You might also like

- Element of CostDocument16 pagesElement of CostcwarekhaNo ratings yet

- Mutual Funds IndustryDocument36 pagesMutual Funds IndustryMaster HusainNo ratings yet

- Options Strategies Model PaperDocument11 pagesOptions Strategies Model PaperAshish Singh100% (1)

- Book BuildingDocument10 pagesBook BuildingSaad Mahmood100% (1)

- Selective Inventory Control for Construction ProjectsDocument5 pagesSelective Inventory Control for Construction ProjectsPinak ShomeNo ratings yet

- DerivativesDocument77 pagesDerivativesDr.P. Siva Ramakrishna100% (2)

- Workbook On Derivatives PDFDocument84 pagesWorkbook On Derivatives PDFsapnaofsnehNo ratings yet

- Green Shoe OptionDocument15 pagesGreen Shoe OptionNadeem Ahmad100% (1)

- Derivatives ManagementDocument13 pagesDerivatives ManagementMaharajascollege KottayamNo ratings yet

- Principles of Option PricingDocument23 pagesPrinciples of Option Pricingcharansap100% (1)

- Pitambari rural distribution strategiesDocument13 pagesPitambari rural distribution strategiesSiddharth GautamNo ratings yet

- 2 - Integrated L&SCMDocument1 page2 - Integrated L&SCMsukumaran321No ratings yet

- Adr GDR IdrDocument19 pagesAdr GDR IdrRachit MadhukarNo ratings yet

- AFM Lecture 11Document24 pagesAFM Lecture 11Alseraj TechnologyNo ratings yet

- MAC Costing ReportDocument10 pagesMAC Costing ReportRohanNo ratings yet

- Evaluation of EDPDocument33 pagesEvaluation of EDPKiran Gujamagadi100% (1)

- Services Marketing, LICDocument107 pagesServices Marketing, LICअंजनी श्रीवास्तवNo ratings yet

- Module 2-EDDocument26 pagesModule 2-EDNikhil RankaNo ratings yet

- Competitor Analysis: Learn Strategies for Understanding Competitors & CustomersDocument21 pagesCompetitor Analysis: Learn Strategies for Understanding Competitors & Customersmail2joe70% (1)

- Dr. Sharan Shetty PHD (Banking & Finance) Mba (Finance) B. Com (Hons)Document54 pagesDr. Sharan Shetty PHD (Banking & Finance) Mba (Finance) B. Com (Hons)Nagesh Pai MysoreNo ratings yet

- Bond valuation and yield analysisDocument35 pagesBond valuation and yield analysisTanmay MehtaNo ratings yet

- Benefits of Depository SystemDocument4 pagesBenefits of Depository SystemAnkush VermaNo ratings yet

- Customer & Trade PromotionDocument8 pagesCustomer & Trade PromotionAnkita ThukralNo ratings yet

- Nism X B Caselet 7Document8 pagesNism X B Caselet 7Finware 1No ratings yet

- Savings and Investment in IndiaDocument20 pagesSavings and Investment in Indianenu_10071% (7)

- 02 Product DecisionDocument38 pages02 Product DecisionJemima Christelle EkraNo ratings yet

- ElasticityDocument68 pagesElasticityARKAJYOTI SAHANo ratings yet

- Motives ofDocument9 pagesMotives ofYogesh BatraNo ratings yet

- GST Assignments For B.com 6TH Sem PDFDocument4 pagesGST Assignments For B.com 6TH Sem PDFAnujyadav Monuyadav100% (1)

- Derivatives: Fundamentals and OverviewDocument72 pagesDerivatives: Fundamentals and OverviewAmit SinhaNo ratings yet

- Sector Analysis Capstone (Rohan Pandita)Document17 pagesSector Analysis Capstone (Rohan Pandita)Rohan PanditaNo ratings yet

- How Swaps Work: An Overview of the Different Types of SwapsDocument3 pagesHow Swaps Work: An Overview of the Different Types of SwapsJohana ReyesNo ratings yet

- QH Talbros 1Document60 pagesQH Talbros 1Rekha MathpalNo ratings yet

- Sources of FinanceDocument53 pagesSources of Financejessica0% (1)

