You might also like

- Desain Test of ControlDocument5 pagesDesain Test of ControlyaniNo ratings yet

- Logical Models Communicate Business RequirementsDocument27 pagesLogical Models Communicate Business RequirementsAdam OngNo ratings yet

- Modern Auditing: Audit Procedures in Response to Assessed RisksDocument21 pagesModern Auditing: Audit Procedures in Response to Assessed Riskschandraindra33No ratings yet

- CC13 2 (Book/static) : Risk Assessment ProceduresDocument94 pagesCC13 2 (Book/static) : Risk Assessment Proceduresmonika1yustiawisdanaNo ratings yet

- ch05 Managerial AccountingDocument75 pagesch05 Managerial AccountingFiryal Yulda100% (1)

- Audit Report AnalysisDocument9 pagesAudit Report AnalysisRey Aurel TayagNo ratings yet

- Modern Auditing Revenue Cycle Audit ProceduresDocument32 pagesModern Auditing Revenue Cycle Audit ProceduresseptherineNo ratings yet

- Audit 2 Week 6 AssignmentDocument11 pagesAudit 2 Week 6 AssignmentDewi RenitasariNo ratings yet

- Internal control weaknesses in purchasing system under 40 charactersDocument3 pagesInternal control weaknesses in purchasing system under 40 charactersRosaly JadraqueNo ratings yet

- Chapter 3: Product Costing and Cost Accumulation in A Batch Production EnvironmentDocument31 pagesChapter 3: Product Costing and Cost Accumulation in A Batch Production EnvironmentSusan TalaberaNo ratings yet

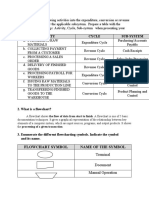

- Activity Cycle Sub-System: Flowchart Symbol Name of The SymbolDocument3 pagesActivity Cycle Sub-System: Flowchart Symbol Name of The SymbolALLIAH CARL MANUELLE PASCASIONo ratings yet

- Revenue Cycle - 31082021Document46 pagesRevenue Cycle - 31082021buat bersamaNo ratings yet

- CH 10Document37 pagesCH 10yurisukmaNo ratings yet

- Bank Audit Process and TypesDocument33 pagesBank Audit Process and TypesVivek Tiwari50% (2)

- Just in Time Jit Back FlushDocument16 pagesJust in Time Jit Back FlushSunsong31No ratings yet

- Section 404 Audits of Internal Control and Control RiskDocument8 pagesSection 404 Audits of Internal Control and Control RiskMuneera Al HassanNo ratings yet

- Chapter 12 HomeworkDocument4 pagesChapter 12 HomeworkMargareta JatiNo ratings yet

- Review Questions: Solutions Manual To Accompany Dunn, Enterprise Information Systems: A Pattern Based Approach, 3eDocument17 pagesReview Questions: Solutions Manual To Accompany Dunn, Enterprise Information Systems: A Pattern Based Approach, 3eOpirisky ApriliantyNo ratings yet

- Tugas Auditing 1 Pertanyaan Dan Soal Diskusi No 14-30 Sampai 14-32 14-30 (Objective 14-5) You Have Been Asked by The Board of Trustees of A Local ChurchDocument4 pagesTugas Auditing 1 Pertanyaan Dan Soal Diskusi No 14-30 Sampai 14-32 14-30 (Objective 14-5) You Have Been Asked by The Board of Trustees of A Local ChurchHusnul KhatimahNo ratings yet

- Chapter 9 - Profit PlanningDocument28 pagesChapter 9 - Profit PlanningEnrique Miguel Gonzalez Collado0% (1)

- Audit Programme - Order To CashDocument14 pagesAudit Programme - Order To CashTang SamNo ratings yet

- Johnstone 9e Auditing Chapter 13 PPT FINALDocument63 pagesJohnstone 9e Auditing Chapter 13 PPT FINALNurlinaEzzati100% (1)

- Work Centers and Storekeeping: (FG) WarehouseDocument4 pagesWork Centers and Storekeeping: (FG) WarehouseFatima Erica I. DatumangudaNo ratings yet

- Unit 5: Audit of Fixed AssetsDocument4 pagesUnit 5: Audit of Fixed AssetsTilahun S. KuraNo ratings yet

- Problem CH 7 Hansen Mowen Cornerstone of Managerial AccountingDocument8 pagesProblem CH 7 Hansen Mowen Cornerstone of Managerial Accountingwiwit_karyantiNo ratings yet

- AC414 - Audit and Investigations II - Introduction To Audit EvidenceDocument32 pagesAC414 - Audit and Investigations II - Introduction To Audit EvidenceTsitsi AbigailNo ratings yet

- Inventory and Production AuditDocument16 pagesInventory and Production AuditArlyn Pearl PradoNo ratings yet

