You might also like

- BFC5935 - Tutorial 10 SolutionsDocument8 pagesBFC5935 - Tutorial 10 SolutionsAlex YisnNo ratings yet

- Samnidhy Faq'sDocument4 pagesSamnidhy Faq'sSourav DharNo ratings yet

- 7.4 Options - Pricing Model - Black ScholesDocument36 pages7.4 Options - Pricing Model - Black ScholesSiva SankarNo ratings yet

- Capital Market Theory: An OverviewDocument38 pagesCapital Market Theory: An OverviewdevinamisraNo ratings yet

- Rose Mwaniki CVDocument10 pagesRose Mwaniki CVHamid RazaNo ratings yet

- CryptocurrencyDocument19 pagesCryptocurrencySonu SainiNo ratings yet

- Foundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsFrom EverandFoundational Theories and Techniques for Risk Management, A Guide for Professional Risk Managers in Financial Services - Part II - Financial InstrumentsNo ratings yet

- FIN 413 - Midterm #2 SolutionsDocument6 pagesFIN 413 - Midterm #2 SolutionsWesley CheungNo ratings yet

- The Correlation Structure of Security Returns: Multiindex Models and Grouping TechniquesDocument26 pagesThe Correlation Structure of Security Returns: Multiindex Models and Grouping TechniquessaminbdNo ratings yet

- Techniques For Managing ExposureDocument26 pagesTechniques For Managing Exposureprasanthgeni22100% (1)

- Financial Statement Analysis PPT 3427Document25 pagesFinancial Statement Analysis PPT 3427imroz_alamNo ratings yet

- Presentation Insurance PPTDocument11 pagesPresentation Insurance PPTshuchiNo ratings yet

- Investment Management Unit 1Document12 pagesInvestment Management Unit 1Fahadhtm MoosanNo ratings yet

- IFRS 12 disclosure guide for interests in other entitiesDocument3 pagesIFRS 12 disclosure guide for interests in other entitiesAira Nhaira MecateNo ratings yet

- Fundamental Analysis GuideDocument12 pagesFundamental Analysis GuidezaryNo ratings yet

- Chapter 7 Portfolio Theory: Prepared By: Wael Shams EL-DinDocument21 pagesChapter 7 Portfolio Theory: Prepared By: Wael Shams EL-DinmaheraldamatiNo ratings yet

- Cost of CapitalDocument55 pagesCost of CapitalSaritasaruNo ratings yet

- T1 Introduction (Answer)Document5 pagesT1 Introduction (Answer)Wen Kai YeamNo ratings yet

- Global Capital Market & Their EffectsDocument22 pagesGlobal Capital Market & Their EffectsJay KoliNo ratings yet

- Markowitz TheoryDocument4 pagesMarkowitz TheoryshahrukhziaNo ratings yet

- Lecture 4 Index Models 4.1 Markowitz Portfolio Selection ModelDocument34 pagesLecture 4 Index Models 4.1 Markowitz Portfolio Selection ModelL SNo ratings yet

- SYBBIDocument13 pagesSYBBIshekhar landageNo ratings yet

- Arbitrage Pricing TheoryDocument10 pagesArbitrage Pricing TheoryarmailgmNo ratings yet

- Capital Asset Pricing ModelDocument4 pagesCapital Asset Pricing ModelGeorge Ayesa Sembereka Jr.No ratings yet

- Cost of Capital, WACC and BetaDocument3 pagesCost of Capital, WACC and BetaSenith111No ratings yet

- 46370bosfinal p2 cp6 PDFDocument85 pages46370bosfinal p2 cp6 PDFgouri khanduallNo ratings yet

- Black Scholes Model ReportDocument6 pagesBlack Scholes Model ReportminhalNo ratings yet

- Understanding Non-Banking Financial Companies (NBFCsDocument31 pagesUnderstanding Non-Banking Financial Companies (NBFCssagarkharpatilNo ratings yet

- Security Analysis: Chapter - 1Document47 pagesSecurity Analysis: Chapter - 1Harsh GuptaNo ratings yet