- Marketing in Indian EconomyDocument15 pagesMarketing in Indian Economyshivakumar NNo ratings yet

- Study and Reviewing The Financial Statements of The Kingfisher AirlinesDocument14 pagesStudy and Reviewing The Financial Statements of The Kingfisher AirlinesAhmad BashaNo ratings yet

- Bought Out Deals ExplainedDocument8 pagesBought Out Deals ExplainedF12 keshav yogiNo ratings yet

- ERP Implementation at Shiv Shakti Gas AgencyDocument10 pagesERP Implementation at Shiv Shakti Gas Agencyshraddha shahNo ratings yet

- L2 DRM - PricingDocument58 pagesL2 DRM - PricingAjay Gansinghani100% (1)

- Hypothetical Capital Structure and Cost of Capital of Mahindra Finance Services LTDDocument25 pagesHypothetical Capital Structure and Cost of Capital of Mahindra Finance Services LTDlovels_agrawal6313No ratings yet

- Fama's Decomposition of Return AnalysisDocument5 pagesFama's Decomposition of Return AnalysisPriyanka AgarwalNo ratings yet

- Non-Linear Pricing: Reference - Marketing Analytics Wayne L WinstonDocument9 pagesNon-Linear Pricing: Reference - Marketing Analytics Wayne L Winstonarunmittal1985No ratings yet

- Derivatives CIA 3 - Christ UniversityDocument10 pagesDerivatives CIA 3 - Christ UniversityRNo ratings yet

- A Comparative Analysis of Mutual Fund SchemesDocument9 pagesA Comparative Analysis of Mutual Fund SchemesVimal SaxenaNo ratings yet

- Regulatory On Derivatives (1) (From Shodhganga)Document70 pagesRegulatory On Derivatives (1) (From Shodhganga)sharathNo ratings yet

- of 8 Financial SectorDocument22 pagesof 8 Financial Sectorsreetam.edevlopNo ratings yet

- Swot Analysis of Asset Classes: OpportunitiesDocument8 pagesSwot Analysis of Asset Classes: OpportunitiesAnjali KanwarNo ratings yet

- Fundamentals of insurance terminology explainedDocument16 pagesFundamentals of insurance terminology explainedFaye Nandini SalinsNo ratings yet

- Financial Service Promotional (Strategy Icici Bank)Document51 pagesFinancial Service Promotional (Strategy Icici Bank)goodwynj100% (2)

- Dabur 3Document46 pagesDabur 3yuktim67% (3)

- Discount and Finance House of IndiaDocument25 pagesDiscount and Finance House of Indiavikram_bansal_5No ratings yet

- Strategic Analysis of Asian Paints-1Document17 pagesStrategic Analysis of Asian Paints-1Shishir MaheshwariNo ratings yet

- A Project Report On Marketing MixDocument7 pagesA Project Report On Marketing Mixvandana220% (1)

- Hedge RatioDocument12 pagesHedge RatioFazal Wahab100% (1)

- Classification & Prediction with Naive BayesDocument19 pagesClassification & Prediction with Naive BayesQamaNo ratings yet

- Mutual Fund GuideDocument14 pagesMutual Fund GuideMukesh Kumar SinghNo ratings yet

- Exotic Options: - Kamya 17118Document22 pagesExotic Options: - Kamya 17118Amit SinghNo ratings yet

- Graham3e ppt08Document38 pagesGraham3e ppt08Lim Yu ChengNo ratings yet

- Damodaran PDFDocument89 pagesDamodaran PDFWirastio RahmatsyahNo ratings yet

- BasicsofoptionsDocument19 pagesBasicsofoptionsmurthy1234567No ratings yet

- Secondary Markets ExplainedDocument27 pagesSecondary Markets ExplainedNhi VõNo ratings yet

- Financial Statements of BMW AgDocument52 pagesFinancial Statements of BMW AgSimranNo ratings yet

- Shares and Bonds Are Float in ?: (A) Money MarketDocument16 pagesShares and Bonds Are Float in ?: (A) Money MarketMurad AliNo ratings yet

- Happiest Minds Share Price - Google SearchDocument1 pageHappiest Minds Share Price - Google SearchYadav ShailendraNo ratings yet

