You might also like

- Figures of Speech ExplainedDocument5 pagesFigures of Speech ExplainedDarenJayBalboa100% (1)

- Economics and The Theory of Games - Vega-Redondo PDFDocument526 pagesEconomics and The Theory of Games - Vega-Redondo PDFJaime Andrés67% (3)

- Module 1-3 ACCTG 201Document32 pagesModule 1-3 ACCTG 201Sky SoronoiNo ratings yet

- Writing Simple Sentences to Describe ScenariosDocument5 pagesWriting Simple Sentences to Describe Scenariosepol67% (3)

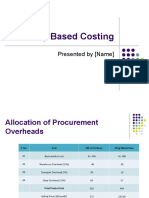

- SCM - Deep Dive Cost PlanningDocument19 pagesSCM - Deep Dive Cost PlanningSrinivasa Rao AsuruNo ratings yet

- New Japa Retreat NotebookDocument48 pagesNew Japa Retreat NotebookRob ElingsNo ratings yet

- Chap.13 Guerrero Job Order CostingDocument40 pagesChap.13 Guerrero Job Order CostingGeoff MacarateNo ratings yet

- Design of Self - Supporting Dome RoofsDocument6 pagesDesign of Self - Supporting Dome RoofszatenneNo ratings yet

- Science Web 2014Document40 pagesScience Web 2014Saif Shahriar0% (1)

- 7 Tools for Continuous ImprovementDocument202 pages7 Tools for Continuous Improvementvivekanand bhartiNo ratings yet

- TelanganaDocument16 pagesTelanganaRamu Palvai0% (1)

- Department of Education Doña Asuncion Lee Integrated School: Division of Mabalacat CityDocument2 pagesDepartment of Education Doña Asuncion Lee Integrated School: Division of Mabalacat CityRica Tano50% (2)

- Manual de Instruções Iveco Eurocargo Euro 6Document226 pagesManual de Instruções Iveco Eurocargo Euro 6rsp filmes100% (1)

- Activity Based Costing-A Tool To Aid Decision MakingDocument54 pagesActivity Based Costing-A Tool To Aid Decision MakingSederiku KabaruzaNo ratings yet

- Activity Based Costing:: A Tool To Aid Decision MakingDocument28 pagesActivity Based Costing:: A Tool To Aid Decision MakingAlbana QemaliNo ratings yet

- Activity Based Costing OmairDocument26 pagesActivity Based Costing OmairblablaNo ratings yet

- Adobe Scan 02-Feb-2022Document4 pagesAdobe Scan 02-Feb-2022Khyati PatelNo ratings yet

- ABC Costing Sample Prob 2nd SetDocument1 pageABC Costing Sample Prob 2nd SetJhanna LarananNo ratings yet

- Activity-Based Costing: A Tool To Aid Decision MakingDocument29 pagesActivity-Based Costing: A Tool To Aid Decision MakingAce RividiNo ratings yet

- Activity-Based CostingDocument49 pagesActivity-Based CostingJene LmNo ratings yet

- Garrison Lecture Chapter 7Document64 pagesGarrison Lecture Chapter 7jeanette100% (1)

- Job Order Costing ReviewerDocument40 pagesJob Order Costing RevieweraidanNo ratings yet

- 3 Classification of Cost CMA Inter Costing Fast Track ClassDocument18 pages3 Classification of Cost CMA Inter Costing Fast Track ClassLeviNo ratings yet

- Systems Design-Process CostingDocument58 pagesSystems Design-Process CostingSederiku KabaruzaNo ratings yet

- PDF Ramas Lingisiticas Griega e Italica - CompressDocument18 pagesPDF Ramas Lingisiticas Griega e Italica - CompressSALDIERNA OLGUIN LIZBETHNo ratings yet

- Idle Capacity and Management: BE PresentationDocument15 pagesIdle Capacity and Management: BE PresentationBhawna GosainNo ratings yet

- Activity Based Costing/Management: Mgr. Andrea Gažová, PHDDocument23 pagesActivity Based Costing/Management: Mgr. Andrea Gažová, PHDRoberto SanchezNo ratings yet

- Managerial Accounting Chap 008 Power PointDocument75 pagesManagerial Accounting Chap 008 Power PointYasmine MagdiNo ratings yet

- Cost TerminologyDocument24 pagesCost TerminologyAqib AliNo ratings yet

- ZCMA6022 Activity Based CostingDocument56 pagesZCMA6022 Activity Based CostingIlanchelian ChandranNo ratings yet