- The Gross Profit Method For Estimated Ending InventoryDocument4 pagesThe Gross Profit Method For Estimated Ending InventoryKeith Joanne Santiago100% (2)

- Target Costing PDFDocument44 pagesTarget Costing PDFAnonymous dPkadxxNo ratings yet

- Quiz CH 9-11 SchoologyDocument8 pagesQuiz CH 9-11 SchoologyperasadanpemerhatiNo ratings yet

- Z003800101201740141305080572 448187Document51 pagesZ003800101201740141305080572 448187Dian AnitaNo ratings yet

- Auditing CIS EnvironmentsDocument7 pagesAuditing CIS EnvironmentsSteffany RoqueNo ratings yet

- Cash Receipts CycleDocument4 pagesCash Receipts CycleYenNo ratings yet

- Completing The AuditDocument26 pagesCompleting The AuditJuliana ChengNo ratings yet

- Audit Procedures: TOC and STOTDocument3 pagesAudit Procedures: TOC and STOTAmandaTalithaRahmaditaNo ratings yet

- Chapter 5 - Business Processes and RisksDocument36 pagesChapter 5 - Business Processes and Riskssiti fatimatuzzahra100% (2)

- Module IV: MUS Sampling - Factory Equipment Additions: RequirementsDocument2 pagesModule IV: MUS Sampling - Factory Equipment Additions: RequirementsMukh UbaidillahNo ratings yet

- Objectives and Phases of Operational AuditsDocument12 pagesObjectives and Phases of Operational AuditsChloe Anne TorresNo ratings yet

- Audit of The Sales and Collection CycleDocument51 pagesAudit of The Sales and Collection CycleZaza FrenchkiesNo ratings yet

- Activity-Based Costing Success (ABC) Implementation in China The Effect of OrganizationalDocument19 pagesActivity-Based Costing Success (ABC) Implementation in China The Effect of Organizationaldiah_savitri12No ratings yet

- Audit Evidence Decisions and ProceduresDocument4 pagesAudit Evidence Decisions and ProceduresRian MamunNo ratings yet

- Auditing Cash BalancesDocument9 pagesAuditing Cash Balancessamuel debebeNo ratings yet

- Expenditure Cycle & Case StudyDocument7 pagesExpenditure Cycle & Case StudybernadetteNo ratings yet

- Chapter 16 Environmental CostDocument34 pagesChapter 16 Environmental CostAngga100% (1)

- LeaseDocument20 pagesLeasesimply Pretty0% (1)

- Auditing I: Chapter 6 (Internal Control in A Financial Statement Audit)Document16 pagesAuditing I: Chapter 6 (Internal Control in A Financial Statement Audit)CrystalNo ratings yet

- Worldcom - Executive Summary Company BackgroundDocument4 pagesWorldcom - Executive Summary Company BackgroundYosafat Hasvandro HadiNo ratings yet

- Audit and Working PapersDocument2 pagesAudit and Working PapersJoseph PamaongNo ratings yet

- Threats and Controls For The Revenue Expenditure Production CyclesDocument7 pagesThreats and Controls For The Revenue Expenditure Production CyclesAldwin CalambaNo ratings yet

- Audit of Biological AssetsDocument4 pagesAudit of Biological AssetsNicNo ratings yet

- IFRS 15 Session4 Handout 1Document2 pagesIFRS 15 Session4 Handout 1Simon YossefNo ratings yet

- Chapter 7 Audit of The Purchases and Payment CycleDocument34 pagesChapter 7 Audit of The Purchases and Payment CycleRishika RapoleNo ratings yet

- Chapter 15 - Auditing The Expenditure CycleDocument30 pagesChapter 15 - Auditing The Expenditure Cycle小菁No ratings yet

- Section - 5 Case-5.3Document21 pagesSection - 5 Case-5.3syafira0% (1)

- Chapter 9 - Audit Sampling - Substantive Tests of Account Balances - AnswersDocument49 pagesChapter 9 - Audit Sampling - Substantive Tests of Account Balances - Answerssat726No ratings yet

- Audit Inventory Warehousing CycleDocument9 pagesAudit Inventory Warehousing CycleREG.B/0115103003/ERSA KUSUMAWARDANINo ratings yet

- Overview of The Financial Statement Audit Process (Final) PDFDocument8 pagesOverview of The Financial Statement Audit Process (Final) PDFMica R.No ratings yet

- Audit BoyntonDocument35 pagesAudit BoyntonMasdarR.MochJetrezzNo ratings yet

- Modern Auditing Personnel Production CyclesDocument35 pagesModern Auditing Personnel Production CyclesPermata KeristiyaNo ratings yet

- Auditing Production Cycles Under 40 CharactersDocument18 pagesAuditing Production Cycles Under 40 CharactersMuhammad Haris Fajar RahmatullahNo ratings yet

