You might also like

- Some Issues On Practice of TDS Law Some Issues On Practice of TDS Law Seminar by NIRC Seminar by NIRCDocument29 pagesSome Issues On Practice of TDS Law Some Issues On Practice of TDS Law Seminar by NIRC Seminar by NIRCJinoy P MathewNo ratings yet

- Seminar On TDSDocument29 pagesSeminar On TDSCA Virendra ChhajerNo ratings yet

- Some Issues On Practice of TDS Law Seminar by NIRCDocument29 pagesSome Issues On Practice of TDS Law Seminar by NIRCShashank Deva SunnyNo ratings yet

- Presentation On TDS Provision: by Nilesh Deharkar & AMAN BhattacharyaDocument15 pagesPresentation On TDS Provision: by Nilesh Deharkar & AMAN BhattacharyaAman BhattacharyaNo ratings yet

- TDS Rent - 194I - 194C PDFDocument54 pagesTDS Rent - 194I - 194C PDFkashyap_ajNo ratings yet

- Advance Learning On TDS Under Section 194-I and 194-C: MeaningDocument52 pagesAdvance Learning On TDS Under Section 194-I and 194-C: MeaningTejTejuNo ratings yet

- What Is Tax Deducted at SourceDocument6 pagesWhat Is Tax Deducted at SourcejdonNo ratings yet

- Deduction, Collection & Recovery of TaxesDocument143 pagesDeduction, Collection & Recovery of TaxesjyotiNo ratings yet

- Intro of TdsDocument6 pagesIntro of Tdsshivani singhNo ratings yet

- Tax Deduct at SourceDocument4 pagesTax Deduct at Sourceankit1070No ratings yet

- TDS Provisions SummaryDocument54 pagesTDS Provisions SummaryFalak GoyalNo ratings yet

- Lecture Notes - Study Module 9 - TDSDocument32 pagesLecture Notes - Study Module 9 - TDSdata.mvgNo ratings yet

- 30851ipcc May Nov14 It Vol1 CP 9.unlockedDocument43 pages30851ipcc May Nov14 It Vol1 CP 9.unlockedavesatanas13No ratings yet

- Tds Rate ChartDocument15 pagesTds Rate ChartJain MjNo ratings yet

- Section 195 TDS On Non-Resident PaymentsDocument1 pageSection 195 TDS On Non-Resident Paymentskumarsanjeev079No ratings yet

- TDS ElaboratedDocument80 pagesTDS ElaboratedAncyNo ratings yet

- TDS Rates Chart FY 2020-21: Key DetailsDocument9 pagesTDS Rates Chart FY 2020-21: Key Detailsjibin samuelNo ratings yet

- 19771ipcc It Vol1 Cp9Document40 pages19771ipcc It Vol1 Cp9Joseph SalidoNo ratings yet

- 67908bos54451 cp15Document167 pages67908bos54451 cp15Pools KingNo ratings yet

- TDS Rate Chart PDFDocument2 pagesTDS Rate Chart PDFjdhamdeep07No ratings yet

- A Book: Integrated Professional Competency Course (IPCC) Paper - 1: AccountingDocument12 pagesA Book: Integrated Professional Competency Course (IPCC) Paper - 1: AccountingSipoy SatishNo ratings yet

- 195 BCA PresentationDocument36 pages195 BCA PresentationCA Sagar WaghNo ratings yet

- Corporate Tax PlanningDocument139 pagesCorporate Tax PlanningDr Linda Mary SimonNo ratings yet

- TDS LAW AND PRACTICE UNDER INCOME TAX ACT 1961Document84 pagesTDS LAW AND PRACTICE UNDER INCOME TAX ACT 1961Vaibhav ChauhanNo ratings yet

- Deduction, Collection and Recovery of Tax: After Studying This Chapter, You Would Be Able ToDocument169 pagesDeduction, Collection and Recovery of Tax: After Studying This Chapter, You Would Be Able ToRajNo ratings yet

- CP 9 Advanced Tax, Tax Deduction at Source and Introduction of Tax Collection at SourceDocument108 pagesCP 9 Advanced Tax, Tax Deduction at Source and Introduction of Tax Collection at Sourcesaravana pandianNo ratings yet

- Sec. 34 IRC-DeductionsDocument8 pagesSec. 34 IRC-DeductionsMav ZamoraNo ratings yet

- Requirements U/S 195: By: Ca Sanjay K. AgarwalDocument71 pagesRequirements U/S 195: By: Ca Sanjay K. AgarwalHemanthKumarNo ratings yet

