You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Emerging Issues - HR Policies of NK MindaDocument5 pagesEmerging Issues - HR Policies of NK MindaAyushmaan BaroowaNo ratings yet

- UntitleddocumentDocument6 pagesUntitleddocumentapi-343534512No ratings yet

- Agency Problem in Financial Management - CFA Research NotesDocument59 pagesAgency Problem in Financial Management - CFA Research NotesVANEENo ratings yet

- Cost Accounting Question BankDocument28 pagesCost Accounting Question BankdeepakgokuldasNo ratings yet

- Institute For Construction Training and Development (ICTAD)Document33 pagesInstitute For Construction Training and Development (ICTAD)Nuwan Sudharshana Weerathunga60% (5)

- 91a2 14 03939 Coll Agree Local79 Nov12 PDFDocument272 pages91a2 14 03939 Coll Agree Local79 Nov12 PDFMarie and Ricardo Benoit/ThompsonNo ratings yet

- Deloitte Future of Work in Financial ServicesDocument20 pagesDeloitte Future of Work in Financial ServicesSandra DeeNo ratings yet

- Employee Training Benefits for Organizations and IndividualsDocument12 pagesEmployee Training Benefits for Organizations and IndividualsDirgo WicaksonoNo ratings yet

- Answer Sheet Gen Math Mod 9Document6 pagesAnswer Sheet Gen Math Mod 9ahlsy CazopiNo ratings yet

- Board StructureDocument21 pagesBoard Structureharman singhNo ratings yet

- Planning With People in MindDocument21 pagesPlanning With People in MindParnamoy Dutta100% (1)

- Decentralization Education PhilippinesDocument34 pagesDecentralization Education PhilippinesDanvie Ryan Phi100% (4)

- Dickens' Novels Highlight Cruelty of 19th Century Child LabourDocument2 pagesDickens' Novels Highlight Cruelty of 19th Century Child LabourMarioara CiobanuNo ratings yet

- Rajasthan-Fix Pay-Notification Dated 13 3 2006 PDFDocument2 pagesRajasthan-Fix Pay-Notification Dated 13 3 2006 PDFMithilesh Narayan BhattNo ratings yet

- English Specific Purposes Curriculum DevelopmentDocument12 pagesEnglish Specific Purposes Curriculum DevelopmentjohnferneyNo ratings yet

- FINAL - ANABIEZA With CommentsDocument25 pagesFINAL - ANABIEZA With CommentsQuint Reynold DobleNo ratings yet

- HRM Theories for Motivating EmployeesDocument21 pagesHRM Theories for Motivating EmployeesDalila MatakovaNo ratings yet

- 4012 For 2017 ReturnsDocument349 pages4012 For 2017 ReturnsSarah EunJu LeeNo ratings yet

- Economics Igcse Paper 1 2020Document8 pagesEconomics Igcse Paper 1 2020Germán AmayaNo ratings yet

- Full CasesDocument101 pagesFull CasesFaye CordovaNo ratings yet

- Caselet For Module 1Document2 pagesCaselet For Module 1Bea BalaoroNo ratings yet

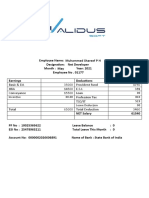

- Salary SlipDocument4 pagesSalary Slipbindu mathaiNo ratings yet

- Angel Sucia CabanDocument32 pagesAngel Sucia CabanAngel CabanNo ratings yet

- Shui Fabrics (Compiled) 2 FINALDocument7 pagesShui Fabrics (Compiled) 2 FINALHanz SoNo ratings yet

- Recruitment Process Flow ChartDocument6 pagesRecruitment Process Flow Chartashaishaishu100% (2)

- SAP-HR OM & PA Tables, Infotypes and Their FieldsDocument12 pagesSAP-HR OM & PA Tables, Infotypes and Their FieldsSuren VictorNo ratings yet

- Toyota dismissal case ruling upheldDocument6 pagesToyota dismissal case ruling upheldIm reineNo ratings yet

- General Principles in Statutory ConstructionDocument8 pagesGeneral Principles in Statutory ConstructionRonald DalidaNo ratings yet

- Occupation Health Safety Practices at Roofing Rolling Mills-Uganda PDFDocument48 pagesOccupation Health Safety Practices at Roofing Rolling Mills-Uganda PDFMelvin Cherry100% (1)

- Business PlanDocument16 pagesBusiness Plansalehin1969No ratings yet