- ABC and Cost Management SystemsDocument48 pagesABC and Cost Management SystemsR.ArumugamNo ratings yet

- Job Order CostingDocument2 pagesJob Order CostingEms TeopeNo ratings yet

- Overhead PPTDocument19 pagesOverhead PPTHemant bhanawatNo ratings yet

- Activity Based CostingDocument14 pagesActivity Based CostingHarsh PratapNo ratings yet

- Chapter 2 - Cost and Cost ClassificationDocument12 pagesChapter 2 - Cost and Cost ClassificationVuong PhamNo ratings yet

- Managerial Accounting Managerial AccountingDocument30 pagesManagerial Accounting Managerial Accountingpvsk17072005No ratings yet

- Garrison Lecture Chapter 7Document64 pagesGarrison Lecture Chapter 7Novel LiaNo ratings yet

- Activity-Based Costing (Abc)Document3 pagesActivity-Based Costing (Abc)colNo ratings yet

- Activity-Based Costing: A Tool To Aid Decision MakingDocument54 pagesActivity-Based Costing: A Tool To Aid Decision MakingAdamme AbhirajNo ratings yet

- Activity Based Costing A Tool To Aid Decision MakingDocument18 pagesActivity Based Costing A Tool To Aid Decision Makingshahidameen2No ratings yet

- ACCOUNTING 2 EBOOK Topic 4Document9 pagesACCOUNTING 2 EBOOK Topic 4hanafikmnNo ratings yet

- Review Chapter 1-2-4-18Document55 pagesReview Chapter 1-2-4-18hoangmyduyennguyen2004No ratings yet

- CostDocument7 pagesCostHara KimNo ratings yet

- Activity Based CostingDocument12 pagesActivity Based CostingMuhammad Imran AwanNo ratings yet

- Cost & Managerial Accounting FundamentalsDocument2 pagesCost & Managerial Accounting Fundamentalsjumper200No ratings yet

- Job Order Costing - Hand OutDocument6 pagesJob Order Costing - Hand OutKorinth BalaoNo ratings yet

- Activity-Based Costing Explained for Improved Product CostingDocument29 pagesActivity-Based Costing Explained for Improved Product CostingRommel RoyceNo ratings yet

- Exam Notes CIMA-P2-Advanced-Management-AccountingDocument4 pagesExam Notes CIMA-P2-Advanced-Management-AccountinghannahjpickNo ratings yet

- P2 MA Cheet Sheet PDFDocument2 pagesP2 MA Cheet Sheet PDFbooks_sumiNo ratings yet

- Chapter 2Document5 pagesChapter 2Hania M. CalandadaNo ratings yet

- Basic Cost Concept - Garrison BCL03Document41 pagesBasic Cost Concept - Garrison BCL03Dhyon YunazarNo ratings yet

- 11 Edition: Mcgraw-Hill/IrwinDocument48 pages11 Edition: Mcgraw-Hill/IrwinArlene Magalang NatividadNo ratings yet

- Cost Concepts Classification BehaviorDocument46 pagesCost Concepts Classification BehaviorrhearomefranciscoNo ratings yet

- Management Accounting Chapter 5&6Document84 pagesManagement Accounting Chapter 5&6yimerNo ratings yet

- Absorption Costing, Marginal CostingDocument29 pagesAbsorption Costing, Marginal Costinggopeshtripathi786No ratings yet

- Property, Plant, and Equipment and Intangible Assets: Utilization and ImpairmentDocument53 pagesProperty, Plant, and Equipment and Intangible Assets: Utilization and ImpairmentSara LimNo ratings yet

- Activity-Based Costing vs Traditional CostingDocument21 pagesActivity-Based Costing vs Traditional CostingKrishna RaiNo ratings yet

- Chap06 Manufacturing ProcessesDocument13 pagesChap06 Manufacturing ProcessesRanbir KapoorNo ratings yet

- Activity Based Costing: Mcgraw-Hill /irwinDocument53 pagesActivity Based Costing: Mcgraw-Hill /irwinsaraNo ratings yet

- تلخيص شابتر 8 محاسبةDocument1 pageتلخيص شابتر 8 محاسبةMariam SalahNo ratings yet

- 2 CMA CostSystemsDocument28 pages2 CMA CostSystemsBushra FatimaNo ratings yet

- Topic 8b Project Cost Control Rev. - 352Document26 pagesTopic 8b Project Cost Control Rev. - 352Riad El AbedNo ratings yet