- RECENT AMENDMENTS TO TDS/TCS PROVISIONSDocument12 pagesRECENT AMENDMENTS TO TDS/TCS PROVISIONSABHISHEKNo ratings yet

- Instructions For Filling Out FORM ITR-2Document8 pagesInstructions For Filling Out FORM ITR-2Ganesh KumarNo ratings yet

- Final Paper 07 - Module 03 - Chapter 15Document169 pagesFinal Paper 07 - Module 03 - Chapter 15arunNo ratings yet

- CH 6Document95 pagesCH 6mulu melakNo ratings yet

- Income From Other SourcesDocument5 pagesIncome From Other SourcesGovarthanan NarasimhanNo ratings yet

- CA-Ashok-Mehta - PPT - Income TaxDocument88 pagesCA-Ashok-Mehta - PPT - Income TaxAbinash DasNo ratings yet

- Chapter 12 Tds & TcsDocument28 pagesChapter 12 Tds & TcsRajNo ratings yet

- Deductions From Gross IncomeDocument23 pagesDeductions From Gross IncomeAidyl PerezNo ratings yet

- IT Rates For Tax Deduction at SourceDocument12 pagesIT Rates For Tax Deduction at SourceArun EmmiNo ratings yet

- Finance Act 1991Document6 pagesFinance Act 1991Govardhan VaranasiNo ratings yet

- Part Tax Deducted at SourceDocument8 pagesPart Tax Deducted at SourcersroughNo ratings yet

- MRA RETURN NOTESDocument2 pagesMRA RETURN NOTESLavneesh ShibduthNo ratings yet

- RR 13-00Document2 pagesRR 13-00saintkarri100% (2)

- Bos 62600 SuDocument5 pagesBos 62600 Sunerises364No ratings yet

- Ch-9 Advance Tax, TDS, TCSDocument122 pagesCh-9 Advance Tax, TDS, TCSrinkal jethiNo ratings yet

- Section 195 and Form 15CBDocument53 pagesSection 195 and Form 15CBVALTIM09No ratings yet

- Section 40Document4 pagesSection 40Anil MathewNo ratings yet

- TDS RatesDocument9 pagesTDS RatesCharu JagetiaNo ratings yet

- Taxs Law ExamDocument15 pagesTaxs Law ExamSaif AliNo ratings yet

- Deduction PDFDocument207 pagesDeduction PDFdeepluthra6No ratings yet

- Section 194Document10 pagesSection 194Hitesh NarwaniNo ratings yet

- Articleship Exam QuestionsDocument33 pagesArticleship Exam QuestionsVarshiniNo ratings yet

- Tax Planning Decisions for Capital Structure, Dividends & Infrastructure DeductionsDocument50 pagesTax Planning Decisions for Capital Structure, Dividends & Infrastructure DeductionsRahul SinghNo ratings yet

- Income From Other SourcesDocument12 pagesIncome From Other Sourcessanjul2008No ratings yet

- Tax Deducted at Source: - Presented By: CA Prabhat Kumar Tandon Fca, Disa (Icai)Document20 pagesTax Deducted at Source: - Presented By: CA Prabhat Kumar Tandon Fca, Disa (Icai)shefalijais6491No ratings yet

- TDS Under Sec 194A EtcDocument26 pagesTDS Under Sec 194A EtcDivyaNo ratings yet

- Permanent Esta researchDocument24 pagesPermanent Esta researchNeha PandeyNo ratings yet

- Income Tax TdsDocument147 pagesIncome Tax TdsRohit SinghNo ratings yet

- CA Final Direct Tax Quick Revision of Assessment of Various 9DB7WBXYDocument16 pagesCA Final Direct Tax Quick Revision of Assessment of Various 9DB7WBXYRocka FellaNo ratings yet

- Applicable Tax Deduction at Source Tds 2023Document4 pagesApplicable Tax Deduction at Source Tds 2023Hemangi PrabhuNo ratings yet

- Unit - 3: Profits and Gains of Business or Profession: After Studying This Chapter, You Would Be Able ToDocument166 pagesUnit - 3: Profits and Gains of Business or Profession: After Studying This Chapter, You Would Be Able ToSakshi SharmaNo ratings yet

- Sales InvoicesDocument1 pageSales InvoicesMayank ManiNo ratings yet

- 415 Baldwin Ave, APT 7, Jersey City, NJ 07306Document5 pages415 Baldwin Ave, APT 7, Jersey City, NJ 07306Estrada Pence HoseaNo ratings yet