- IEM COE QuestionsDocument11 pagesIEM COE QuestionsMohd A Ishak0% (1)

- Umiiiiiiiiiiiiiiiiii GGGGGGGGGGDocument13 pagesUmiiiiiiiiiiiiiiiiii GGGGGGGGGGMuhammad Umair YunasNo ratings yet

- Motorola's Training ExcellenceDocument19 pagesMotorola's Training ExcellenceYashupriya ThakurNo ratings yet

- Kasambahay Law ExplainedDocument8 pagesKasambahay Law ExplainedKR ReborosoNo ratings yet

- Office OF THE Student Regent: Matters Arising From The Previous MinutesDocument80 pagesOffice OF THE Student Regent: Matters Arising From The Previous MinutesOffice of the Student Regent, University of the PhilippinesNo ratings yet

- SSS Promotion ApplicationDocument1 pageSSS Promotion ApplicationEL BertNo ratings yet

- TGB Communication ReportDocument17 pagesTGB Communication ReportRima AgarwalNo ratings yet

- Global Teams Report FinalDocument22 pagesGlobal Teams Report FinalDavid Briggs100% (1)

- Introduction To Performance ManagementDocument23 pagesIntroduction To Performance ManagementGajaba GunawardenaNo ratings yet

- Lesson 6: Contemporary Economic Issues Facing The Filipino EntrepreneurDocument14 pagesLesson 6: Contemporary Economic Issues Facing The Filipino EntrepreneurApril Joy DelacruzNo ratings yet

- Johnson LawsuitDocument129 pagesJohnson LawsuitJessacaNo ratings yet

- NA Payroll 9.0Document155 pagesNA Payroll 9.0poornima_np80% (5)

- Workplace Violence in Nursing: A Concept Analysis: Mahmoud Mustafa Al-Qadi RN, MSN, MHADocument11 pagesWorkplace Violence in Nursing: A Concept Analysis: Mahmoud Mustafa Al-Qadi RN, MSN, MHASHOAIB BUDALASINo ratings yet

- PSM Compliance ManualDocument6 pagesPSM Compliance ManualMohammed Zubair100% (1)

- Charlotte HamiltonDocument3 pagesCharlotte Hamiltoncharlotte190hamiltonNo ratings yet

- 24042015045230advt 05 VSA 2015 PDFDocument3 pages24042015045230advt 05 VSA 2015 PDFSunil SharmaNo ratings yet

- Career Planning & Succession Planning: Prof. Preeti BhaskarDocument40 pagesCareer Planning & Succession Planning: Prof. Preeti BhaskarDrNeeraj N. RanaNo ratings yet

- The Impact of Impression Management Behavior On Organizational PoliticsDocument12 pagesThe Impact of Impression Management Behavior On Organizational PoliticsispmuxNo ratings yet

- Introduction To BusinessDocument534 pagesIntroduction To BusinessgladioNo ratings yet

- Topic 4: Morphological Analysis and Related TechniquesDocument41 pagesTopic 4: Morphological Analysis and Related TechniqueschenboontaiNo ratings yet

- Human Resource Management Failure Is The Death of A BusinessDocument15 pagesHuman Resource Management Failure Is The Death of A Businessndayishimiye innocentNo ratings yet

- OQP Student Flyer 2Document2 pagesOQP Student Flyer 2Safnas KariapperNo ratings yet

- Project Report On PMSDocument50 pagesProject Report On PMSrohitbatraNo ratings yet

- Oracle HRMS Online TrainingDocument9 pagesOracle HRMS Online TrainingcosmosonlinetrainingNo ratings yet

- Literature Review ofDocument27 pagesLiterature Review ofSebastián OlaveNo ratings yet

- HRM Final Report ("Recruitment and Selection Process of The Nestlé Bangladesh Limited")Document34 pagesHRM Final Report ("Recruitment and Selection Process of The Nestlé Bangladesh Limited")mirraihan37100% (1)

- SBN-0832: Philippine Nursing Practice Reform ActDocument28 pagesSBN-0832: Philippine Nursing Practice Reform ActRalph RectoNo ratings yet

- Ch.7 Designing Organizational Structure (Chapter Review Slides)Document27 pagesCh.7 Designing Organizational Structure (Chapter Review Slides)Tirsolito SalvadorNo ratings yet

- Sagicor Insurance Company V Carter Et Al AXeZm3Cdo5CdlDocument23 pagesSagicor Insurance Company V Carter Et Al AXeZm3Cdo5CdlNathaniel PinnockNo ratings yet

- EMPLOYEE COMPENSATION & BENEFITS GUIDEDocument9 pagesEMPLOYEE COMPENSATION & BENEFITS GUIDEjaydee_atc5814100% (1)