- Ind As 33 Material For VC 26 28 August 2021Document69 pagesInd As 33 Material For VC 26 28 August 2021Khawaish MittalNo ratings yet

- A Comparative Analysis of Theperformance o FAfrican Capital Market Volume 2 2010Document81 pagesA Comparative Analysis of Theperformance o FAfrican Capital Market Volume 2 2010NiladriAcholNo ratings yet

- Strategic Financial Management - Investment Appraisal - RCF, PP, DPP, TVM, ARR - Dayana MasturaDocument23 pagesStrategic Financial Management - Investment Appraisal - RCF, PP, DPP, TVM, ARR - Dayana MasturaDayana MasturaNo ratings yet

- Balance Sheet: Annual DataDocument4 pagesBalance Sheet: Annual DataJulie RayanNo ratings yet

- Accounting Module 2 AnswerDocument5 pagesAccounting Module 2 AnswerMariel Mae MoralesNo ratings yet

- CH 1 QaDocument5 pagesCH 1 QaAhmad Tawfiq DarabsehNo ratings yet

- Case2 Group2Document11 pagesCase2 Group2Yang ZhouNo ratings yet

- MindTree Balance Sheet Summary 2011-2007Document4 pagesMindTree Balance Sheet Summary 2011-2007shraddhamalNo ratings yet

- Direct Tax Ca FinalDocument10 pagesDirect Tax Ca FinalGaurav GaurNo ratings yet

- Case Study - ACI and Marico BDDocument9 pagesCase Study - ACI and Marico BDsadekjakeNo ratings yet

- 【寶塔個經私藏筆記】Ch1Economic ModelsDocument4 pages【寶塔個經私藏筆記】Ch1Economic Models黃譯民No ratings yet

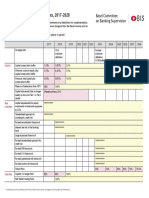

- Basel III transitional arrangements 2017-2028 summaryDocument1 pageBasel III transitional arrangements 2017-2028 summarygoonNo ratings yet

- Overview of Financial Statement Analysis: Mcgraw-Hill/Irwin ©2007, The Mcgraw-Hill Companies, All Rights ReservedDocument45 pagesOverview of Financial Statement Analysis: Mcgraw-Hill/Irwin ©2007, The Mcgraw-Hill Companies, All Rights ReservedMutiara RamadhaniNo ratings yet

- Financial Reporting (FR) Mar / June 2021 Examiner's ReportDocument24 pagesFinancial Reporting (FR) Mar / June 2021 Examiner's ReportKeong ShengNo ratings yet

- Business Valuation Using Financial Statements (BVFS) Prof. Vaidya Nathan Term 6, February 2022Document242 pagesBusiness Valuation Using Financial Statements (BVFS) Prof. Vaidya Nathan Term 6, February 2022Anurag JainNo ratings yet

- Dilemma - Mohamed HassanDocument66 pagesDilemma - Mohamed HassanMohammed HassanNo ratings yet

- Notes For Week 2Document3 pagesNotes For Week 2algokar999No ratings yet

- Icici Securities Internship ReportDocument33 pagesIcici Securities Internship ReportDhanush.RNo ratings yet

- Case On UTV Software Communications LTDDocument5 pagesCase On UTV Software Communications LTDShail MalviyaNo ratings yet

- True or False Conceptual Framework Set 2Document2 pagesTrue or False Conceptual Framework Set 2Demi Pardillo100% (1)

- Group Work #1 With SolutionsDocument3 pagesGroup Work #1 With SolutionsShadi MorakabatiNo ratings yet

- Dividend and Determinants of Dividend PolicyDocument3 pagesDividend and Determinants of Dividend PolicyAmit PandeyNo ratings yet

- Financial Statement Analysis: K.R. SubramanyamDocument50 pagesFinancial Statement Analysis: K.R. SubramanyamDaveli NatanaelNo ratings yet

- Project 2 Nse BseDocument12 pagesProject 2 Nse BseIshita BansalNo ratings yet

- Technical Rooms DetailDocument24 pagesTechnical Rooms Detailconsultnadeem70No ratings yet

- The Use of Technical and Fundamental Analysis Kumar NaveenDocument296 pagesThe Use of Technical and Fundamental Analysis Kumar Naveensmeena100% (1)