010)Document44 pagesOklahoma Budget Overview: Trends and Outlook (May 12, 2010)dblattokNo ratings yet

- 4Q2020 Fullbook enDocument39 pages4Q2020 Fullbook enVincentNo ratings yet

- Corpres Bbni Am-1h-2019 PDFDocument40 pagesCorpres Bbni Am-1h-2019 PDFRadiSujadi24041977No ratings yet

- The Australian Economy and Financial Markets: July 2019Document33 pagesThe Australian Economy and Financial Markets: July 2019Amita SinghNo ratings yet

- SaaS Financial Model 3.0 ExcelDocument367 pagesSaaS Financial Model 3.0 Excelმექანიკური ფორთოხალიNo ratings yet

- PN Co PresentationDocument57 pagesPN Co PresentationFernando De Juan Ruíz-Montalvo Perez de AragónNo ratings yet

- Midcap Monitor November 2019 HighlightsDocument27 pagesMidcap Monitor November 2019 HighlightsSudhir ShastriNo ratings yet

- Tata Chemicals Limited AGMDocument20 pagesTata Chemicals Limited AGMRakesh VaidyanathanNo ratings yet

- Asia StrategyDocument21 pagesAsia StrategySouvia RahimahNo ratings yet

- Impact of The Global Slowdown On Developing CountriesDocument14 pagesImpact of The Global Slowdown On Developing CountriesNANDUTHECHAMPNo ratings yet

- Phil Knowledge 4Q2015Document12 pagesPhil Knowledge 4Q2015Kareen Ann RanteNo ratings yet

- Lenders of Last Resort in A Globalized World: Maurice ObstfeldDocument16 pagesLenders of Last Resort in A Globalized World: Maurice Obstfeldapi-26091012No ratings yet

- Paper 4Document35 pagesPaper 4UMT JournalsNo ratings yet

- SUBEXLTD - Investor Presentation - 01-Feb-22 - TickertapeDocument37 pagesSUBEXLTD - Investor Presentation - 01-Feb-22 - TickertapeleoharshadNo ratings yet

- UTI Nifty 200 Momentum 30 Index Fund - V1 - 2 (1) 20210217-061307Document1 pageUTI Nifty 200 Momentum 30 Index Fund - V1 - 2 (1) 20210217-061307RavishankarNo ratings yet

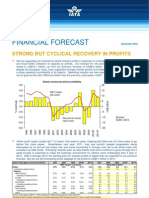

- STRONG BUT CYCLICAL RECOVERY IN AIRLINE PROFITS FORECASTDocument4 pagesSTRONG BUT CYCLICAL RECOVERY IN AIRLINE PROFITS FORECASTDaniel WongNo ratings yet

- Daily Trading Stance - 2009-10-15Document3 pagesDaily Trading Stance - 2009-10-15Trading FloorNo ratings yet

- Business Strategy For The Petrochemicals & Plastics Sector: October 8, 2015Document36 pagesBusiness Strategy For The Petrochemicals & Plastics Sector: October 8, 2015afs araeNo ratings yet

- Budget Presentation: Budget For The Year 2018Document15 pagesBudget Presentation: Budget For The Year 2018Arif IslamNo ratings yet

- Stock Market Briefing: Bear Market Indicators: Yardeni Research, IncDocument6 pagesStock Market Briefing: Bear Market Indicators: Yardeni Research, IncgfernandezvNo ratings yet

- Kalim A. Siddiqui, Byco Petroleum. Petroleum Retail Market in PakistanDocument41 pagesKalim A. Siddiqui, Byco Petroleum. Petroleum Retail Market in PakistansyedqamarNo ratings yet

- Bret Polfuss - Resume 2021Document2 pagesBret Polfuss - Resume 2021api-533858450No ratings yet

- Risk Mitigation and Vulnerability Assessment of Nam Dok Mai Mango (Mangifera Indica L.cv. Nam Dok Mai) Supply Chain Using Rapid Agricultural Supply Chain Risk Assessment (RapAgRisk)Document8 pagesRisk Mitigation and Vulnerability Assessment of Nam Dok Mai Mango (Mangifera Indica L.cv. Nam Dok Mai) Supply Chain Using Rapid Agricultural Supply Chain Risk Assessment (RapAgRisk)Dhiyaa Ulhaq RikavianiNo ratings yet