- International FinanceDocument56 pagesInternational FinanceSucheta Das100% (1)

- Security Analysis and Portfolio ManagementDocument31 pagesSecurity Analysis and Portfolio ManagementAnubhav SonyNo ratings yet

- FE 445 M1 CheatsheetDocument5 pagesFE 445 M1 Cheatsheetsaya1990No ratings yet

- Bankruptcy Prediction Models-ArtikelDocument5 pagesBankruptcy Prediction Models-ArtikelLjiljana SorakNo ratings yet

- Indian Financial System: FunctionsDocument31 pagesIndian Financial System: Functionsmedha jaiwantNo ratings yet

- Markowitz Portfolio Theory IIIDocument12 pagesMarkowitz Portfolio Theory IIIShafiq Khan100% (1)

- CHP 1 - Introduction To Merchant BankingDocument44 pagesCHP 1 - Introduction To Merchant BankingFalguni MathewsNo ratings yet

- Security Analysis - IntroductionDocument20 pagesSecurity Analysis - IntroductionAnanya Ghosh100% (1)

- Introduction To Financial ManagemntDocument29 pagesIntroduction To Financial ManagemntibsNo ratings yet

- Construction of The Optimal PortfolioDocument4 pagesConstruction of The Optimal PortfolioRavi KhatriNo ratings yet

- Chapter 13 Return, Risk and Security Market LineDocument44 pagesChapter 13 Return, Risk and Security Market LineFahmi Ahmad FarizanNo ratings yet

- Bond Portfolio MGTDocument22 pagesBond Portfolio MGTChandrabhan NathawatNo ratings yet

- CocDocument47 pagesCocUmesh ChandraNo ratings yet

- Introduction To Risk and ReturnDocument59 pagesIntroduction To Risk and ReturnGaurav AgarwalNo ratings yet

- Derivatives Markets: Futures, Options & SwapsDocument20 pagesDerivatives Markets: Futures, Options & SwapsPatrick Earl T. PintacNo ratings yet

- e 51 F 8 F 8 B 4 A 32 Ea 4Document159 pagese 51 F 8 F 8 B 4 A 32 Ea 4Shawn Kou100% (5)

- Revenue (Sales) XXX (-) Variable Costs XXXDocument10 pagesRevenue (Sales) XXX (-) Variable Costs XXXNageshwar SinghNo ratings yet

- Operationalizing Capm ModelDocument3 pagesOperationalizing Capm ModelFahim Ali Khan100% (1)

- Characteristics of The Money MarketDocument8 pagesCharacteristics of The Money Marketshubhmeshram2100No ratings yet

- Market Risk MeasurementDocument19 pagesMarket Risk MeasurementRohit SinghNo ratings yet

- Assignment 1 - Investment AnalysisDocument5 pagesAssignment 1 - Investment Analysisphillimon zuluNo ratings yet

- CAPM TheoryDocument11 pagesCAPM TheoryNishakdasNo ratings yet

- 1.2 Doc-20180120-Wa0002Document23 pages1.2 Doc-20180120-Wa0002Prachet KulkarniNo ratings yet

- Financial Statement Analysis (Fsa)Document32 pagesFinancial Statement Analysis (Fsa)Shashank100% (1)

- Security Analysis & Portfolio Management Syllabus MBA III SemDocument1 pageSecurity Analysis & Portfolio Management Syllabus MBA III SemViraja GuruNo ratings yet

- Arbitage TheoryDocument9 pagesArbitage Theorymahesh19689No ratings yet

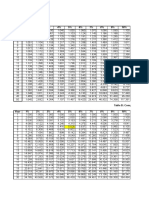

- Fvifa Tables 2Document2 pagesFvifa Tables 2Alexia100% (3)

- CH 3 Test Bank الاسايمنت جا من هناDocument36 pagesCH 3 Test Bank الاسايمنت جا من هناNTNNo ratings yet

- COM 6 (B) of 96th AIBBDocument2 pagesCOM 6 (B) of 96th AIBBShamima AkterNo ratings yet