- Topic 06 - Activity-Based Costing - Cost and Management Accounting Course Notes 2021 PWC Conversion ProgrammeDocument52 pagesTopic 06 - Activity-Based Costing - Cost and Management Accounting Course Notes 2021 PWC Conversion ProgrammejerrymaNo ratings yet

- Chapter 4 OverheadDocument21 pagesChapter 4 OverheadMUHAMMAD ZAIM HAMZI MUHAMMAD ZINNo ratings yet

- Accounting cases cost systems behavior costsDocument28 pagesAccounting cases cost systems behavior costsKrishna RaiNo ratings yet

- absorption and marginalDocument7 pagesabsorption and marginalshafinasimanNo ratings yet

- Hilton 04Document19 pagesHilton 04JavierNo ratings yet

- Session 4 ADM SharedDocument29 pagesSession 4 ADM Sharedum23394No ratings yet

- Bab 2 - Perilaku BiayaDocument40 pagesBab 2 - Perilaku BiayaAndy ReynaldyyNo ratings yet

- 03 Seatwork 1 ProjectManagement SenisRachelDocument2 pages03 Seatwork 1 ProjectManagement SenisRachelRachel SenisNo ratings yet

- How To Install Windows XP From Pen Drive Step by Step GuideDocument3 pagesHow To Install Windows XP From Pen Drive Step by Step GuideJithendra Kumar MNo ratings yet

- AMB4520R0v06: Antenna SpecificationsDocument2 pagesAMB4520R0v06: Antenna SpecificationsЕвгений ГрязевNo ratings yet

- Kanavos Pharmaceutical Distribution Chain 2007 PDFDocument121 pagesKanavos Pharmaceutical Distribution Chain 2007 PDFJoao N Da SilvaNo ratings yet

- Vonovia 9M2021 Presentation 20211118Document76 pagesVonovia 9M2021 Presentation 20211118LorenzoNo ratings yet

- F&B Data Analyst Portfolio ProjectDocument12 pagesF&B Data Analyst Portfolio ProjectTom HollandNo ratings yet

- Institutional Competency Assessment Instrument (ICAI)Document12 pagesInstitutional Competency Assessment Instrument (ICAI)Bea EtacNo ratings yet

- Falling Weight Deflectometer Bowl Parameters As Analysis Tool For Pavement Structural EvaluationsDocument18 pagesFalling Weight Deflectometer Bowl Parameters As Analysis Tool For Pavement Structural EvaluationsEdisson Eduardo Valencia Gomez100% (1)

- 4 Exploring Your Personality Q and Scoring Key (Transaction Analysis)Document3 pages4 Exploring Your Personality Q and Scoring Key (Transaction Analysis)Tarannum Yogesh DobriyalNo ratings yet

- Manual EDocument12 pagesManual EKrum KashavarovNo ratings yet

- Science SimulationsDocument4 pagesScience Simulationsgk_gbuNo ratings yet

- Loverpreet Chapterv 1Document16 pagesLoverpreet Chapterv 1Sheikh SiddiquiNo ratings yet

- Potato Peroxidase LabDocument2 pagesPotato Peroxidase LabKarla GutierrezNo ratings yet

- Robotic End Effectors - Payload Vs Grip ForceDocument8 pagesRobotic End Effectors - Payload Vs Grip ForcesamirNo ratings yet

- 02 - Order Quantities When Demand Is Approximately LevelDocument2 pages02 - Order Quantities When Demand Is Approximately Levelrahma.samyNo ratings yet

- Simulated Robot Football Team Uses Neural Networks to LearnDocument8 pagesSimulated Robot Football Team Uses Neural Networks to LearnKishore MuthukulathuNo ratings yet

- PPC2000 Association of Consultant Architects Standard Form of Project Partnering ContractDocument5 pagesPPC2000 Association of Consultant Architects Standard Form of Project Partnering ContractJoy CeeNo ratings yet

- How To Oven and Sun Dry Meat and ProduceDocument12 pagesHow To Oven and Sun Dry Meat and ProduceLes BennettNo ratings yet

- Electronics HubDocument9 pagesElectronics HubKumaran SgNo ratings yet

- Ultimate Guide To Construction SubmittalsDocument10 pagesUltimate Guide To Construction SubmittalsDavid ConroyNo ratings yet