- PAPER REFERENCE LIST JAschDocument1 pagePAPER REFERENCE LIST JAschehtesabiNo ratings yet

- Feasibility Study TBBDocument12 pagesFeasibility Study TBBtryasihNo ratings yet

- Ridi Antyaningrum - KapulagaDocument8 pagesRidi Antyaningrum - KapulagaridiantyaningrumNo ratings yet

- Indian Textile Industry: Opportunities, Challenges and SuggestionsDocument5 pagesIndian Textile Industry: Opportunities, Challenges and Suggestionsgizex2013No ratings yet

- Identifying proportional and non-proportional relationships in tablesDocument4 pagesIdentifying proportional and non-proportional relationships in tablesEllen Marie PackNo ratings yet

- PLC & BCG matrix analysis of AsianPaintsDocument11 pagesPLC & BCG matrix analysis of AsianPaintsNeeraj PrajapatNo ratings yet

- 8 Waste Down TimeDocument1 page8 Waste Down TimeAbassNo ratings yet

- Module 9 - The WorksheetDocument13 pagesModule 9 - The WorksheetNina AlexineNo ratings yet

- Housing loan details and documentsDocument2 pagesHousing loan details and documentsArun PrasadNo ratings yet

- BP Ruminants2 Ummb2Document6 pagesBP Ruminants2 Ummb2Ronnie NaagNo ratings yet

- Uruba Wheat and Teff farm proposal highlights key detailsDocument27 pagesUruba Wheat and Teff farm proposal highlights key detailsAbayneh ErkaloNo ratings yet

- Directorio Maquiladoras 2009Document4 pagesDirectorio Maquiladoras 2009Angel ReynaNo ratings yet

- Chapter 1: Overview: (Difficulty: E Easy, M Medium, H Hard)Document5 pagesChapter 1: Overview: (Difficulty: E Easy, M Medium, H Hard)yebegashetNo ratings yet

- The Evolution of Banking in IndiaDocument5 pagesThe Evolution of Banking in IndiaCyril ChettiarNo ratings yet

- Starting A Winery in Ontario: Publication 815Document108 pagesStarting A Winery in Ontario: Publication 815Nab TorNo ratings yet

- E - 01 - 06 - 07 - 39 - 42 - Pragya Trivedi PDFDocument21 pagesE - 01 - 06 - 07 - 39 - 42 - Pragya Trivedi PDFTabrej AlamNo ratings yet

- INVESTMENT GUIDE Skopje Region - Infrastructure, Resources & OpportunitiesDocument348 pagesINVESTMENT GUIDE Skopje Region - Infrastructure, Resources & OpportunitiesMonika TanushevskaNo ratings yet

- Performance Evaluation of Self Propelled Vertical Conveyor ReaperDocument6 pagesPerformance Evaluation of Self Propelled Vertical Conveyor ReaperPrashant NaleNo ratings yet

- Sale of Goods Act ExplainedDocument147 pagesSale of Goods Act ExplainedKhairun Nasuha Binti Mohamad Tahir A20B2134No ratings yet

- 1-BMCG2323 Introduction To ManufacturingDocument56 pages1-BMCG2323 Introduction To Manufacturinghemarubini96100% (1)

- Executive Chairman Corporate InformationDocument9 pagesExecutive Chairman Corporate InformationnoreenNo ratings yet

- Quality Wireless (A) ... KEL153Document6 pagesQuality Wireless (A) ... KEL153Amit Admune0% (1)

- Official Gazette Regulations on Insurance IntermediariesDocument142 pagesOfficial Gazette Regulations on Insurance Intermediariespacs0% (1)

- Make Jose A. GalarzaDocument3 pagesMake Jose A. GalarzaAlex G StollNo ratings yet

- Petra Capital Research Note Peer Next Door Valued 8x MoreDocument5 pagesPetra Capital Research Note Peer Next Door Valued 8x MoretgitoenebNo ratings yet

- WalmartDocument7 pagesWalmart1921 Pallav PaliNo ratings yet

- Spring 2022 Mudpuppy CatalogDocument30 pagesSpring 2022 Mudpuppy CatalogChronicleBooksNo ratings yet

- Kiran Mazumdar Shaw: India's Biotech QueenDocument13 pagesKiran Mazumdar Shaw: India's Biotech QueenRising RevolutionaryNo ratings yet