- Calculate Annuity and Perpetuity Present ValuesDocument17 pagesCalculate Annuity and Perpetuity Present ValuesJericho AguirreNo ratings yet

- Beta - Calculations PDFDocument3 pagesBeta - Calculations PDFRebecca Ann SajiNo ratings yet

- Risk Management - c1Document33 pagesRisk Management - c1nana hahaNo ratings yet

- Chapter 6 - AnnuityDocument19 pagesChapter 6 - Annuitynurfatimah473No ratings yet

- Fin 460-HW 4 Adianto JoelDocument7 pagesFin 460-HW 4 Adianto JoelAdianto TjandraNo ratings yet

- Homework 5 MGMT 41150 KeyDocument6 pagesHomework 5 MGMT 41150 KeyLaxus DreyerNo ratings yet

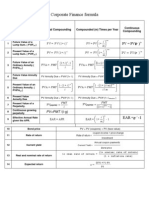

- Corporate Finance FormulasDocument3 pagesCorporate Finance FormulasMustafa Yavuzcan83% (12)

- Chapter 11 Compound Interest PDFDocument5 pagesChapter 11 Compound Interest PDFYAHIA ADELNo ratings yet

- Time Value of Money Formula SheetDocument2 pagesTime Value of Money Formula SheetMD Abrar FaiyazNo ratings yet

- Compound InterestDocument29 pagesCompound InterestNicole Roxanne RubioNo ratings yet

- BBM Student Handbook - (Intake AY19-20)Document47 pagesBBM Student Handbook - (Intake AY19-20)Justin ChongNo ratings yet

- How To Calculate Present Values?: Abhinav Anand (IIM Bangalore)Document50 pagesHow To Calculate Present Values?: Abhinav Anand (IIM Bangalore)Gaurav SainiNo ratings yet

- Iquanta SICI PDFDocument12 pagesIquanta SICI PDFSiddhartha ChoudhuryNo ratings yet

- Compound Interest All QuestionsDocument9 pagesCompound Interest All QuestionsAbhraham Benjamin de VilliersNo ratings yet

- Acc Assignment FMDocument66 pagesAcc Assignment FMram_prabhu003No ratings yet

- TVM TablesDocument21 pagesTVM Tablesanamika prasadNo ratings yet

- Sdepde PDFDocument202 pagesSdepde PDFGustaf TegnérNo ratings yet

- Understanding Variance SwapsDocument2 pagesUnderstanding Variance SwapsyukiyurikiNo ratings yet

- TVM TablesDocument13 pagesTVM TablesSaurabh ShuklaNo ratings yet

- Core Chapter 04 Excel Master 4th Edition StudentDocument150 pagesCore Chapter 04 Excel Master 4th Edition StudentDarryl WallaceNo ratings yet

- Bullock Gold Mining: Corporate Finance Case StudyDocument28 pagesBullock Gold Mining: Corporate Finance Case StudyVivek TripathyNo ratings yet

- Investment alternatives comparison using incremental IRRDocument7 pagesInvestment alternatives comparison using incremental IRRJual BelibarangNo ratings yet

- Mastering Option Trading Volatility Strategies With Sheldon NatenbergDocument31 pagesMastering Option Trading Volatility Strategies With Sheldon NatenbergGabriel Peixoto100% (4)

- Nama: Redi Perdiansyah NIM: 55120110139 Quiz Ke: 9: Stock X Stock y Stock ZDocument5 pagesNama: Redi Perdiansyah NIM: 55120110139 Quiz Ke: 9: Stock X Stock y Stock ZFikky Chandra SilabanNo ratings yet

- Basic Long-Term Financial ConceptsDocument40 pagesBasic Long-Term Financial ConceptsBr. Ivan Karlo Umali FSCNo ratings yet

- CH 9 ClsDocument2 pagesCH 9 Clsrupok100% (1)

- 1 The Black-Scholes ModelDocument12 pages1 The Black-Scholes ModeloptisearchNo ratings yet