- Malta TINDocument4 pagesMalta TINMelvin ScorfnaNo ratings yet

- Madhyanchal Vidyut Vitran Nigam Limited, Lucknow: Shabnam ShabnamDocument2 pagesMadhyanchal Vidyut Vitran Nigam Limited, Lucknow: Shabnam ShabnamYadav Manish KumarNo ratings yet

- 2019 Taxation Law FundamentalsDocument14 pages2019 Taxation Law FundamentalsMiamor NatividadNo ratings yet

- Outlier Innovations Private Limited Other Charges Invoice (Dec-2022)Document2 pagesOutlier Innovations Private Limited Other Charges Invoice (Dec-2022)SiddharthNo ratings yet

- Basic Concepts: Bcom CC 306 Semester 3 Income Tax Laws and PracticeDocument6 pagesBasic Concepts: Bcom CC 306 Semester 3 Income Tax Laws and PracticeAnushka PriyaNo ratings yet

- Tax TermsDocument3 pagesTax TermsRAJINIKNTH REDDYNo ratings yet

- 25.2 MR of TOLENTINO V Secretary of FinanceDocument2 pages25.2 MR of TOLENTINO V Secretary of FinanceTelle MarieNo ratings yet

- Tax Planning Tax Avoidance &tax EvasionDocument8 pagesTax Planning Tax Avoidance &tax EvasionIshpreet Singh BaggaNo ratings yet

- TRAIN Seminar by Rex Recoter ComparisonDocument11 pagesTRAIN Seminar by Rex Recoter ComparisonmonaileNo ratings yet

- Monetary Fiscal Policy MCQsDocument17 pagesMonetary Fiscal Policy MCQsrohanNo ratings yet

- Charge OF GST: After Studying This Chapter, You Will Be Able ToDocument93 pagesCharge OF GST: After Studying This Chapter, You Will Be Able ToPraveen Reddy DevanapalleNo ratings yet

- Tax MCqsDocument10 pagesTax MCqsassadrafaqNo ratings yet

- Individual Income Tax Return and SummaryDocument2 pagesIndividual Income Tax Return and SummaryJackson RodrigoNo ratings yet

- Service Estimate: CustomerDocument2 pagesService Estimate: CustomerazharNo ratings yet

- EU VAT Regulations 2014Document24 pagesEU VAT Regulations 2014mattgirvNo ratings yet

- Export Invoice TitleDocument1 pageExport Invoice TitleMihir Kumar MohapatraNo ratings yet

- GST Tax Invoice Format For Goods - TeachooDocument2 pagesGST Tax Invoice Format For Goods - TeachooAzhar Ahmed100% (1)

- Perry County Republican Candidates For 2015 ElectionDocument19 pagesPerry County Republican Candidates For 2015 ElectionPennLiveNo ratings yet

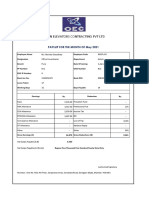

- Orion Elevators Contracting PVT LTD: Payslip For The Month of May 2021Document1 pageOrion Elevators Contracting PVT LTD: Payslip For The Month of May 2021Monika ChoudhariNo ratings yet

- Contract Librarian Appointment Template 06 21 08Document2 pagesContract Librarian Appointment Template 06 21 08Winniejanes nyabokeNo ratings yet

- PayslipDocument1 pagePayslipCristina Frias100% (1)

- The lack of effectiveness of tax exemption policies in achieving development on the Algerian economyDocument27 pagesThe lack of effectiveness of tax exemption policies in achieving development on the Algerian economyHamid HathatiNo ratings yet

- Amended 1040 Tax Form ExplainedDocument2 pagesAmended 1040 Tax Form Explainedgolcha_edu532No ratings yet

- Spring 2023 FIN623 1Document2 pagesSpring 2023 FIN623 1Shahid SaeedNo ratings yet

- Salient Features of GSTDocument8 pagesSalient Features of GSTNaraesh KNo ratings yet

- TCS compensation letter details annual pay Rs. 4,69,860Document4 pagesTCS compensation letter details annual pay Rs. 4,69,860AbdulkhadarJilani ShaikNo ratings yet

- Tax on Lottery Winnings UpheldDocument1 pageTax on Lottery Winnings UpheldEANo ratings yet

- International Finance - TCS Case StudyDocument22 pagesInternational Finance - TCS Case StudyPrateek SinglaNo ratings yet